Authored by Lance Roberts via RealInvestmentAdvice.com,

Last week, President Trump nominated Judy Shelton to a board seat on the Federal Reserve. Shelton has been garnering a lot of “buzz” because of her outspoken and alternative stances, including “zero interest rates” and a “gold standard” for the U.S. dollar.

But, Shelton is full of inconsistent and incongruous views on monetary policy. For instance, in 2017 she stated:

“When governments manipulate exchange rates (by changing interest rates) to affect currency markets, they undermine the honest efforts of countries that wish to compete fairly in the global marketplace. Supply and demand are distorted by artificial prices conveyed through contrived exchange rates. Businesses fail as legitimately earned profits become currency losses,”

In short, when the Fed, or any central bank/government, lowers or raises interest rates it directly affects the currency exchange rates between countries and, ultimately, trade.

However, when recently asked on her views about whether the Fed should cut rates to boost economic growth, she said:

“The answer is yes.”

So, the U.S. should lower rates as long as it is beneficial for the U.S., but no one else should be allowed to do so because it is “unfair” to U.S. businesses.

Hypocritical?

This is also the same woman who supports a return to the “gold standard” for the U.S. dollar. With a limited supply of gold and a massive level of global trade based on the U.S. dollar reserve system, the value of the dollar would skyrocket effectively collapsing the entire global trade system. Zero interest rates and “gold back dollar” can not co-exist.

Shelton’s nomination by Trump is not surprising as he has been lobbying the Fed to cut rates in the misguided belief it will support economic growth. Shelton, who has been supportive of Trump’s views, recently stated her support to the WSJ which again shows her ignorance as to the actual workings of the economy.

“Today we are seeing impressive gains in productivity, which more than justify the meaningful wage gains we are likewise seeing—a testimonial to the pro-growth agenda. The Fed’s practice of paying banks to keep money parked at the Fed in deposit accounts instead of going into the economy is unhealthy and distorting; the rate should come down quickly as the practice is phased out.”

Well, this is the point, as we say in Texas, “We call Bulls**t.”

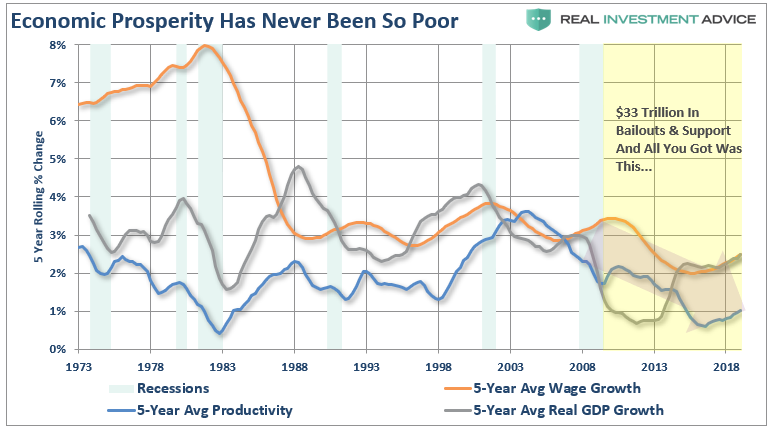

As shown, the U.S. is currently running at lower levels of GDP, productivity, and wage growth than before the last recession. While this certainly doesn’t confirm Shelton’s analysis, it also doesn’t confirm the conventional wisdom that $33 Trillion in bailouts and liquidity, zero interest rates, and surging stock markets, are conducive to stronger economic growth for all.

However, what the data does confirm is the Fed is caught in a “liquidity trap.”

The Liquidity Trap

Here is the definition:

“A liquidity trap is a situation described in Keynesian economics in which injections of cash into the private banking system by a central bank fail to lower interest rates and hence fail to stimulate economic growth. A liquidity trap is caused when people hoard cash because they expect an adverse event such as deflation, insufficient aggregate demand, or war. Signature characteristics of a liquidity trap are short-term interest rates that are near zero and fluctuations in the monetary base that fail to translate into fluctuations in general price levels.”

Let’s take a moment to analyze that definition by breaking it down into its overriding assumptions.

There is little argument that Central Banks globally are injecting liquidity into the financial system.

