Everyone seems worried about it. Bridgewater Associates co-Chief Investment Officer Greg Jensen says spiraling prices that choke off growth are a “real risk” that many portfolios are massively overexposed to. A “fairly strong consensus” of market professionals believe that some kind of stagflation is more likely than not, according to a Deutsche Bank AG survey. And while Goldman Sachs Group Inc. urged investors to buy the dip, strategists said “stagflation” was the most common topic in client conversations.

Wherever you fall on the debate, alarm bells are ringing as energy prices head toward multiyear highs and persistent shortages crimp supply chains worldwide. That’s fueling price pressures and pushing up bond yields just as economic growth is cooling and central banks such as the Federal Reserve weigh scaling down pandemic-era stimulus. And after a second straight month of disappointing U.S. jobs gains, the stakes are rising heading into this week’s inflation report.

“The reality that inflation is more persistent and sustainable than the ‘transitory’ camp thought, and that inflation and its causes are in turn slowing economy growth,” said Peter Boockvar, chief investment officer for Bleakley Advisory Group.

Energy Epicenter

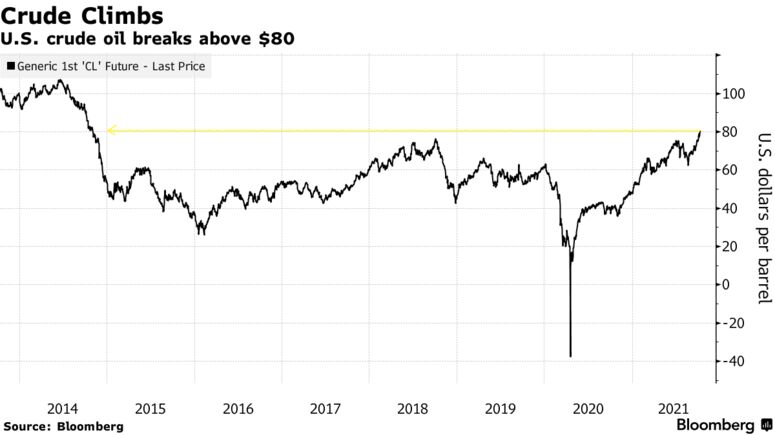

Much of the stress is emanating from the energy market, where West Texas Intermediate crude oil broke above $82 per barrel for the first time since 2014 on Monday amid a power crisis from Europe to Asia. Prices of coal and natural gas have also jumped, with demand ahead of winter whittling worldwide stockpiles.

The commodity surge has thrust stagflation fears front-and-center in markets, given that higher energy prices have the potential to pinch consumers, according to Principal Global Investors. Gains in consumer spending are already expected to slow, leading Goldman economists to slash U.S. growth estimates over the weekend.

“The idea was already starting to take shape. The increase in commodity prices has just formalized those fears,” said Seema Shah, Principal’s chief global strategist. “While there have been complaints around higher food prices, higher lumber prices, higher clothes prices, it’s the increase in household bills that has really put fear into peoples’ minds, because it is so visible and rising gas prices are difficult to substitute away from for an average household.”

Murky Bond Picture

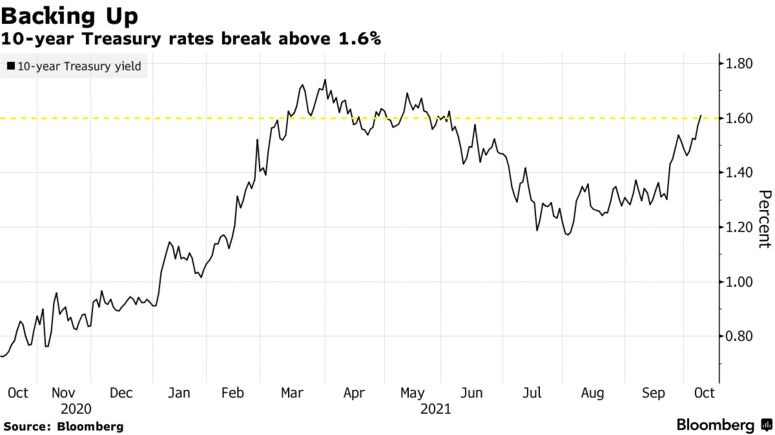

Sky-high commodity prices have filtered through to the Treasury market, where yields on benchmark 10-year notes broke above 1.6% for the first time since June last week. Driving the gain is an increase in breakeven inflation rates, while so-called real yields — often viewed as a proxy of growth expectations — have retreated so far this month.

“If we look at the composition within the TIPs market, we see an increase in breakevens to the detriment of real yields,” BMO strategist Ian Lyngen said on the firm’s “Macro Horizons” podcast. “We read this as the market’s focus on longer-term inflation has taken some of the optimism out of the growth profile going forward.”

