by Troy

Last week we explained why the market’s short term outlook is bearish. The stock market is now making a pullback, and trade war news isn’t helping bulls. Over the past year, tariff-related news has not been good for stocks in the short term.

- Technicals (short term, next 1-3 months): mixed

- Technicals (medium term, next 6-9 months): mostly bullish

- Fundamentals (long term): no significant U.S. macro deterioration, but the long term risk:reward doesn’t favor bulls.

Technicals: Short Term & Medium Term

*For reference, here’s the random probability of the U.S. stock market going up on any given day, week, or month.

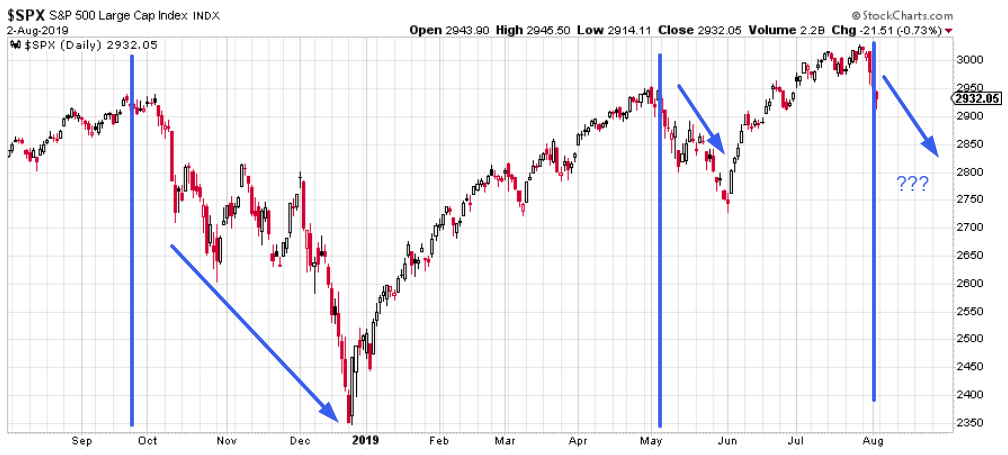

Quick reversal

The S&P has fallen 5 days in a row immediately after reaching an all-time high.

While this doesn’t necessarily mean that the stock market’s bottom is in, these quick pullbacks are usually followed by gains over the next 2 months. In the past, the S&P was higher 83% of the time 2 months later.

VIX

We’ve been looking for a VIX spike over the past 2 weeks. After spiking over the past 2 days, it’s easy to spot something out of place on the scoreboard. Stocks fell today while VIX did not go up.

This tends to happen near a top for VIX:

- When the stock market first starts to fall, VIX tends to explode. E.g. if the S&P falls -1%, VIX can rally 15-20%.

- After the stock market falls for a few days, VIX’s gains become more tempered. E.g. if the S&P falls -1%, VIX might only go up another 5%.

Here’s what happened next to VIX when the S&P fell more than -0.7% in one day, while VIX fell more than -1%.

We can be more specific and only examine cases that occurred after VIX set a 1 month high.

Here’s what happened next to the S&P

Overall, this is short term bearish for VIX and short term bullish for stocks.

Breadth

The stock market dropped quickly over the past few days. As a result, the % of S&P stocks above their 50 ema has also dropped quickly. It went from more than 80% to less than 45% in just 3 weeks.

In the past, such a quick drop in the % of S&P stocks above their 50 dma was usually followed by a stock market rally over the next few weeks.

Basic trends

The S&P fell below its 20 dma and is sitting on its 50 dma.

From a basic trend following perspective:

- Short term trend followers would NOT be long stocks right now.

- Medium & long term trend followers would still be long stocks right now

Speaking of long term trends, the S&P’s monthly MACD histogram has turned positive after being negative for more than half a year.

Historically, this was bullish for the S&P over the next 1-2 years.

Sentiment

AAII isn’t the best sentiment indicator, but it is a popular one. Bullish sentiment is rising. AAII Bulls has exceeded 38% for the first time in 11 weeks.

