Very often we emphasized that when investing in commodity market it is worth using ETFs. They have lower costs of a given investment or achieve better diversification. It happens, however, that for a given commodity an attractive fund has not been created yet, or an investment in those which exist carries too much risk. Then, investors are forced to choose individual companies, which requires a thorough analysis. Therefore, below we describe a number of factors that should be considered during the selection of mining companies for the investment portfolio.

Structure of revenues

In order for investment to make sense, first of all the selected company must actually give an exposure to a specific commodity. If we are dealing with a company that specializes in extracting only one element, the matter is simple.

The situation is somewhat more complicated when the company focuses on several different raw materials. Then we need to determine how much extraction revenues share has this particular commodity. Suppose we want to get exposure to iron ore. Therefore, we will look for a company whose revenues depend mainly on the extraction of this raw material.

The share of a given element in the company’s revenues can be easily checked on its website. Companies post such information when publishing results for a given period of time. It is also worth using presentations, which are written in a simpler language facilitating analysis.

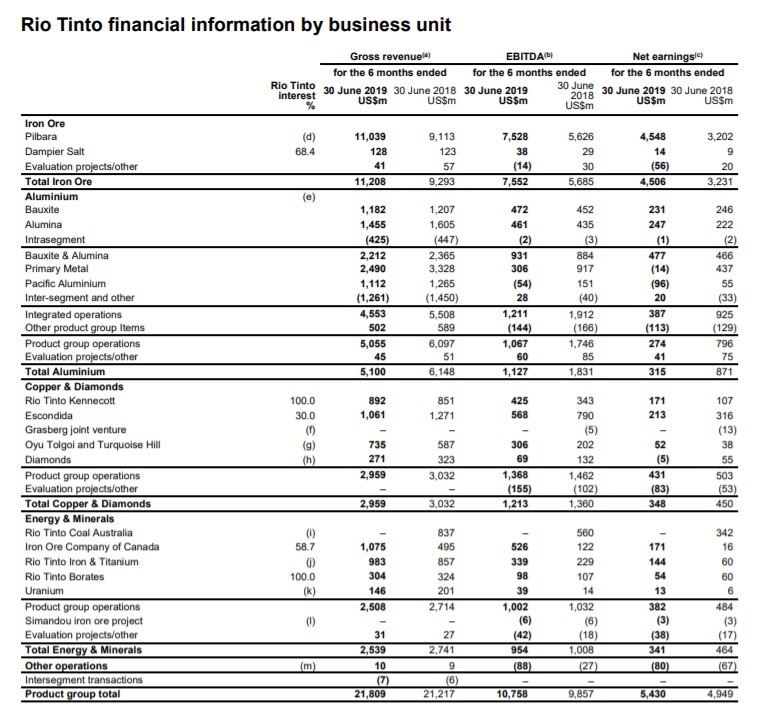

The table below comes from the Rio Tinto financial report for the first half of 2019. In the “Gross revenue” column, we can see that despite the fact that the company is involved in various raw materials, most of revenues come from the extraction of iron ore.

source: Rio Tinto annual report

Geographical diversification

From the investor’s point of view, it is also very important that the company has a well-diversified geographic portfolio of assets. It is worth choosing companies that carry out mining projects in various regions of the world. Thanks to this, our investment will be less susceptible, for example, to political turmoil in a single country.

This is also important in random situations that we are not able to predict. Such events in the mining industry are quite frequent. An example is Vale’s dam collapse, which took place at the end of January in Brazil.

Losses that the company suffered as a result of a dam break are just part of the problem. After the catastrophe, a number of regulations have been introduced in that country and impacted heavily the entire industry. If it was not for the fact that Vale conducts operations all over the world, the company’s situation could significantly deteriorate.

It is worth adding here that mining companies very often run projects in countries that, to put it mildly, are not considered as the safest. They decide to do that primarily because there are high-quality deposits there. As history shows, sometimes attacks on mines happen, during which organized criminal groups can steal a lot of valuable spoil. A perfect example of such a country is the Democratic Republic of the Congo, where the law is commonly violated and the level of corruption is extremely high.

In order to increase investment security, we should avoid companies heavily involved in mining projects in the jurisdictions described.

An example of a well-geographically diverse company is the previously mentioned Rio Tinto, which is confirmed by the map below.

source: RioTinto.com

As you can see, most Rio Tinto projects are located in developed countries such as Australia, United States, or Canada.