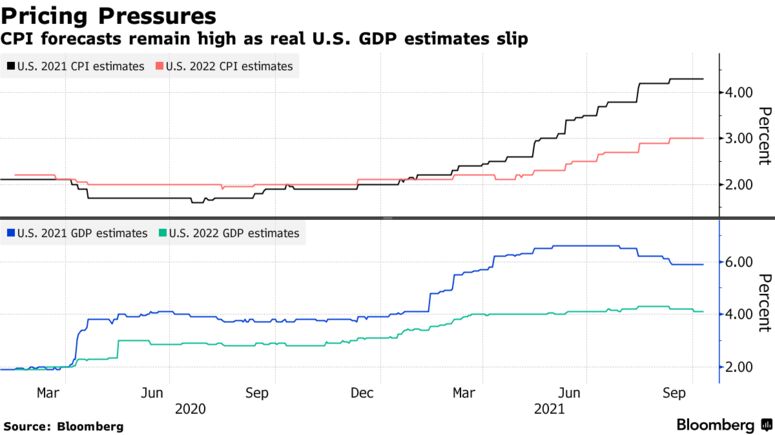

Morgan Stanley strategist Andrew Sheets disagrees. Breakeven rates are still below their May peaks, while the cross-asset landscape is distinct from the stagflationary setup of the 1970s, he argued. Data compiled by Bloomberg shows gross domestic product is forecast by economists to rise 5.9% this year, 4.1% next year and 2.4% in 2023.

“Asset pricing also couldn’t be more different. Over the last century, the 1970s represented an all-time high for nominal interest rates and an all-time low for equity valuations,” Sheets wrote in a note Sunday. “Today we’re near a low in yields and a high in those valuations.”

Stocks Still Serene

Equity investors so far seem unperturbed. That’s the view of Matt Maley, chief market strategist for Miller Tabak + Co., given that the S&P 500 is just 3.9% lower from its all-time high. However, the mood music could change as the third-quarter reporting season kicks off and corporate executives sound off on supply chain issues and rising input costs, he said.

“The key should be this earnings season,” Maley said. “If a lot of companies start talking about margin pressures, the stock market will start pricing in stagflation rather quickly.”

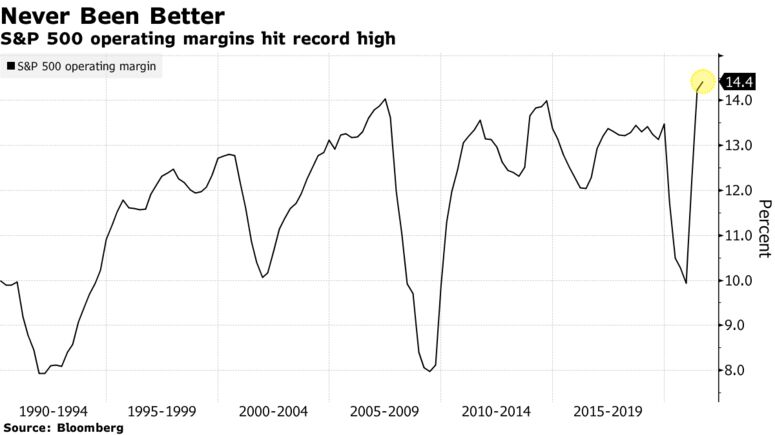

So far, balance sheets have been resilient. Operating margins for the S&P 500 clocked in at 14.4% last quarter, a record high, with companies in many cases actually benefiting from the inflation uptick.

But should stagflation fears start to meaningfully rattle equity markets, shares of companies with higher pricing power — the ability to pass on costs — should profit, according to Goldman, after several weeks of underperformance.

“Stocks with strong pricing power have recently lagged but appear attractive if stagflationary concerns continue to build,” strategists led by David J. Kostin wrote. “If inflation remains high alongside a weakening economic growth outlook, firms with strong pricing power should be best positioned to maintain profit margins despite slowing revenue growth and rising input costs.”

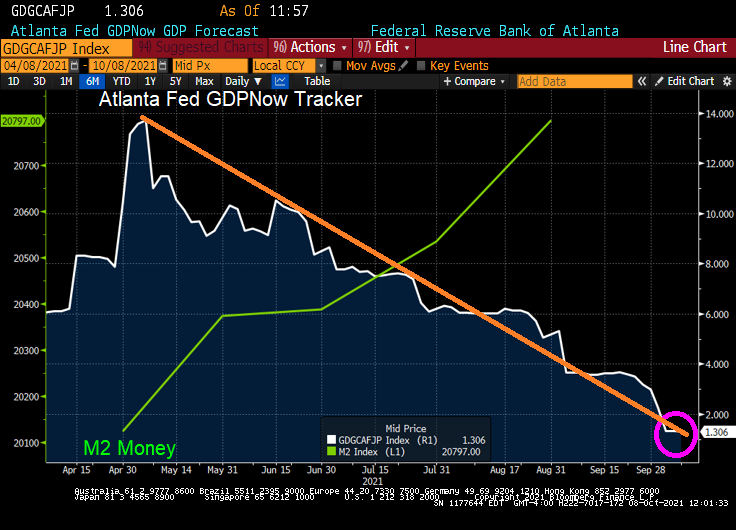

Not to mention real-time GDP of 1.3%. And falling!

Of course, there will be cries in Washington DC to spend trillions … and trillions … and trillions.