“There is a ‘Great Divide’ happening between the near ‘depressionary’ economy versus a surging bull market in stocks. Given the relationship between the two, they both can’t be right.” – May 12th.

The optimistic view currently is that stocks have it right. Such was a point made in a recent CNBC interview with Ed Yardeni:

“The market has been a ray of sunshine. Basically investors are convinced that we’ll get out of this, and the economy will recover along with earnings. So far, that forecast seems to be working out pretty well. The economy may very well be catching up with the stock market rather than the stock market going off on its own.”

I want to come back to this point in a moment, but we need some historical context.

Relationship Between Stocks & Economy

While the media is a bit ecstatic with the markets rise, I disagree with Yardeni a bit. Historically when stocks have deviated from the underlying economy, the resolution has always been lower stock prices.

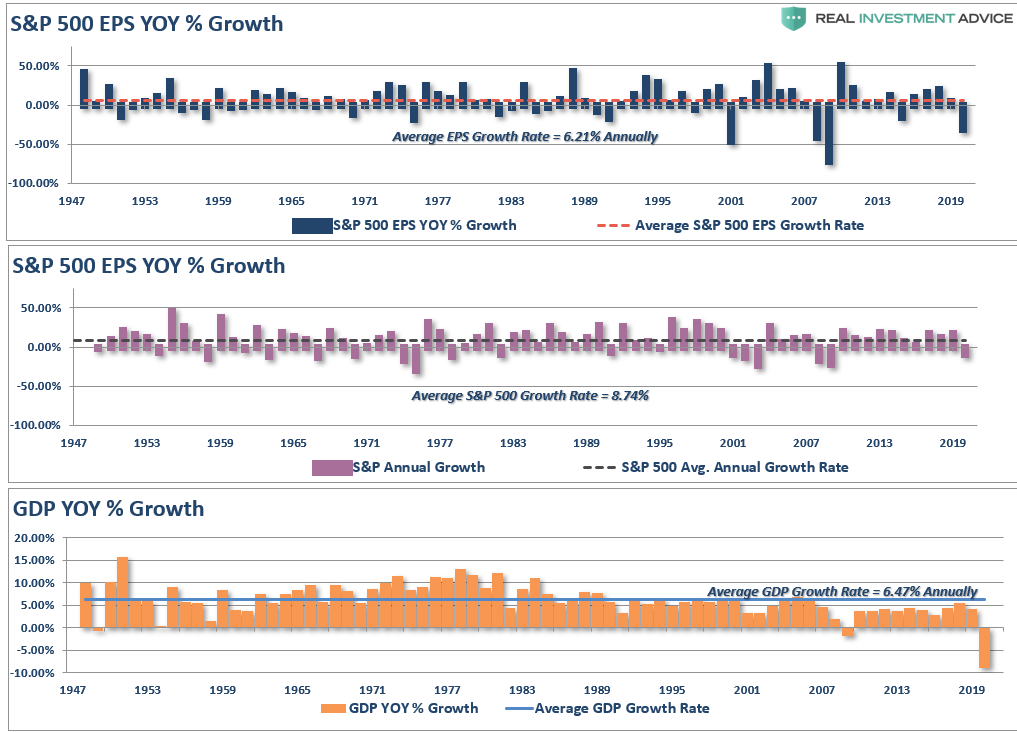

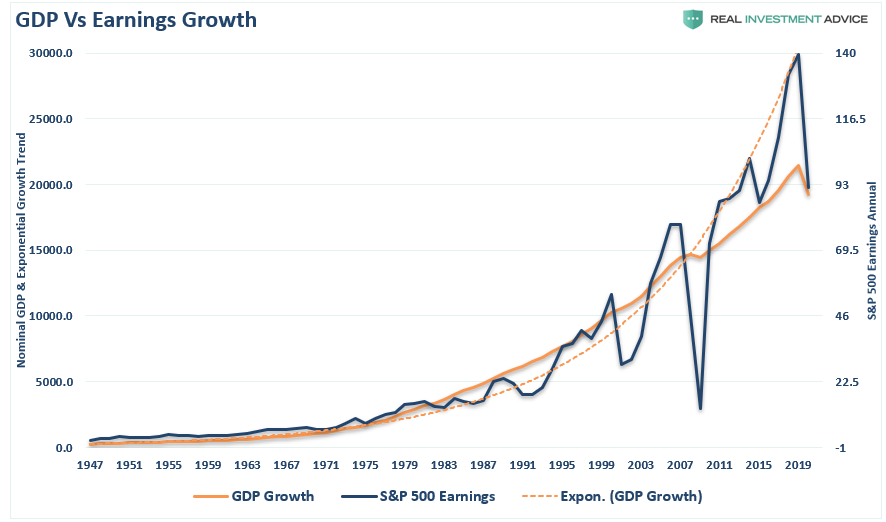

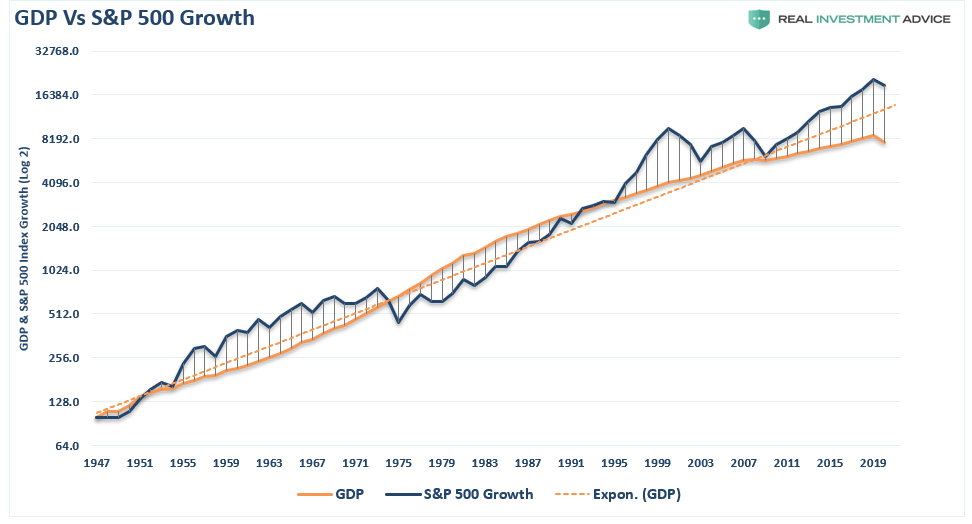

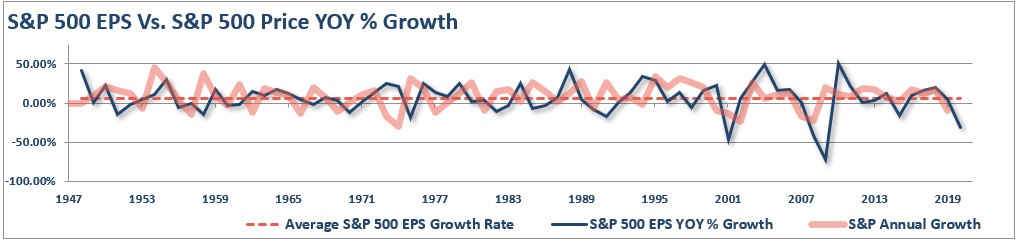

There is a close relationship between the economy, earnings, and asset prices over time. The chart below compares the three going back to 1947 with an estimate for 2020 using the latest data points.

Since 1947, earnings per share have grown at 6.21%, while the economy has expanded by 6.47% annually. That close relationship in growth rates should be logical, particularly given the significant role that consumer spending has in the GDP equation.

Stocks Vs. The Economy, Which Is Right?

While over short periods, the stock market often detaches from underlying economic activity, this is due to psychology as investors latch onto the belief “this time is different.”

Unfortunately, it never is.

While not as precise, a correlation between economic activity and the rise and fall of equity prices does remain. In 2000, and again in 2008, as economic growth declined, corporate earnings contracted by 54% and 88%, respectively. Such was despite calls of never-ending earnings growth before both previous contractions.

As earnings disappointed, stock prices adjusted by nearly 50% to realign valuations with both weaker than expected current earnings and slower future earnings growth. While the stock market is once again detached from reality, looking at past earnings contractions, suggests it won’t be the case for long.

