Last week, Kevin Muir wrote a very interesting piece on debt and whether it is inflationary or deflationary. To wit:

“One of the greatest debates within the financial community centers around debt and its effect on inflation and economic prosperity. The common narrative is that government deficits (and the ensuing debt) are bad. It steals from future generations and merely brings forward future consumption. In the long run, it creates distortions, and the quicker we return to balancing our books, the better off we will all be.”

As he states, he is no fan of the Paul Krugman’s “all stimulus is good stimulus” philosophy.

Neither am I.

While I agree with the majority of Kevin’s views regarding the impact of debt on the inflation/deflation debate, I do disagree on the following point:

“Creating debt is inflationary, while paying down debt is deflationary. That’s pretty basic.

The easiest way for me to demonstrate this fact is to look at an area where debt has been created for spending in a specific area. No better example than student loans.

Over the past fifteen years, inflation in college tuition has exploded. It’s been absolutely bonkers. Here is the chart of regular CPI versus tuition CPI.”

He is correct, debt used to directly make a purchase of a service or product is inflationary.

I agree 100% with Kevin in his prognosis of how debt effects prices in the short term. However as I will explain, it is the servicing of debt (paying interest and principal) over the long run that applies deflationary pressures to the economy.

As he states this is basic.

If I have $100 then I can buy $100 worth of goods. That’s it. However, if I am able to borrow and additional $200, then I can buy $300 worth of goods. When there is more demand, due to leverage, the price of the product or service will rise.

This is what happened with student loans. When the government took over student loan debt and assured everyone that money was readily available, Universities cheered as they could raise tuition beyond what students could previously afford. The more debt that was given out, the higher tuition went.

As I have explained before there is good and bad inflation.

Inflationary pressures can be representative of expanding economic strength if it is reflected in the stronger pricing of both imports and exports as well as wages. Increases in prices would suggest stronger consumptive demand, which is 2/3rds of economic growth, and increases in wages allows for absorption of higher prices.

That would be the good.

As shown below, there has been a modest uptick in import and export prices due to the demand generated by the slate of natural disasters last year BUT prices are only back to import and export prices are currently only back to levels last seen in 2008. This isn’t surprising given the weakness in wage growth which combined suggests there is little “good” inflationary pressure presently.

The “bad”: would be inflationary pressures in areas which are direct expenses to the household. Such increases curtail consumptive demand, which negatively impacts pricing pressure, by diverting consumer cash flows into non-productive goods or services.

Take a look at where consumers are being impacted the most.

The largest areas of the CPI inflation calculation, are specifically the areas where consumers have the least amount of control. Escalating rent, utilities, food, and health care are the biggest constituents of the “non-discretionary family budget.” While consumers are spending more on these areas, the economic impact is negligible as paying more for food, rent, utilities and health care does not increase the demand for these products and services which would create stronger rates of economic growth.

Those rising costs combined with the lack of wages leaves a family little choice to fund their “standard of living.” As I discussed in “Sex, Money & Happiness:”

“The ‘gap’ between the ‘standard of living’ and real disposable incomes is more clearly shown below. Beginning in 1990, incomes alone were no longer able to meet the standard of living so consumers turned to debt to fill the ‘gap.’

However, following the ‘financial crisis,’ even the combined levels of income and debt no longer fill the gap. Currently, there is almost a $7000 annual deficit that cannot be filled.”