Rising Bullish % was mostly bullish for stocks 1 year later.

Considering all the above short term bullish factors, why don’t I have confidence in being outright short term bullish?

- There has been no selling exhaustion. (It’s hard to have selling exhaustion when the S&P is just 3% off its peak).

- The short term is always hard to predict, no matter how much confidence you have.

Here’s an example of a bearish factor to consider.

Put/Call

The Put/Call ratio is trending higher now that stocks are falling. The Put/Call ratio is now more than 15% above its 200 dma, for the first time since May.

In the past, these “first Put/Call spikes” could lead to more selling over the next 1-2 weeks.

Seasonality

From a seasonality perspective, the stock market has entered into a weaker period of the year. I would consider seasonality to be of tertiary importance.

Fundamentals (is it a bull market or a bear market?)

Will the bull market resume after this pullback/correction? That depends on the economy. The stock market & economy move in the same direction in the long run.

- If the economy continues to improve over the next few months, then the stock market’s rally will probably continue into 2020.

- But if the economy deteriorates significantly over the next few months, then we will be long term bearish for 2020.

There are various pockets of macro weakness right now, but there is no significant deterioration. Absent significant deterioration, stocks tend to go up. Let’s recap some of the leading macro indicators we covered by beginning with the bad news:

Housing is still a weak point

Housing – a key leading sector for the economy – remains weak. Housing Starts and Building Permits are trending downwards while New Home Sales is trending sideways. In the past, these 3 indicators trended downwards before recessions and bear markets began.

Personally, I am not extremely worried about the weakness in housing right now. But if this deterioration continues for another few months, then I would be much more worried.

Yield curve

The 10 year – 3 month yield remains inverted for the 11th week in a row.

In the past, this wasn’t too good for stocks over the next year.

Manufacturing

Manufacturing-related data remains weak. This is probably related to the ongoing trade war. The latest ISM manufacturing PMI fell to 51.2

It’s easy to automatically assume that this is bearish for the stock market. Here’s what happened next to the S&P when ISM manufacturing PMI fell to 51.2 in the past.

ISM readings of 51.2 still indicate expansion (any reading above 50 = expansion). It’s better to wait for a multi-month reading below 50 before considering manufacturing to be a clear bearish sign for stocks. Manufacturing has too many false bearish signals.

Now onto the good news.

Labor market is still a positive factor

The labor market is still a positive factor for macro. Initial Claims and Continued Claims are trending sideways. In the past, these 2 leading indicators trended higher before bear markets and recessions began.

Financial conditions

Financial conditions remain very loose. In the past, financial conditions tightened before recessions and bear markets began.

Here’s the Chicago Fed’s Financial Conditions Credit Subindex

Here’s banks’ lending standards. Whereas lending standards remain loose today, they tightened significantly before the previous 2 bear markets and recessions.

Delinquency Rates

Delinquency rates continue to trend downwards. In the past, this indicator trended upwards before recessions and bear markets began.

Heavy Truck Sales

Heavy Truck Sales is still trending upwards. In the past, Heavy Truck Sales trended downwards before recessions and bear markets began.

Retail Sales

Inflation-adjusted Retail Sales are still trending upwards. This is different from the previous 2 bear markets and recessions, which were preceded by flattening real Retail Sales.

Long term (risk:reward)

And lastly, I would like to touch upon risk:reward from a long term perspective. The economic expansion and bull market are late-cycle. Even if stocks keep going up over the next 1-2 years, I don’t think the bull market will last another 3-5 years.

For example, here’s the Goldman Sachs’ Bull/Bear Indicator.

From 1953 – present, there have been 162 months with Bull/Bear readings above 0.7

When this happened in the past, the S&P’s average gain over the next 2-5 years was negative.

Meanwhile, the Conference Board’s Consumer Confidence is still very high.

Consumer Confidence’s latest reading exceeded 135. There are only 3 other periods with such high Consumer Confidence:

- January-August 1998

- May 1999-November 2000

- September-October 2018

The Fed cut rates this week. Late-cycle rate cuts aren’t very good for stocks from a long term perspective.