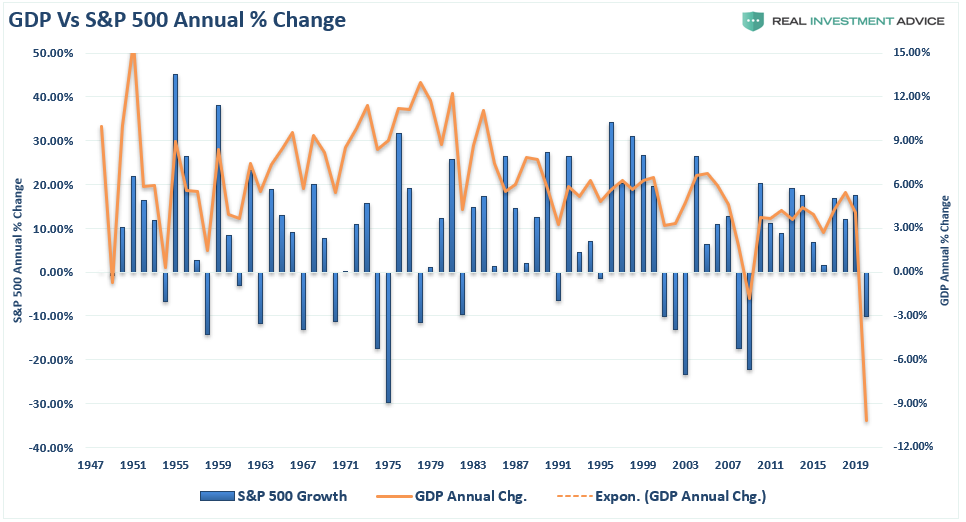

The relationship becomes more evident when looking at the annual change in stock prices relative to the yearly GDP change.

Again, since stock prices are driven in part by the “psychology” of market participants, there can be periods where markets become detached from fundamentals. However, where history disagrees with Yardeni, fundamentals never play “catch up” with stock prices.

Stocks Running Of Bad Economic Data

As Mr. Yardeni noted, the market is hopeful that the economy will quickly recover, bringing earnings growth back. Bolstering that view was last Friday’s employment report which CNBC continues to tout:

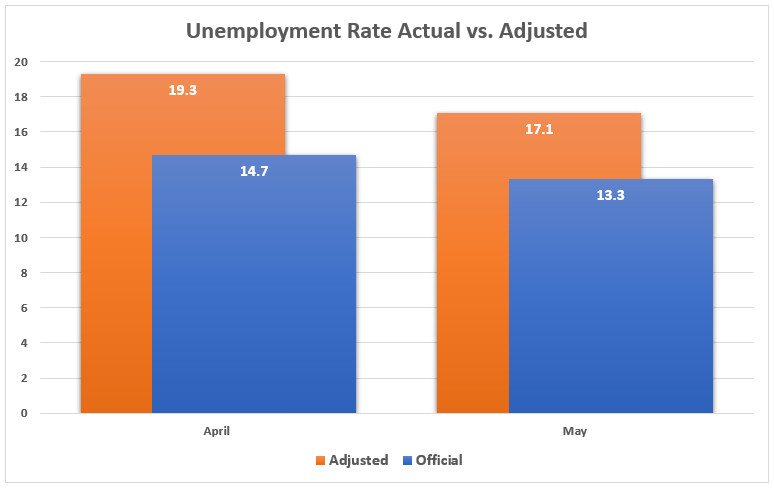

“The Bureau of Labor Statistics’ latest release trounced expectations, revealing the unemployment rate dipped to 13.3% from 14.7% while economists anticipated a jump to roughly 20%. Payrolls increased by more than 2.5 million, beating estimates for a 7.5 million decline.”

It was certainly good news at the headline. Unfortunately, the report was rife with errors that suggest the “real” unemployment rate is markedly higher.