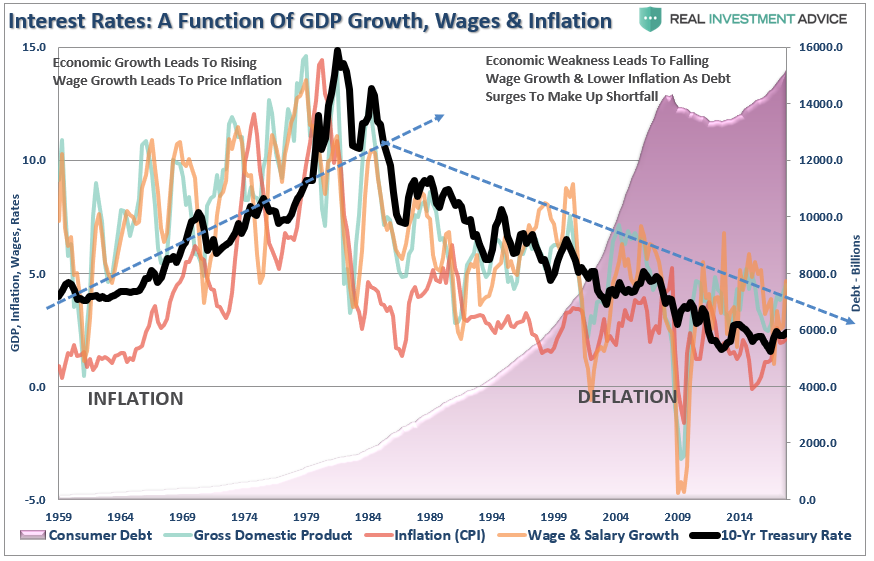

In the past, when Americans wanted to expand their consumption beyond the constraint of incomes they turned to credit in order to leverage their consumptive purchasing power. Steadily declining interest rates and lax lending standards put excess credit in the hands of every American. Such is why, during the 80’s and 90’s, as the ease of credit permeated its way through the system, the standard of living seemingly rose in America even while economic growth slowed along with incomes.

Despite seemingly increasing levels of consumption, actual inflation pressures have continued to erode as shown below.

Now, let me back up for a minute.

Kevin is correct that debt, when consumers borrow money to buy stuff (cars, houses, washers, dryers, computers)leads to a demand push of inflation in the short-term. However, the use of debt is deflationary over the long-term as debt service redirects consumptive spending into debt service. Said differently, if you buy on credit today, you must make payments tomorrow that inhibit your ability to purchase stuff.

There is simply a limit to what consumers can generate for income and to the amount of debt they can absorb.

Same Goes For Government Debt

The same goes for Government debt as well. As discussed in “The Debtors Prism:”

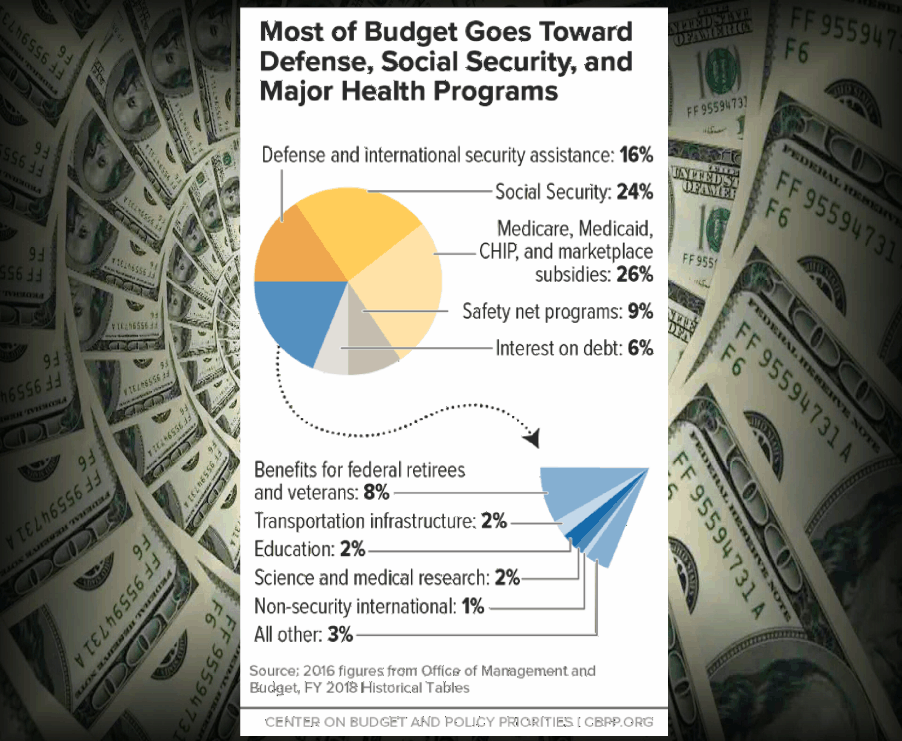

“In order for government deficit spending to be effective, the ‘payback’ from investments being made through debt must yield a higher rate of return than the debt used to fund it.

The problem is that government spending has shifted away from productive investments that create jobs (infrastructure and development) to primarily social welfare and debt service which has a negative rate of return. According to the Center On Budget & Policy Priorities, nearly 75% of every tax dollar now goes to non-productive spending.”

