By Wolf Richter for WOLF STREET:

The lockdown regime has changed the once booming housing market. Real estate businesses, such as real estate brokers, mortgage brokers, and other types of businesses, and the government offices that make it all work are now considered “essential businesses” under federal guidelines and under California lockdown rules. Social distancing must still be observed. But deals can be made.

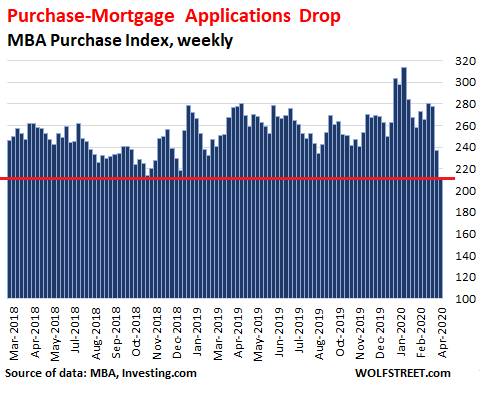

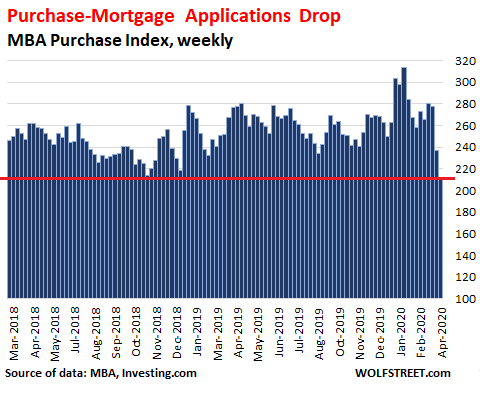

The first glimpse of what the new housing market might look like is provided by a weekly report on the number of mortgage applications by the Mortgage Bankers Association. Today, the MBA released the results for the week ended March 27: Across the US, mortgage applications to purchase a home plunged by 24% from the equivalent week a year ago. Since the multi-year peak in January, purchase-mortgage applications have plunged by one-third:

This is now the second week that mortgage applications have started to reflect the new reality of lockdowns and social distancing. Last week, the MBA reported that purchase-mortgage applications across the US had dropped 15% from a year ago. At the time, the first lockdowns weren’t fully reflected yet as they’d become effective during the last part of that reporting week.

Since then, we got blasted by the first report under the lockdown reality of initial unemployment claims, which had spiked to a horrid 3.28 million, nearly five times the prior record. All this goes together.

In states where lockdowns started first – there were kicked off in the San Francisco Bay Area – the year-over-year plunge in purchase-mortgage applications was the most severe:

- California: -36.4%

- New York: -35.6%

- Washington: -32.5%

And this is happening despite the lowest average mortgage rates in the MBA’s survey data. During the reporting week, the average contract rate for 30-year fixed-rate mortgages fell back to 3.47%.

“The bleaker economic outlook, along with the first wave of realized job losses reported in last week’s unemployment claims numbers, likely caused potential homebuyers to pull back,” the MBA’s report said.

“Buyer and seller traffic – and ultimately home purchases – will also likely be slowed this spring by the restrictions ordered in several states on in-person activities,” the report added.

So, in many markets, it means no open houses. Face-to-face closings are to be avoided. The business still operates with paper documents and lawyers watching over signings, etc. So closings are now tough. But exchanging signed documents through car windows in a parking lot is OK. Under the pressure of social distancing, the doors have opened to modern document technology. In theory, homes can be sold, and mortgages can be written, but it’s now a different ballgame.

“In the past two weeks, there has been a seismic shift in the mortgage lending world that will affect housing greatly,” mortgage broker Dan Draitser told me. And he went on:

“All of those exotic loan programs, such as bank-statement for income and stated-income and lower-credit score programs have all ceased. Done!

“All investors buying that paper are gone! No one remains.

“Lenders are tightening up loan quality for government loans, such as FHA and VA loans. And for conventional loans as well.

“Now it’s higher credit scores, more down, lower debt to income ratios.

“Nobody has any taste for any risk at the moment.

“It is a quickly changing market with everything reverting to low-risk quality loans, which leaves credit extension limited.

“‘Non-QM,’ or basically any loan outside of Fannie, Freddie, FHA and VA, is toast. No longer exists. Being felt industry wide.”

But he was working hard for the wrong reasons: “My transactions are taking three times as much time and effort to get done due to the environment, both refi & purchase.”

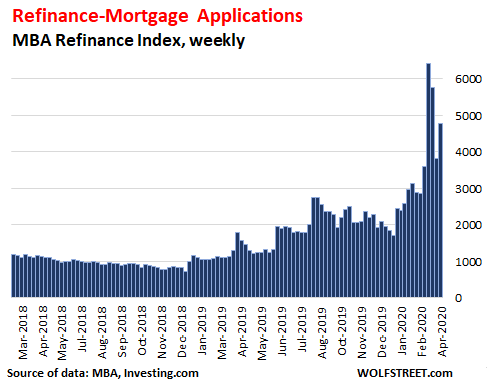

Mortgage applications to refinance existing mortgages (refis) spiked spectacularly over the past few weeks, hitting the highest level since 2003, as mortgage rates plunged. But then turmoil in the market for mortgage-backed securities briefly drove up mortgage rates, despite the Fed having cut its policy rates to near-zero; and refi applications plunged. But during the week reported today, as mortgage rates dropped to historic lows again, refi applications jumped again:

This data is based on weekly surveys by the MBA that covers 75% of all US retail residential mortgage applications at nonbanks, banks, and thrifts. Mortgage applications are not an indicator of demand by non-resident foreign investors or large domestic investors since they can obtain funding elsewhere. But they’re an early indication of local demand by regular folks.

This demand had been strong all last year and earlier this year. But it is now spiraling down. And as mortgage broker Draitser pointed out, the entire risk environment on the lending side has suddenly changed – with risky loans, which were a considerable part of the business, having been pushed off the table.