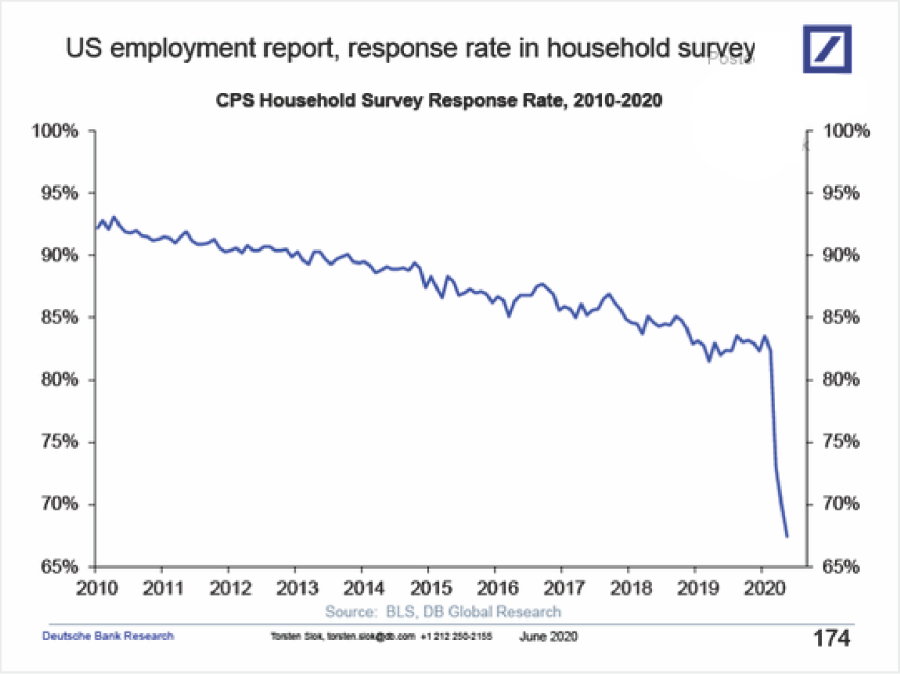

There was a significant decrease in the sample rate of households, which sharply increases the margin of error in the report.

BLS In Error

More importantly, there was a miscalculation of the data in the report:

The drop in the unemployment rate is due precisely to the substantial decrease in the labor force. Since February, according to the BLS, 6.3 million people have decided they no longer wanted to work. Such is substantially more than would be expected even based on the massive increase in unemployment.

Therefore, if we adjust for the labor force, and count the extra 4.9 million people who were “not at work for other reasons,” the “realistic unemployment rate” was 17.1 percent in May.

While that number is down from April, it is still higher than any other unemployment rate in over 70 years. (But the 13.3% number was as well.)

“There were also a large number of workers classified as employed but absent from work. As was the case in March and April, household survey interviewers are instructed to classify employed persons absent from work due to coronavirus-related business closures as unemployed on temporary layoff.

However, not all such workers were so classified.

If the workers were classified as unemployed on temporary layoff, the overall unemployment rate would be about 3 percentage points higher than reported (on a not seasonally adjusted basis).

If we make the proper adjustments to the unemployment rate for both April and May, it reveals the ugly truth.

In other words, the unemployment rate was 16.3% using their data, which suggests the number of unemployed is closer to 26 million.

If my numbers are close to correct, there will be implications to earnings and profits.

One Time Bump May Fade Quickly

Furthermore, there is a difference between a one-time bump and an economic recovery based on growing economic activity.

“The labor market data suggested an economic recovery is arriving sooner than expected and revived hopes for a V-shaped trendline for gross domestic product.” – Yardeni

While “hope” is high, the virus is behind us, there will be no “second-wave,” a vaccine will be available by year-end, and more stimulus is on the way; there are many issues which can go wrong. Like this:

I am certain the economy will not be “locked down” a second time regardless of the severity of the outbreak. Politicians have learned their lesson. As Steve Mnuchin said on Thursday:

However, the risk is a secondary infection will deter consumers from returning to the economy.

The partial reopening of the economy did lead to some hiring last month, but going from zero staff to a skeleton crew with a limited opening is one thing. Getting back to full-employment, which will require substantially increased demand, is quite another.

Importantly, the government’s Paycheck Protection Program (PPP) certainly boosted employment in May. However, while the program “encouraged businesses to keep people on payroll,” if demand doesn’t return before the money runs out, layoffs will rise.

JOLTS May Have It

Looking at the latest Job Opening and Labor Turnover Survey (JOLTS), openings continue to decline suggesting the initial rehiring may be a one-time bump.

The same was the case in the areas that saw the biggest jumps in employment last month. In other words, businesses have rehired the workers they need, but may not be hiring any more for a while.

Such was further confirmed by another 1.5 million individuals filing for initial unemployment claims last week. While initial claims from unemployment are falling, such is expected as employers reach the limits of staffing needed to remain in business. However, these numbers could rise as the wave of forthcoming bankruptcies ensue and PPP ends.

