Wolf Richter wolfstreet.com, http://www.amazon.com/author/wolfrichter

Revisions show the slowdown expected this year hit last year, and now is the rebound. If there’s ever a time for the Fed to not cutalready low interest rates, it’s now.

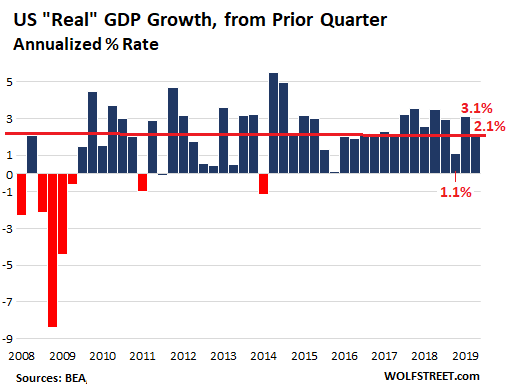

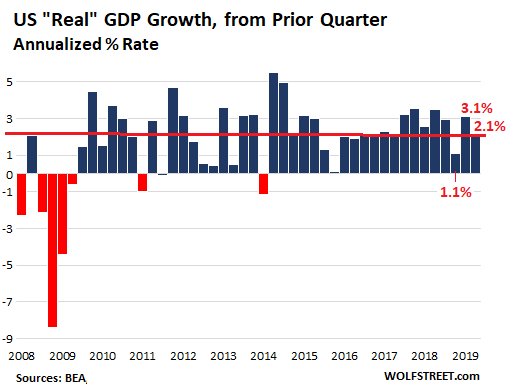

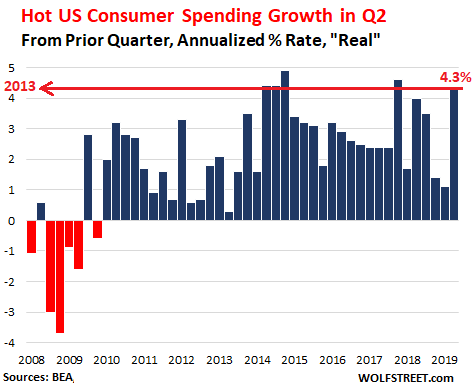

Economic growth in the US for the second quarter once again exceeded consensus expectations, after blowing past them in the first quarter. This morning, the Bureau of Economic Analysis reported that the economy, as measured by “real” (inflation-adjusted) GDP, grew at an annualized rate of 2.1%. It was powered by the hottest consumer spending growth since Q4 2017, and the fifth highest quarterly growth in the past 52 quarters (since Q1 2006).

But the GDP growth rates for 2018 were slashed, particularly for Q4. It is now apparent that the slowdown that was expected this year but didn’t arrive actually took place in Q4 last year, and what we’re seeing this year is a rebound:

Consumer spending, which accounts for nearly 70% of the economy, grew at an annualized rate of 4.3%, adjusted for inflation, blowing past expectations, after having been lethargic in Q4 last year and Q1 this year. It was the fastest growth rate since Q4 2017 and the fifth fastest since Q1 2006.

By category, consumer spending on durable goods soared at an annualized rate of 12.9%, adjusted for inflation; and for non-durable goods, it jumped 6.0%. This brought the growth rate for spending on all goods combined to 8.3%. Spending on services rose 2.5%.

A decided weakness in the data was business investment. Gross private domestic investment fell 5.5%, including at 10.6% drop in investment in structures. And it includes a big drop in private inventories. This confirms the phenomenon we have seen for months now in what I now call the “transportation recession,” where companies, sitting on bloated inventories they acquired to frontrun the tariffs, are cutting back orders to whittle those inventories down, and therefore shipments decline.

The inventory pileup we have been discussing since last year, and that boosted Q1 GDP growth, has started to reverse in Q2. An increase in inventories is considered an “investment” and is added to GDP growth. A decrease in inventories is subtracted from GDP growth. Everyone expected this would happen eventually – and now it happened. In Q2, “private inventories” fell by $44.3 billion, which knocked 0.9 percentage points off the GDP growth rate. Had inventories remained flat, the GDP growth rate would have been about 3%.

The tantalizing data in today’s release were the radical downward revisions of GDP growth in 2018, for Q2, Q3, and Q4. The growth rate in Q4 got slashed from 3.0% earlier this year to 1.1% today, the lowest growth rate since Q4 2015.

In other words, the slowdown that was supposed to hit this year hit in Q4 last year, and the economy already muddled through this episode and is now bouncing back, with GDP growth averaging 2.6% this year so far.

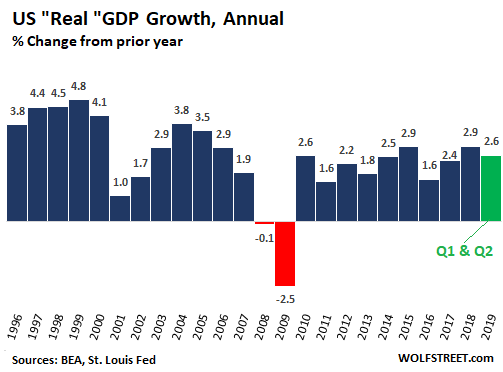

The revisions caused the annual growth rate of 2018 to be revised down to 2.9%, still the highest rate since 2015 (also 2.9%), but below the illusory 3% level that the US hasn’t reached since 2004. The chart shows the revised annual rates of growth adjusted for inflation, with 2019 (green) being the average of Q1 and Q2. This is not a chart of a rate-cut economy:

So far in 2019, US economic growth is back in the upper end of the range since the great recession. That range stretched from 1.6% growth at the low end in 2016 to 2.9% growth at the high end in 2018 and 2015.

The economy is still powered by very low interest rates, massive government spending growth, and consumers that are working and making money and spending money. Some business investment has taken a wait-and-see approach, but hiring is strong, companies complain about the difficulty of finding qualified workers, and unemployment claims hover at multi-decade lows. If there was ever a time for the Fed to not cut already low interest rates, it’s now. The economy is, as Powell has stated many times recently, “in a good place.”

Despite the trade wars, tariffs, and counter-tariffs, consumers and companies keep plugging, and the world has not come to an end. Read… World Trade in Face of Tariffmageddon, Trade Wars & Manufacturing Slowdown