“In 2017, the Federal Government spent an estimated $4.3 Trillion which was equivalent to roughly 21% of the nation’s entire GDP. Of that total spending, an estimated $3.68 Trillion was financed by Federal revenues leaving $657 billion to be financed through debt. In other words, it took almost all of the revenue received by the Government just to cover social welfare programs and service the interest on the debt.”

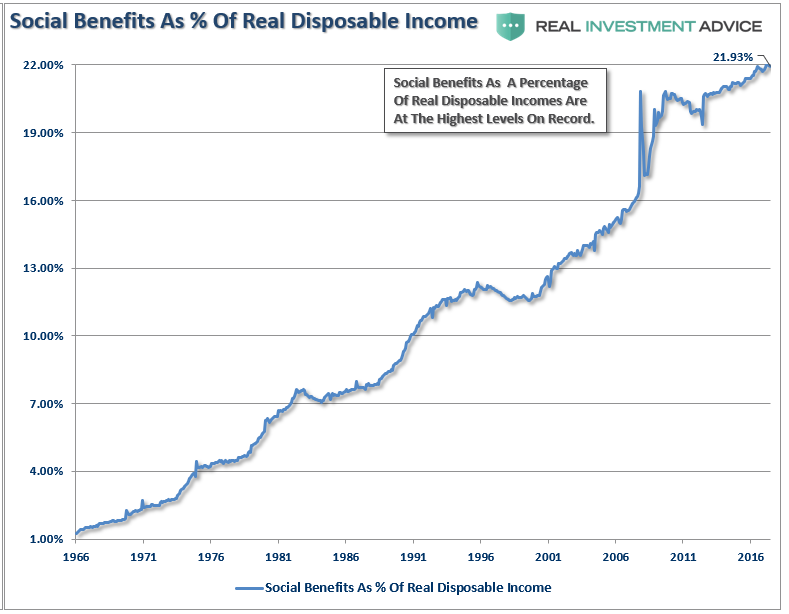

For the average person, these social benefits are critical to their survival as they make up more than 22% of real disposable personal incomes. With 1/5 of incomes dependent on government transfers, it is not surprising that the economy continues to struggle as recycled tax dollars used for consumption purposes have virtually no impact on the overall economy.

If debt was truly inflationary in the long-term, then we should actually see two things occurring.

The first would be a DECREASING level of debt to create economic growth as debt would be leveraging accelerating rates of growth. Unfortunately, it is quite the opposite as it is requiring an ever increasing level of “economic debt” to only modestly increase economic growth. Currently, it requires $3.11 of debt to create $1 of economic growth. (Note: for this exercise, “economic debt” is the combined amount of household, corporate and publicly held government debt. All data is in nominal terms)

Secondly, we should also see rising rates of inflation as debt increases. Again, we see the opposite.

The difference between the Government and households is there is no real limit on how much debt the Government can issue. But that is also why economic growth remains constrained at sub-par levels despite “hopes” of a resurgence.

Debt actually is deflationary on a longer-term basis as it acts as a “cancer” siphoning potential savings from income to service the debt. Rising levels of debt, means rising levels of debt service that reduces actual “disposable” incomes, both personal and governmental, that could be saved or reinvested back into the economy.

The mirage of economic growth has been a function of surging debt levels. “Wealth” is not borrowed,but “saved,” and this is a lesson has yet to be learned.

About the only thing that is “inflationary” about debt over the long-term is simply the amount of debt itself.

Until the deleveraging cycle is allowed to occur, and household balance sheets return to more sustainable levels, the attainment of stronger, and more importantly, self-sustaining economic growth could be far more elusive than currently imagined.

However, Kevin is absolutely correct that we will do nothing to correct the problem before “the collision” eventually occurs: To wit:

“Governments were faced with a choice during the 2008 Great Financial Crisis. Credit was naturally contracting, and the economy wanted to go through a cleansing economic rebalancing where debt would be destroyed through a severe recession. Yet, governments had practically zero appetite to allow this sort of cathartic cleansing to happen. Instead, they stepped up and stopped the credit contraction through government spending and quantitative easing.”

We had the opportunity to restore economic balance and we blew it. Of course, since fiscal conservatism left the country decades ago, there is little to stop the debt driven economy until, as Kevin put it, “the bond market takes away the keys.”

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter and Linked-In