Economy May Disappoint

“We’ve been talking about the ‘V’ — this is better than a ‘V’. This is a rocket ship.” – President Trump

“Real GDP could be down 40% to 50% in the second quarter. But the worse it is in the second quarter, the greater the likelihood we’ll see something like a 20% increase in the third quarter.” – Yardeni.

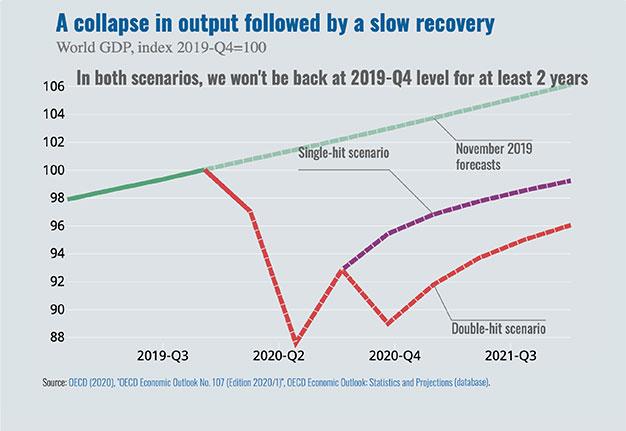

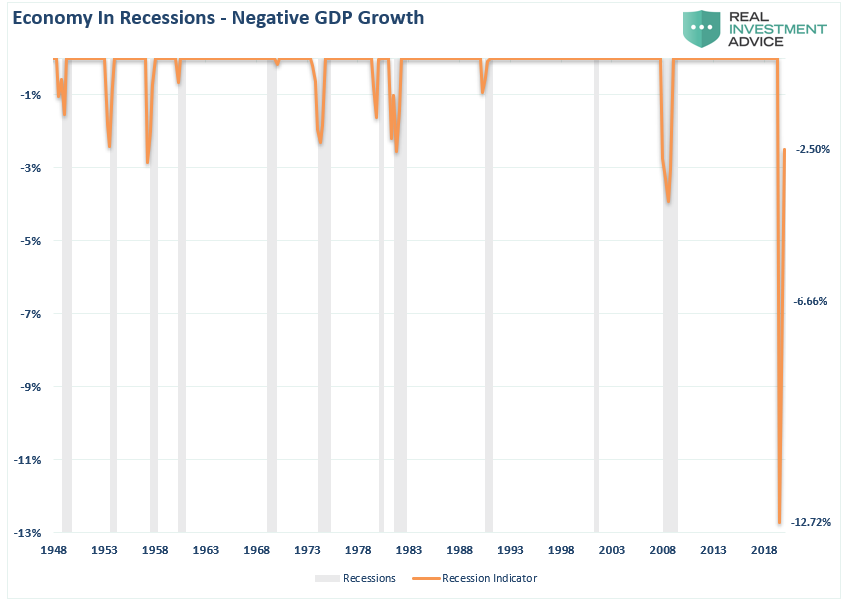

The COVID-19 pandemic has triggered one of the most severe global recessions in nearly a century and will leave the world scarred for years. Such was the warning from the Organization for Economic Cooperation and Development (OECD) on Wednesday.

Their warning, based upon the expectations of a “second-wave” of the virus, would derail the initial economic bounce. The OECD offered two forecasts for global growth:

- The assumption a second wave of the coronavirus arrives in the back half of 2020; and,

- A strict social distancing measures is enough to avoid the emergence of new virus cases and deaths.

The OECD forecasts global growth will plunge by 7.6% in 2020, and “remain well short” of its growth activity levels from 2019, suggesting no V-shaped recovery. If a second wave can is avoided, the world economy will contract by 6% in 2020, and again fail to recover to pre-corona levels by the end of 2021.