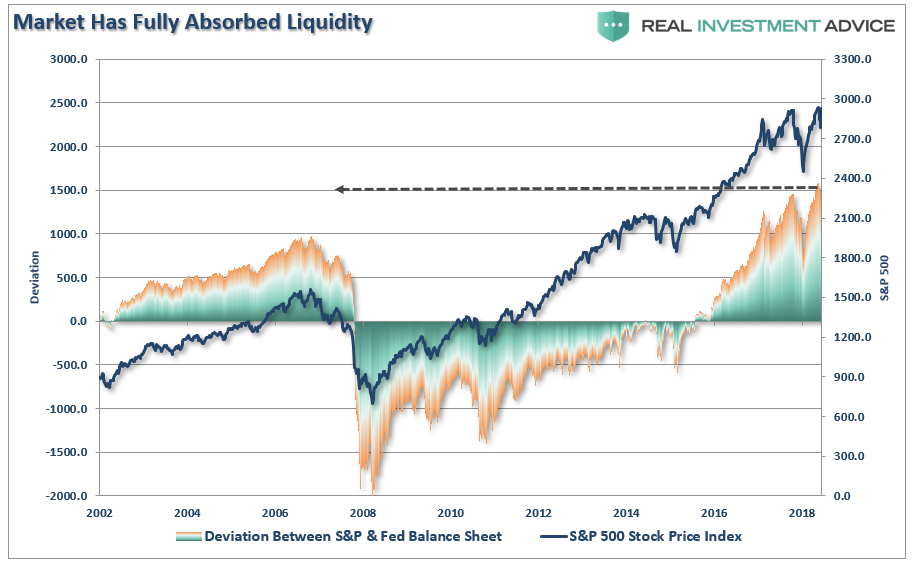

However, has the increase in liquidity into the private banking system lowered interest rates? That answer is also “yes.” The chart below shows the increase in the Federal Reserve’s balance sheet, since they are the “buyer” of bonds, which in turn increases the excess reserve accounts of the major banks, as compared to the 10-year Treasury rate.

Of course, that money didn’t flow into the U.S. economy, it went into financial assets. With the markets having absorbed the current levels of accommodation, it is not surprising to see the markets demanding more, (The chart below compares the deviation between the S&P 500 and the Fed’s balance sheet. That deviation is the highest on record.)

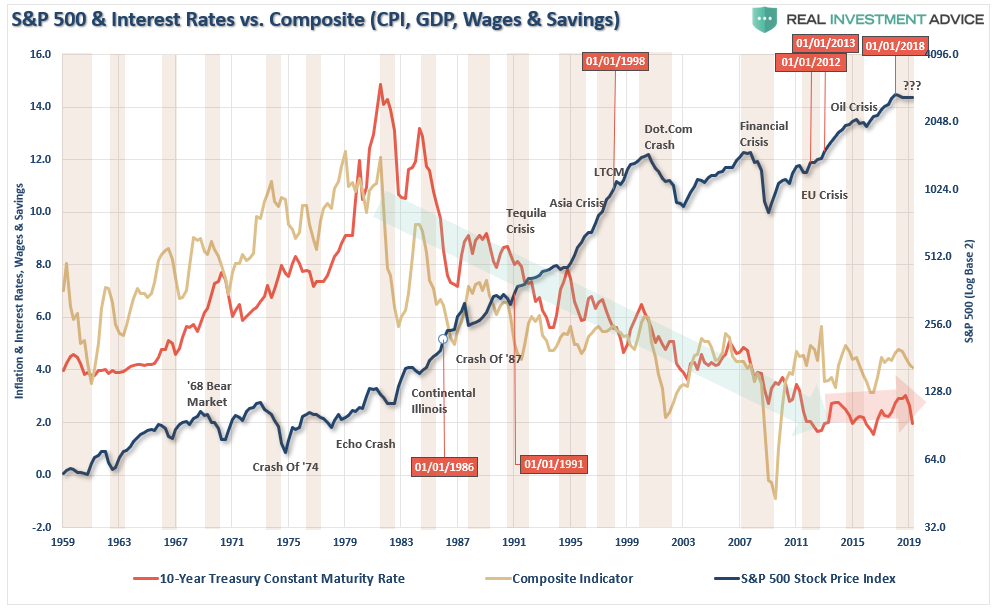

While, in the Fed’s defense, it may be clear the Fed’s monetary interventions have suppressed interest rates, I would argue their liquidity-driven inducements have done much to support durable economic growth. Interest rates have not been falling just since the monetary interventions began – it began four decades ago as the economy began a shift to consumer credit leveraged service society. The chart below shows the correlation between the decline of GDP, Interest Rates, Savings, and Inflation.

In reality, the ongoing decline in economic activity has been the result of declining productivity, stagnant wage growth, demographic trends, and massive surges in consumer, corporate and, government debt.

For these reasons, it is difficult to attribute much of the decline in interest rates and inflation to monetary policies when the long term trend was clearly intact long before these programs began.