Evaluation of deposits

When planning investment in a mining company, it is necessary to check whether it has prospects for long-term extraction. We must read data of individual projects. We will look there for prediction of company’s exploration plans for specific deposits.

At this point it is worth recalling that mining companies divide deposits into three basic types:

1. Proven, i.e., the deposit for which a chance of mining is at least 90%.

2. Probable, where the probability is 50-90%.

3. Possible, with the chance of mining around 10-50%.

It is best if the company has large proven and probable deposits that will allow it to bring revenues over the next several years.

When assessing deposits, it will also be a good idea to check if the company hires geologists with extensive experience. Although there are a lot of mining companies on the market, but there are not so many real specialists.

Cost of extraction and commodity price

Another very important element of the analysis is the cost that the company incurs in order to extract one unit of a given raw material. The mining companies use different cost metrics, with AISC (i.e. all-in sustaining cost) being the most reliable. Of course, it has some drawbacks (does not take into account loan interest or income tax), but fairly presents production costs.

Suppose the company has AISC for gold at 1,000 USD per ounce, while the metal spot price is 1,400 USD per ounce. Therefore, the company earns 400 USD on every extracted gold ounce.

If the metal price suddenly increases by 10% (1,540 USD per ounce), profit will increase by 35% at the same time.

Thanks to this dependence, investing in mining companies can bring a much greater profit (or loss) than a direct investment in a given commodity.

Therefore, as described above, we should choose a company’s portfolio that has the lowest possible cost of extraction relative to the price of a given element. Therefore, we increase safety margin, because even if the price of the raw material decreases, the company will still earn money.

Company’s debt

Mining industry is extremely capital-intensive, and therefore the next important factor to consider is the company’s debt. Generally, the smaller it is the better. While a reasonable level of debt can accelerate the company’s development, too much debt can lead to bankruptcy.

It is worth getting to know two very useful indicators: Cash-to-Debt Ratio and Debt-to-Equity Ratio.

Cash-to-Debt indicator shows us to the extent of company’s debt covered in cash. The lower the index value, the worse. This means that the debt is much higher than the amount of cash available. In turn, if the company has many times more cash than debt, we can assume that it is ineffective.

It is worth adding here that the level of this indicator may suddenly increase, e.g., as a result of the sale of some of the company’s assets. It may also result from the increase in profitability, which is a reason why it should always be checked by referring to historical data. You can check it on gurufocus.com which provides data for free.

Second indicator, Debt-to-Equity Ratio, informs us about the extent of the company’s finances with debt in comparison to the funds that are its total property. High level of the ratio suggests that the company is aggressively getting into debt.

Historical data of commodities prices

Before we start analyzing a particular company, it is necessary to check the fundamentals of a given commodity. This is primarily about the structure of supply and demand. In the first place, we should be interested in elements which are missing on the market. In turn, we will avoid investments in raw materials, for which there is an oversupply.

On our blog, we have repeatedly pointed out about the undervaluation of tangible assets in relation to financial assets. This is best illustrated by the graphics below.

Despite favorable fundamentals, you can still invest at the wrong time, so you should check whether a given good is cheap in the short term. To this end, we can use, among others, Commitment of Traders (you can find more about it here).

At the same time, we check whether selected company is attractive in terms of indicators such as P/E, P/BV, etc. In the case of P/E ratio, it is worth adding that its negative value in terms of mining companies does not necessarily mean a bad investment. Why? We describe it below.

It happens that a given company will suffer due to a strong sell-off of the commodity which company extracts. Then, P/E values can go below zero. Afterwards, when there is a strong rebound in price of the element (after which the company’s quotes will also follow), the value of the P/E ratio will improve, and the company will remain attractively priced even after these increases.

Additionally, when opening a position, it is worth using technical analysis to get the best price.

Summary

We listed only a few factors that should be taken into account when assessing prospects of mining companies. In addition to them, it is also worth checking how much shares of the company are owned by insiders (the bigger the better). It is also beneficial if the company regularly pays high dividends, allocating a reasonable part of profits for this purpose.

Although sometimes buying individual companies is a must, we have to always look first for an attractive ETF, which will remove obligation of detailed analysis for dozens of companies. According to our observations, the best behaviour is in addition to exposure to the selected fund, to pick also additional 1-3 individual producers. In this way, we will protect ourselves from a situation similar to the one currently taking place in case of ETF REMX.

Despite favorable information about potential blocking of rare earth metals exports from China, this fund increased only slightly, while the most important companies in the industry brought very good returns.

Independent Trader Team