The OECD makes the case for either a “Nike Swoosh” or a “W-shaped” recovery. Both are well short of current expectations, but align with our analysis from last week:

Recovery To Nowhere

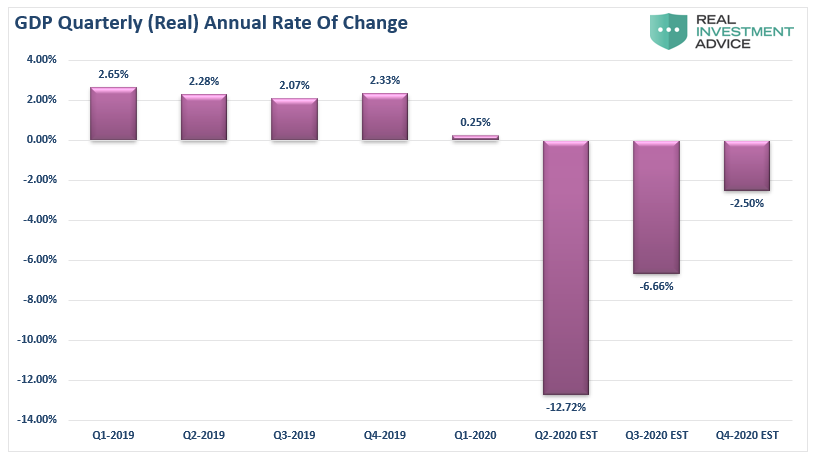

“However, the “return to economic normality” faces immense challenges. High rates of unemployment, suppressed wages, and elevated debt levels, makes a “V-shaped” recovery unlikely.

Such is where the “math” becomes problematic. A 50% drawdown in Q2, requires a 100% recovery to return to even. In the more optimistic recovery scenario detailed above, two-quarters of record recovery rates still leave the economy running in a deep recession.”

“Even if the economy achieves high recovery rates, it won’t change the recession. The resulting 2.5% economic deficit will remain one of the deepest in history.”

While such a recovery would be welcomed, it is not enough to support stronger employment, wage growth, or corporate earnings.

Here is the issue missed by the majority of mainstream economists.

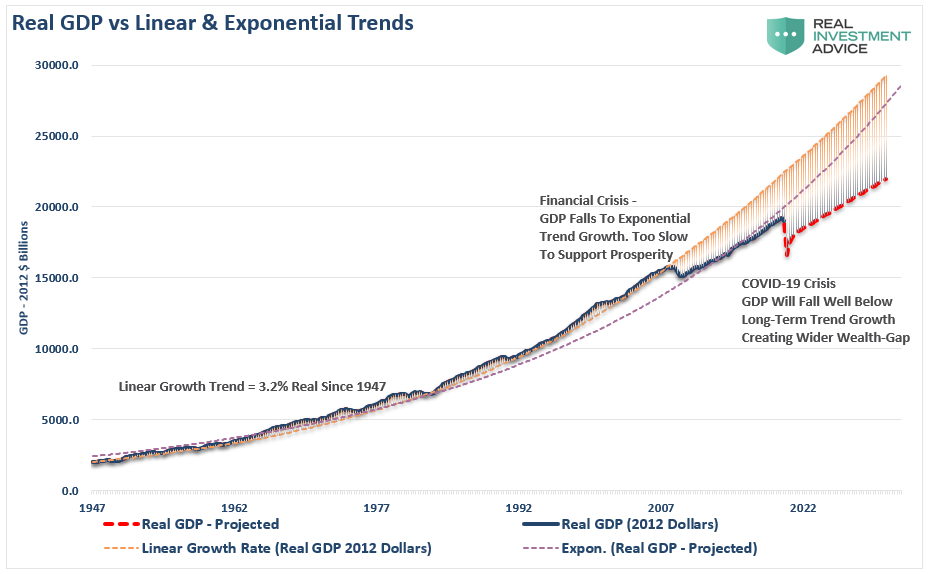

“Before the “Financial Crisis,” the economy had a linear growth trend of real GDP of 3.2%. Following the 2008 recession, the growth rate dropped to the exponential growth trend of roughly 2.2%. Instead of reducing the debt problems, unproductive debt, and leverage increased.”

If our analysis is correct, which agrees with the OECD and the World Bank, such would suggest President Trump’s pumping of a V-shaped recovery is overly optimistic. Importantly, the markets may suffer disappointment as expectations fall short.

