Wolf Richter wolfstreet.com, http://www.amazon.com/author/wolfrichter

Only feeble signs of manufacturing returning to the US (you’ve got to build the plants first).

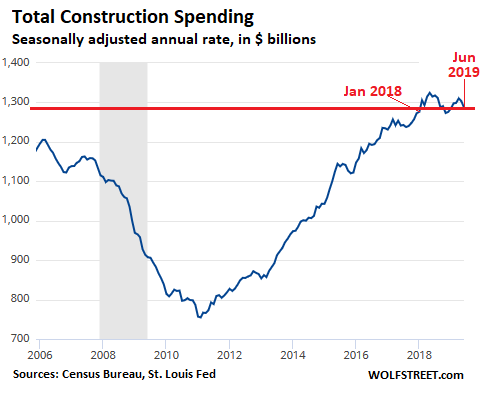

Construction spending, an important part of the US economy, has essentially gone nowhere over the past 18 months – the longest period of drought since the great recession. Total construction spending – residential and nonresidential, private and public – in June fell 2.1% from June last year to a seasonally adjusted annual rate of $1.29 trillion, according to the Commerce Department today.

Construction spending has now fallen on a year-over-year basis in four of the last five months, and is back where it had first been in January 2018:

All figures are quoted as “annual rate.” Annual rate means that at the June pace, construction spending for the whole year would total $1.29 trillion.

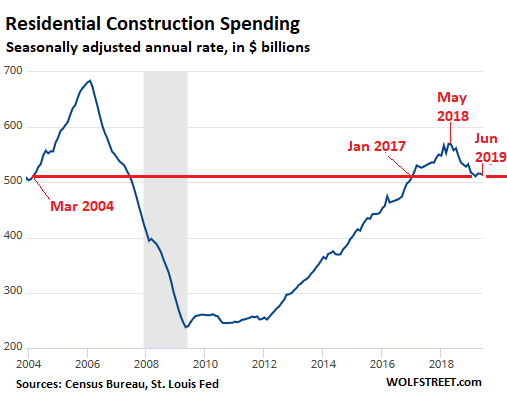

Residential construction spending – 99% is “private” rather than “public” spending – dropped 8% from June 2018, the ninth month in a row of year-over-year declines, to a seasonally adjusted annual rate of $513 billion, back to January and February 2017 levels, and down 10% from the recent peak in April 2018. Note, that residential construction spending never fully recovered from the collapse during the Housing Bust:

The decline in residential construction spending has been the dominant culprit for weak overall construction spending since mid-2018. But residential construction has stabilized near the $513 billion level during the past five months, and has stopped dropping. Now nonresidential construction spending is getting weak.

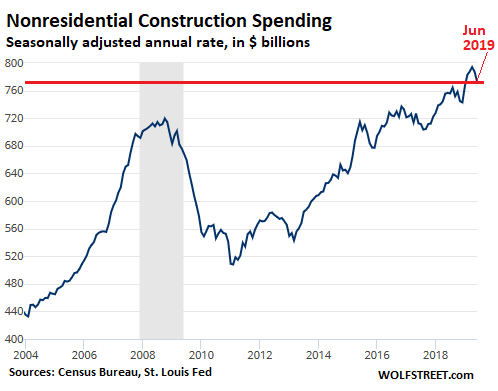

Nonresidential construction spending – which is about 50% larger than residential construction spending and is therefore a lot more important for the economy – had been growing at a decent clip through April, when it peaked at a seasonally adjusted annual rate of $794 billion, a historic record. But over the past two months, spending has dropped on a month-to-month basis, to a rate of $773 billion in June. This reduced the year-over-year gain to just 2.3%:

Unlike residential construction, nonresidential construction – which also collapsed during the Great Recession – has blown past the 2008 peak. But it took 8 years!

As the above chart shows, so far, the month-to-month declines still look fairly benign compared to episodes of declines in 2013, 2015, 2017, and even the four-month dip in 2018. So, it’s not yet time to panic. But the thing is, residential construction is weak, and if nonresidential construction continues to fall, overall construction spending is going to sag in a much more pronounced way.

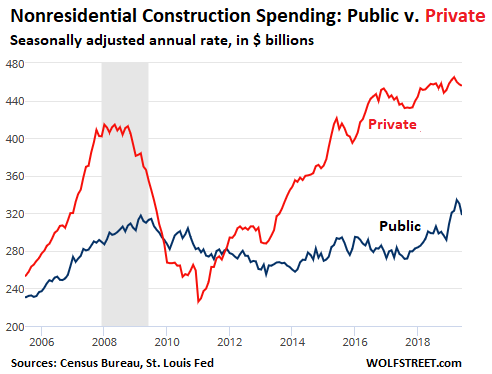

Private spending on nonresidential construction in June ticked down 0.4% year over year to a rate of $456 billion.

Public spending on nonresidential construction – by federal, state, and local governments for bridges, sewer projects, administrative buildings, etc. – declined on a month to month bases for the second month in a row, to a rate of $318 billion, down from the record spike in April. So year-over-year, given the double-digit growth earlier this year – it was still up 6.4%.

These are the largest segments of private nonresidential construction spending. The top two had sharp year-over-year declines in June; the remaining four booked sharp increases:

- Power, highly volatile but roughly flat since 2012: -4.8% yoy, to $92.4 billion.

- Commercial: -12.0% yoy, to $78.7 billion.

- Manufacturing (more in a moment): +10% yoy, to $71 billion.

- Office, at all-time record levels: +8.9% yoy, to $68.2 billion.

- Lodging: +8.1% yoy, to $33 billion.

- Healthcare: +5.9% yoy, to $34 billion.

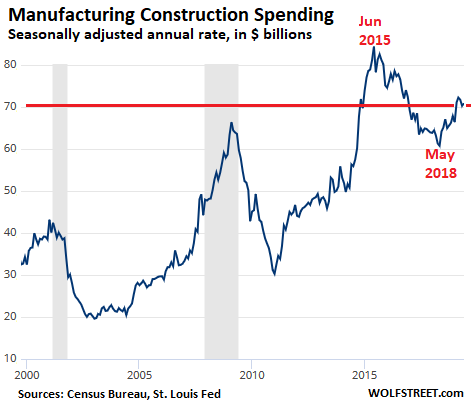

Since “bringing manufacturing back to the US” is currently such a politically charged topic, a special word about construction spending on manufacturing facilities, because you’ve got to build the plants first: It’s up 10% year-over-year, but…. Construction spending peaked in June 2015 at a historic record, and has since fallen 15% despite the increases in recent months. In terms of hopes that there would be a boom in US manufacturing – which would be coming along with a boom in spending on manufacturing facilities – the jury is still out.

Growth in manufacturing production – what is actually being produced at these plants – is languid at the moment, to put a positive spin on it. And the uptick in construction spending for manufacturing facilities since May 2018 is not in the same ballpark as the surge in early 2015, but it’s mildly encouraging:

Consumers and companies keep plugging, the world has not come to an end. Read... World Trade in Face of Tariffmageddon, Trade Wars & Manufacturing Slowdown