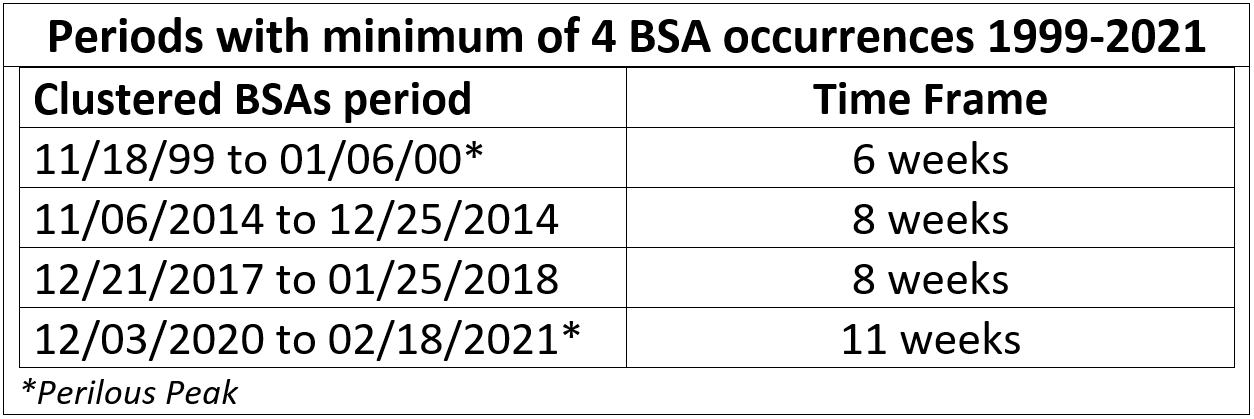

The probability is high for the S&P 500 in February 2022 to be below its February 2021 high. This quant-based conclusion is from my research findings on four clusters of BSAs (Bullish Sentiment Anomalies). Three of the BSA clusters were formed from 1999 to 2017. The fourth BSA cluster since 1999 was formed from 12/3/2020 to 2/18/2021.

The discovery was the S&P 500 underperformed or declined for the 12-month periods which follow a cluster of BSAs. The table below depicts the periods in which a minimum of four BSAs occurred within an 11-week time frame.

The BSA is an acronym for the Bullish Sentiment Anomaly which was discovered in November 2020. For more about BSAs which have occurred at all of the S&P 500’s Perilous Peaks since 1881 read my “DNA Discovery Confirms 2021 Perilous Peak & Secular Bull High for S&P 500”.

The BSA is calculated from the following:

- Bullish readings from American Association of Individual Investor (AAII) weekly individual investor sentiment surveys reaching a minimum level.

- S&P 500 trading at a record high during the same week in which AAII minimum is reached.

The charts below depict the post 12 months performance from when the first BSA occurred for each of the clustered BSA periods which began from 1999 to 2017.

The chart for 1999 to 2000 below depicts that a significant correction followed the BSAs. There was a quick recovery and the occurrence of a lone BSA which coincided with the S&P 500’s pre dotcom bubble bursting, Perilous Peak and Secular Bull highs.

The S&P 500 did not recover from the post BSA clustering 12 month decline. The index instead declined by 49% from its March 2000 high to its October 2002 low. The S&P did not exceed the high until March of 2013.

The chart for 2014 to 2015 below depicts that the S&P 500 experienced a significant draw down during the clustered BSAs period. For the balance of the 12 months the index declined by 12.3% from the high to the August 2015 low. From the point at which the last BSA occurred for the Clustered BSA period to the end of the 12 months, the S&P 500’s gain was a miniscule 0.67%.

The chart for 2017 to 2018 below depicts that the S&P 500 experienced an immediate 12% plus draw down at the end of the clustered BSAs period. The index closed the 12 months with a decline of 12.8% when compared to its level was when the first BSA occurred in 2017.

The reason why the S&P 500 underperforms or declines for the 12 months after a Clustered BSA period has occurred is because a BSA only occurs when the S&P 500 is at a record high and investors believe that it is going higher. Having four or more BSAs occurring within a concentrated six to 11-week period indicates that Bullishness is EXTREME.

The logic is simple. Investor sentiment has proven to be a good contrary indicator. If the majority of investors’ have the opinion:

- Bullish (stocks going higher); they are already fully invested …

(no cash left to buy)

- Bearish (stocks going lower); they have already cashed out …

(no shares left to sell)

The chart below depicts that the 2009 bottom for S&P 500’s post Lehman bankruptcy crash coincided with the AAII’s highest ever 70.2% Bearish sentiment reading.

The chart below depicts the S&P 500 & AAII Sentiment Survey Bullish & Bearish highs for the 12 months ended October 30, 2020. The Bullish sentiment reading of 45.6% was the highest for the 12 months. At the March low the 52.0% Bearish sentiment reading was the second highest for the 12 months ended October 31st. The chart below also depicts the first BSA (1-23-20) which had occurred since January 2018.

The discoveries of the DNA for a Perilous Peak DNA and the S&P 500’s underperformance for the 12 months after the BSAs had clustered is significant. They further support my thesis for why all investors should be effectuating a Secular Bear investing strategy immediately. To remain in a Secular Bull investing strategy is not logical. Read my “Prepare for the Bear”.

AlphaTack.com was developed to provide investors with Secular Bear Market investing products and strategies. The good news is that Alpha Tack is the lifeboat. The bad news is that since Alpha Tack is a lifeboat it does not have unlimited capacity. The two rules applicable to Secular Markets:

- In a Secular Bull Market, the majority of all stocks and asset classes can increase the value of a portfolio.

- In a Secular Bear Market, only a minority of all stocks and asset classes can increase the value of a portfolio.

Based on my experience during the Dow Jones’ 1966-1982 and 2000-2009 Secular Bear Markets the capacity of available growth investing opportunities for investors and investment advisors will be constrained. The inability to receive an allocation of a hot IPO is good example of the capacity constraints which will occur throughout a Secular Bear Market. Unfortunately, only a minority of investors and advisors will have access to the investment opportunities to enable assets to grow during a Secular Bear Market. En masse, portfolios will steadily decline.