Wolf Richter wolfstreet.com, http://www.amazon.com/author/wolfrichter

And its eerie exhortations to the banks to prepare for a downturn to avoid “undue disruption to the financial system.”

The FDIC’s quarterly report on commercial banks and savings institutions was cited in the media mostly for the $56 billion in profits that FDIC-insured commercial banks and savings institutions made in the first quarter, which was up 27% from a year ago. An estimated $6.6 billion of the profits were due to the tax-law changes.

It remained mostly unmentioned that this increase in profits came after the huge charge-offs banks took in the fourth quarter mostly due to write-downs of tax assets, also a result of the new tax law. These write-downs slashed bank profits in Q4 to $25 billion, the worst quarter since the Great Recession.

Overall, Q1 was really exciting. Banks were firing on all cylinders, according to the FDIC: Net income jumped, loan balances rose, net interest margins improved, and the number of “problem banks” edged down. But worries are creeping up:

The interest-rate environment and competitive lending conditions continue to pose challenges for many institutions. Some banks have responded by “reaching for yield” through investing in higher-risk and longer-term assets.

Going forward, the industry must manage interest-rate risk, liquidity risk, and credit risk carefully to continue to grow on a long-run, sustainable path.

The industry also must be prepared to manage the inevitable economic downturn, whenever it comes, smoothly and without undue disruption to the financial system.

I added the bold. This is a goodie. We had an “undue disruption to the financial system” during the last downturn, and we don’t want another one, the FDIC says.

“Undue disruption” would be when banks stop lending. That’s when credit freezes up in a credit-dependent economy. Everything comes to a halt. Paychecks start bouncing. So, don’t do that again.

The long-term objective for banks should be to position themselves during periods of good economic and banking conditions, as exist today, to be able to sustain lending through the economic cycle so that the industry can play a counter-cyclical role, and not a pro-cyclical role as occurred during the financial crisis.

“Pro-cyclical role” means banks made things worse during the last downturn. So don’t do that again, it says.

These warnings about the end of the credit cycle don’t come out of the blue. We have seen in other data that defaults in subprime auto loans and subprime credit card loans are already surging. Those are early flags that the credit cycle has entered the next phase.

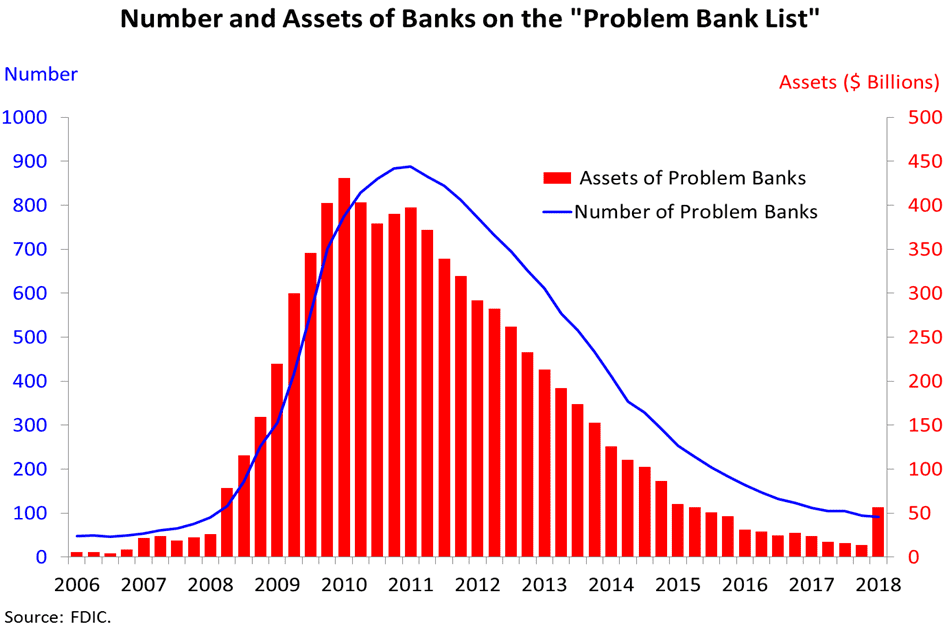

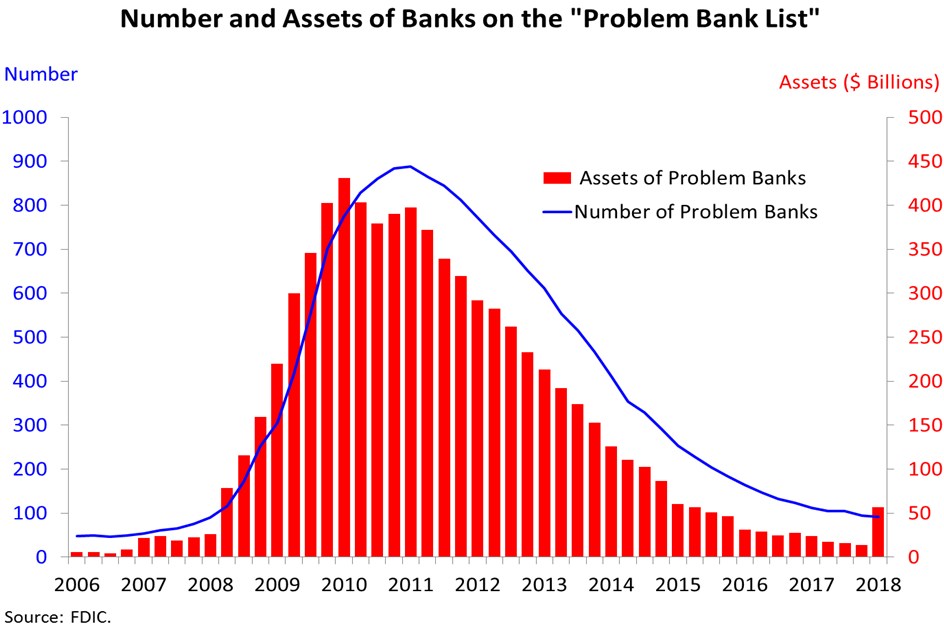

The FDIC also reported that the total number of banks on its “Problem Bank List” declined by 3 to 92 banks. Which banks are on the list is a secret. It said that three institutions were added to the list. Thus, five must have made if off the list. None of the banks toppled in Q1, which is a good thing, after six bank failures in 2017 and five failures in 2016. All this is benign compared to the 148 bank failures in 2009 and 157 bank failures in 2010, or the 534 failures in 1989.

And then comes “Chart 8” in the FDIC’s presentation, which depicts the nicely behaved number of banks on the FDIC’s “Problem Bank List” (blue line, left scale), and the red bars… OOPS! The “Assets of Problems Banks” (right scale) more than tripled in the quarter to $60 billion:

This doesn’t mean the financial system is going to collapse in Q2. But it does show that the three new banks that were added to the “Problem Bank List” were bigger banks with a lot more assets. This is the same kind of jump seen in 2008.

It confirms the other early indications that the credit cycle has definitely moved on to the next phase. The FDIC is not oblivious to it, and its risks:

[A]n extended period of low interest rates and an increasingly competitive lending environment have led some institutions to reach for yield. This has led to heightened exposure to interest-rate risk, liquidity risk, and credit risk.In addition, with the current expansion in its latter stage, the industry needs to be prepared to manage the inevitable downturn, whenever it may occur, in order to avoid financial system disruption and sustain lending through the economic cycle.

I added the bold. The FDIC just cannot stay away from the phrase, “avoid financial system disruption.”