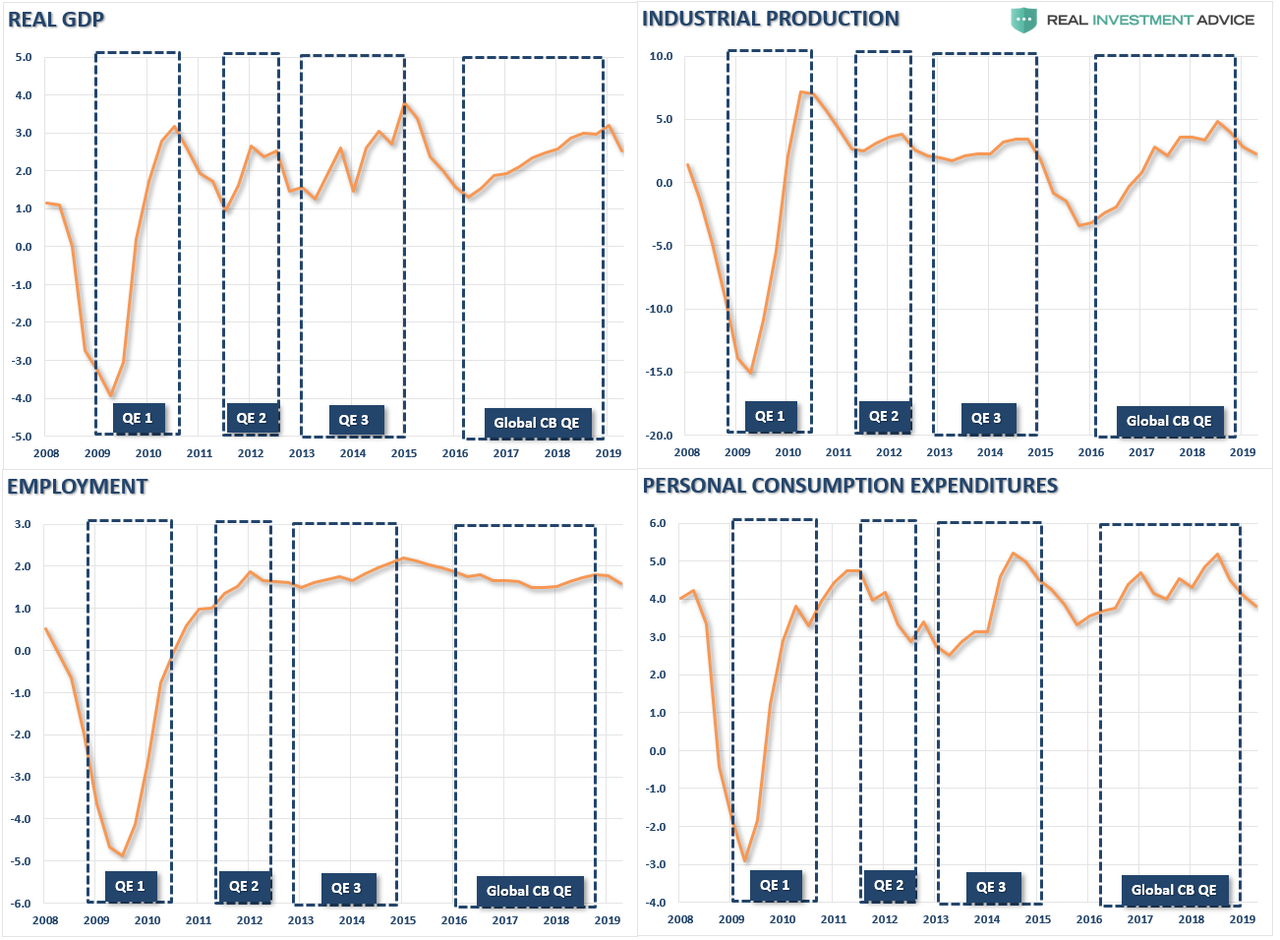

There is also no real evidence excess liquidity and artificially low interest rates have spurred economic activity judging by some of the most common measures – Real GDP, Industrial Production, Employment, and Consumption.

While an argument can be made that the early initial rounds of QE contributed to the bounce in economic activity it is important to also remember several other supports during the latest economic cycle.

- Economic growth ALWAYS surges after recessionary weakness. This is due to the pent up demand that was built up during the recession and is unleashed back into the economy when confidence improves.

- There were multiple bailouts in 2009 from “cash for houses”, “cash for clunkers”, to direct bailouts of the banking system and the economy, etc., which greatly supported the post-recessionary boost.

