BY ROBERT ROSS

I’m not buying the dip in stocks—and neither should you.

Let me explain…

On December 24, the S&P 500 slid to its lowest level since 2017. The index has since rebounded 6.9%.

Investors passed this off as a sign the correction is over. This is wishful thinking.

The main worry behind this sell-off was higher interest rates. But they have only just started to take effect on the economy.

Since December 2015, the Fed has hiked six times. They signal two more times this year.

That tells me there is more danger ahead for stock investors.

Higher Rates Are Bad News for Stocks

When interest rates are low, money is cheap. Businesses borrow money and expand at a small cost.

Conversely, when rates are higher, it costs more to a run a company. This lowers a company’s earnings and drags down its stock price.

A study from Bridgeway Capital Management showed that after interest rates fall, the long-term average return on the S&P 500 is 13.3%.

Meanwhile, when interest rates rise, the S&P 500 return is almost half that figure.

Rising interest rates are not kind to stocks. That’s a fact. And businesses addicted to cheap credit will be even worse off.

REITs Have a Target on Their Backs

Some of the most vulnerable industries today are:

- Utilities,

- pipeline master limited partnerships,

- and perhaps most of all, Real Estate Investment Trusts (REITs)

REITs are known for paying generous dividends. Many of them offer yields of 6% or more.

That looks very tempting. But owning a REIT can be dangerous when rates are rising.

The thing is, they won’t be able to pay those tempting dividends much longer.

Here’s why.

REITs own and operate income-producing real estate. These properties range from apartment buildings to hospitals, shopping centers, and hotels.

An REIT grows its business by borrowing money and buying more property.

Herein lies the problem.

Caught in the Rising Rate Crossfire

When interest rates are low, an REIT’s finance costs are lower and its profits are higher. That enables it to pay a fat dividend.

When interest rates were low, REITs performed great.

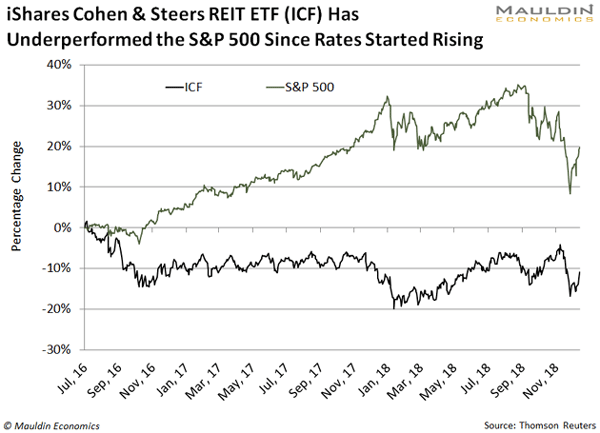

From January 2009 to December 2015, interest rates were at their lowest levels ever. During this period, the iShares Cohen and Steers REIT ETF (ICF) handed investors a 164.7% return.

It beat the S&P 500 return of 138.5%.

But times have changed.

The Fed ended cheap credit in December 2015. And just like that, REITs have lagged the S&P 500:

Even with the steep sell-off last month, the S&P 500 is still up 18.6%. Meanwhile, the iShares Cohen and Steers REIT ETF has lost 11.4%.

The good old days of low interest rates won’t come back anytime soon. I expect REITs will continue to perform poorly in today’s already rocky market.

That’s why I’ll steer clear of REITs. And if I were you, I’d do the same.

Instead, I’ll add companies—like Coca-Cola—that don’t need cheap money to stay afloat.

Coca-Cola Is a Classic All-Weather Stock

The famed beverage maker of Coca-Cola, Sprite, Vitaminwater, and Minute Maid doesn’t rely on low interest rates to stay afloat.

Heck, Coca-Cola has enough cash in the bank to fund its business for two years. And it can do so without any additional revenue.

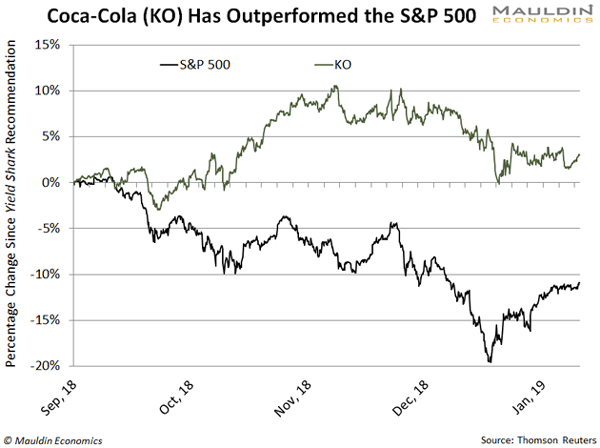

I recommended my readers buy Coca-Cola (KO) on September 25, 2018.

Since then, the S&P 500 has been crushed over 11%.

Meanwhile, Coca-Cola has actually gained 3.9%:

Coca-Cola is immune to rising rates. And the strength of its shares during the recent sell-off proves it.