The Stock Market Isn’t The Economy

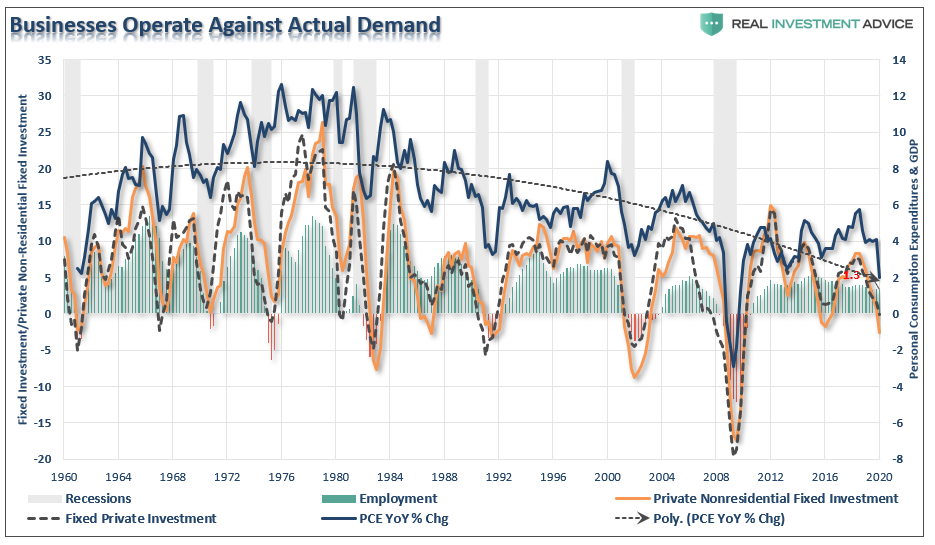

The economic destruction playing out in real-time will eventually weigh on markets. There is a negative feedback loop between employment and consumption. As unemployment rises, consumption falls due to a lack of income. Since businesses operate based on demand for goods and services, the correlation between PCE, fixed investment, and employment are high.

As noted, even with the reopening of the economy, businesses will not immediately return to full operational activity, until consumption returns to normalized levels. Such will frustrate policy-makers and the Fed.

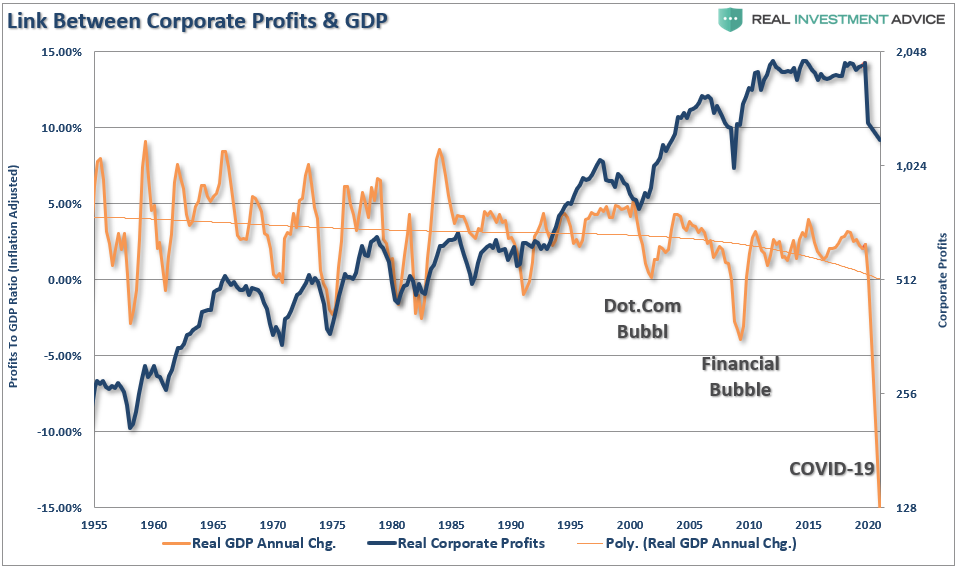

Profits To GDP

It isn’t just the economic data that will be horrid over the next few months, but earnings will likely be just as bad. Earnings can not live in isolation from the economy. As shown below, corporate profits ebb and flow with economic activity.