- Several natural disasters from the “Japanese Trifecta” which shut down manufacturing temporarily, to massive hurricanes and wildfires, provided a series of one-time boosts to economic growth just as weakness was appearing.

- A massive surge in government spending which directly feeds the economy

The Fed’s interventions from 2010 forward, as the Fed became “the only game in town,” seems to have had little effect other than a massive inflation in asset prices. The evidence suggests the Federal Reserve has been experiencing a diminishing rate of return from their monetary policies.

Lack Of Velocity

Once again, we find Judy Shelton completely clueless as to how monetary policy actually translates into the economy. She recently stated:

“When you have an economy primed to grow because of reduced taxes, less regulation, dynamic energy, and trade reforms, you want to ensure maximum access to capital. The Fed’s practice of paying banks to keep money parked at the Fed in deposit accounts instead of going into the economy is unhealthy and distorting; the rate should come down quickly as the practice is phased out.”

Poor Judy.

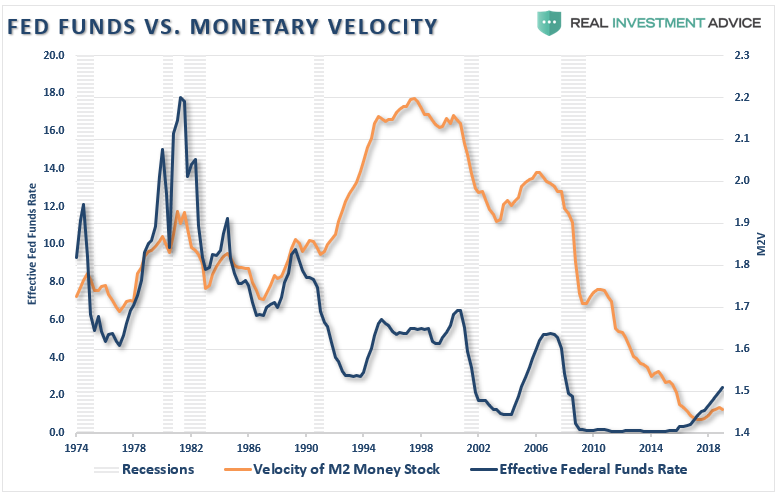

There is absolutely no evidence that the Fed’s “zero interest rate policy” spurred a dramatic increased in lending over the last decade. Monetary velocity has been clear on this point.

The definition of a “liquidity trap” states that people begin hoarding cash in expectation of deflation, lack of aggregate demand or war. As the “tech bubble” eroded confidence in the financial system, followed by a bust in the credit/housing market, and wages have failed to keep up with the pace of living standards, monetary velocity has collapsed to the lowest levels on record.

The issue of monetary velocity is the key to the definition of a “liquidity trap.” As stated above:

“The signature characteristic of a liquidity trap are short-term interest rates that are near zero and fluctuations in the monetary base that fail to translate into fluctuations in general price levels.”

