Fed Chair Jerome Powell just spooked the markets by predicting that inflation will jump when the economy reopens – but don’t worry, it’s just temporary. Here’s the real-time CNBC account:

Fed’s Powell says reopening could cause inflation to pick up temporarily

Federal Reserve Chairman Jerome Powell said Thursday that he expects some inflationary pressures in the time ahead but they likely won’t be enough to spur the central bank to hike interest rates.

“We expect that as the economy reopens and hopefully picks up, we will see inflation move up through base effects,” Powell said during a Wall Street Journal conference. “That could create some upward pressure on prices.”

The Fed likes inflation to run around 2%, a rate it believes signals a healthy economy and provides some room to cut interest rates during times of crisis. However, the rate has run below that for most of the past decade and inflation has been particularly weak during the pandemic.

With the economy increasingly back on its feet, some price pressures are likely to emerge, said Powell, but he said they likely will be transitory and look higher because of “base effects,” or the difference measures against last year’s deeply depressed levels just as the Covid-19 crisis began.

Now, this comes as the federal government is preparing to hit the economy with … wait for it… $4 trillion of created-out-of-thin-air cash, in the form of the covid stimulus bill currently in the Senate and the blockbuster “infrastructure” plan that’s apparently next in the pipeline. Here’s Goldman Sachs’ prediction on that one:

Biden’s Infrastructure Bill Could Be $2 Trillion Behemoth—Here’s What Goldman Sachs Is Expecting

With President Biden’s $1.9 trillion stimulus bill now making its way to the Senate, analysts from investment giant Goldman Sachs laid out their expectations for his forthcoming infrastructure spending initiative—the second phase of his ambitious plan to revitalize the American economy.

In a research note late Sunday, Goldman Sachs’ analysts said they expect the proposal will be worth at least $2 trillion—and potentially even double that—over the next 10 years based on previous proposals and estimates of how much investment will be necessary to shore up U.S. infrastructure.

They also note that the upcoming package could be broader in scope than expected and has the potential to expand beyond infrastructure, green energy, and climate change initiatives to include a spate of Democratic priorities including childcare, healthcare, and education initiatives, though the Washington Post reported last month that Democrats are far from united on what the final proposal should look like.

“We are so far behind the curve,” Biden said last month ahead of a meeting with labor leaders to discuss his stimulus and infrastructure legislation. “We rank something like 38th in the world in terms of our infrastructure—everything from canals to highways to airports.” He added that the United States needs to do “everything we can do…to make ourselves competitive in the 21st century.”

A quick digression: Notice the neat bit of misdirection here? “Infrastructure,” like “covid relief,” can in practice mean pretty much anything a political party wants to give its favorite voting blocs. So childcare, education, you name it, it’s either relief or infrastructure.

It’s simpler to just view this year’s spending as a back-door bailout for badly run cities and states. After all, part of being “badly-run” is skimping on roads, bridges, etc., in order to fund wildly overgenerous public sector pensions. Because most of these places have been ruined by politicians from the same party that now controls Washington, a direct bailout would be politically dangerous. But give a bill a popular name and Congress can lard it with everything on the wish list.

Now back to an analysis of the numbers, the point of which is that in this late, decadent stage of rampant financialization, governments will always find a way to borrow and spend more, because there’s really no other option if they want to avoid presiding over Great Depression 2.0. More debt won’t delay the Big D forever of course, but it might move it beyond the retirement date of most of the current political class, and for them, that seems to be enough.

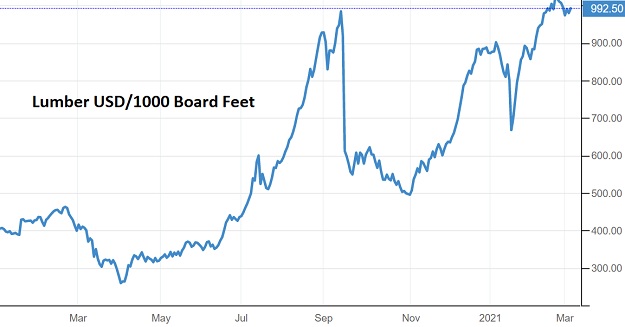

As for temporary inflation, one could make the case that it’s already raging. Lumber, for instance …

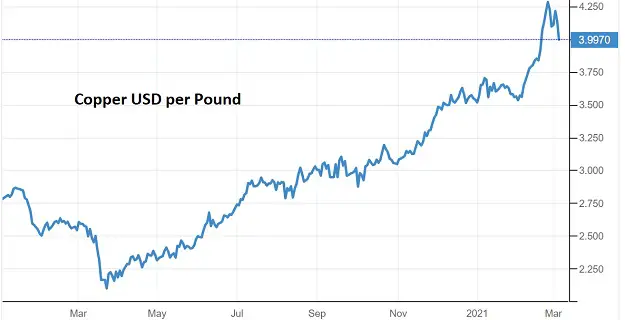

… and copper…

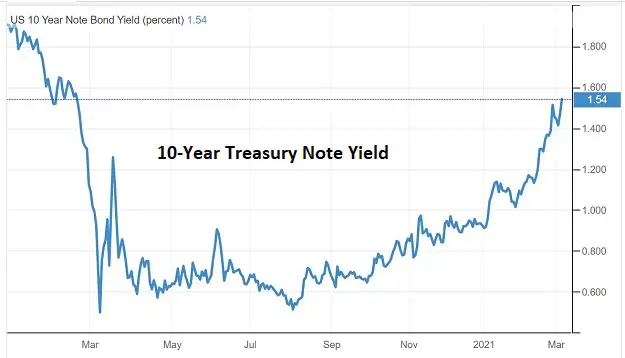

… and of course interest rates. The 10-year Treasury Note responded to Powell’s speech by jumping back up to 1.5%.

These are all signs of an overheating economy – BEFORE several trillion more dollars inundate construction, housing, and finance. So how exactly can the Fed know that the even more broad-based inflation likely to result from tossing new gasoline onto this fire will burn itself out in a few months? The answer is they can’t possibly know that. And history says that this particular genie, once out of the bottle, likes to stick around for a good long while.