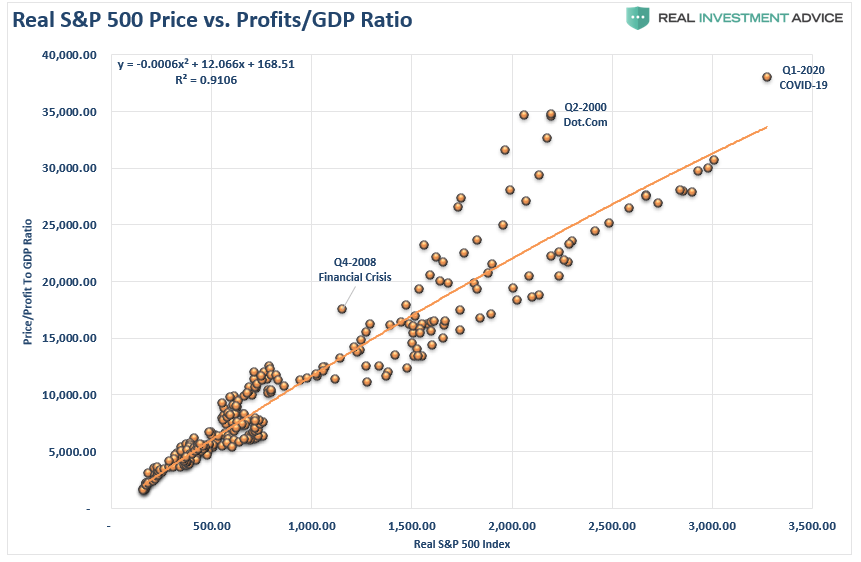

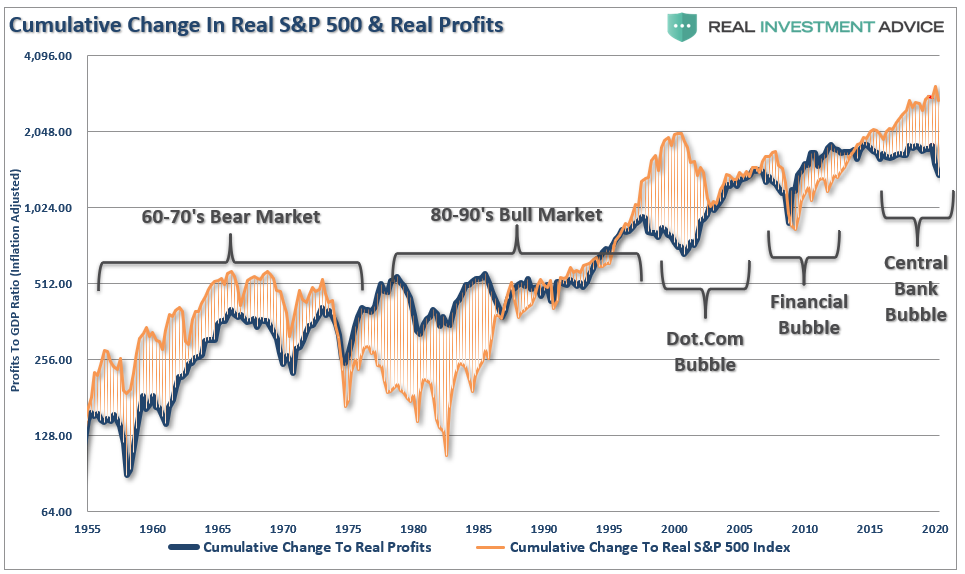

You shouldn’t dismiss the fact markets are deviated from long-term earnings. Historically, such deviations don’t work out well for overly “bullish” investors. The correlation is more evident when looking at the market versus the ratio of corporate profits to GDP.

Again, since corporate profits are ultimately a function of economic growth, the correlation is not unexpected. Hence, neither should the impending reversion in both series.

The detachment of the stock market from underlying profitability guarantees poor future outcomes for investors. But, as has always been the case, the markets can certainly seem to “remain irrational longer than logic would predict.”

However, such detachments never last indefinitely.

“Profit margins are probably the most mean-reverting series in finance, and if profit margins do not mean-revert, then something has gone badly wrong with capitalism. If high profits do not attract competition, there is something wrong with the system, and it is not functioning properly.” – Jeremy Grantham

Reversions Happen Fast

There are a tremendous number of things that can go wrong in the months ahead. Such is particularly the case of surging stocks against a depressionary economy.

While investors cling to the “hope” that the Fed has everything under control, there is more than a reasonable chance they don’t.

Regardless, there is one truth about stocks and the economy.

“Stocks are NOT the economy. But the economy is a reflection of the very thing that supports higher asset prices – corporate profits.”