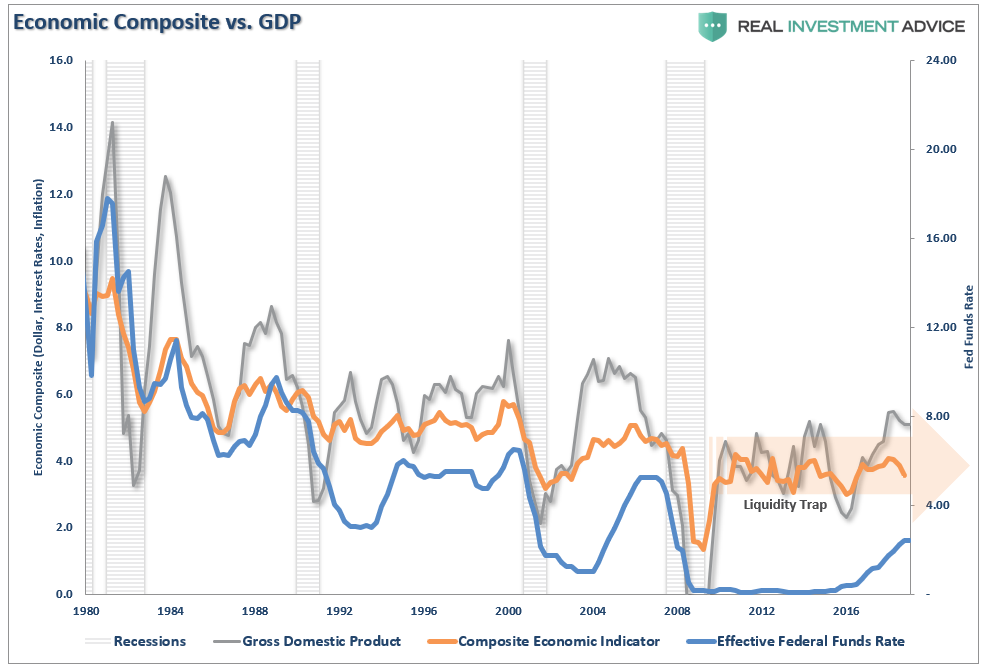

The chart below shows that, in fact, the Fed has actually been trapped for a very long time. The “economic composite” indicator is comprised of 10-year rates, inflation (CPI), wages, and the dollar index.While the BEA measure of GDP ticked up (due to consistent adjustments to calculation) the economic composite has not. More importantly, downturns in the composite lead the BEA measure.

The problem for the Fed has been that for the last three decades every time they have tightened monetary policy it has led to an economic slowdown or worse. More importantly, each rate hike cycle has continued to start at a lower rate level than the previous low, and has stopped at a level lower than the previous low as economic weakness set in.

While, in the short term, it appeared such accommodative policies aided in economic stabilization, it was actually lower interest rates increasing the use of leverage. However, the dark side of the increase in leverage was the erosion of economic growth, and increased deflationary pressures, as dollars were diverted from productive investment into debt service.

No Escape From The Trap

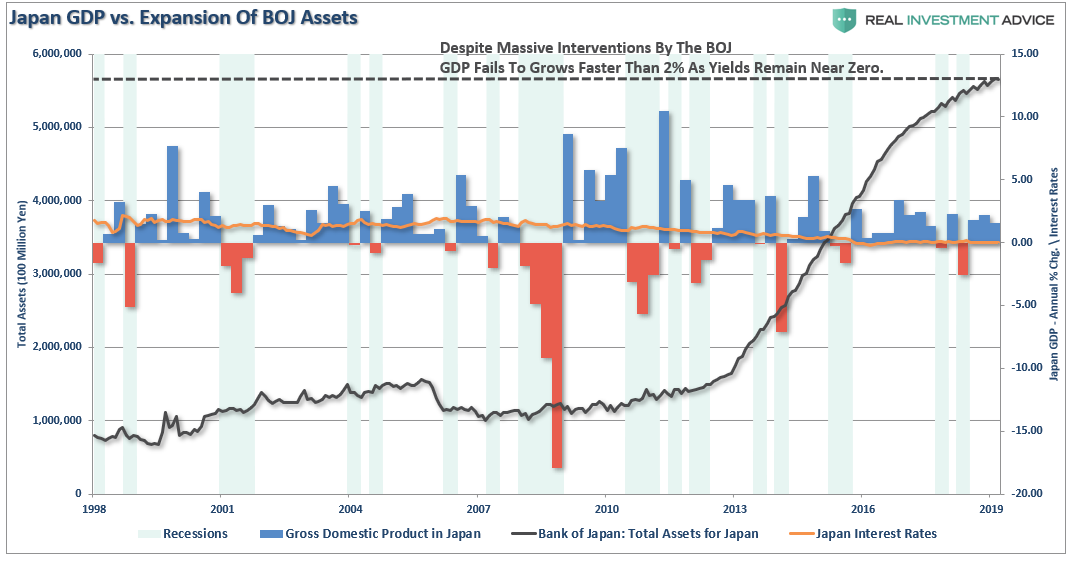

The Federal Reserve is now caught in the same “liquidity trap” that has been the history of Japan for the last three decades. With an aging demographic, which will continue to strain the financial system, increasing levels of indebtedness, and unproductive fiscal policy to combat the issues restraining economic growth, it is unlikely continued monetary interventions will do anything other than simply continuing the boom/bust cycles in financial assets.

The chart below shows the 10-year Japanese Government Bond yield as compared to their quarterly economic growth rates and the BOJ’s balance sheet. Low interest rates, and massive QE programs, have failed to spur sustainable economic activity over the last 20 years. Currently, 2, 5, and 10 year Japanese Government Bonds all have negative real yields.

The reason you know the Fed is caught in a “liquidity trap” is because they are being forced to lower rates due to economic weakness.

It is the only “trick” they know.

Unfortunately, such action will likely have little, or no effect, this time due to the current stage of the economic cycle.

While Judy Shelton may certainly have the President’s ear, her recent statements clearly show inconsistencies and a lack of understanding about how the economy and monetary policies function in the real world.

Of course, as we learned from Jerome Powell, what officials say before they are appointed, and do afterward, tend to be two very different things particularly when they have become “political animals.”