Wolf Richter wolfstreet.com, http://www.amazon.com/author/wolfrichter

The four account for 58% of global manufacturing value added. And the big exporters are getting hit.

The global slowdown in manufacturing progressed another notch in February. Among the top four manufacturing giants in the world, the US is the cleanest dirty shirt. Together, they produced 58% of the world’s “value added in manufacturing” in 2016:

- China: $3.08 trillion (26% of global total)

- US: $2.18 trillion (18% of global total)

- Japan: $979 billion (8% of global total

- Germany: $718 billion (6% of global total)

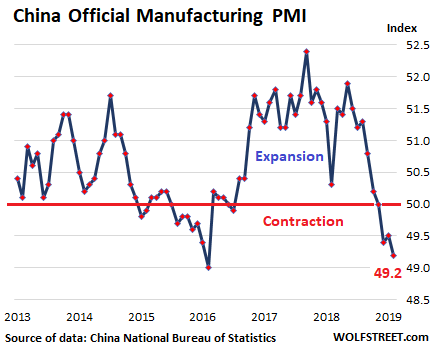

China’s small and mid-size manufacturers sink.

In February, manufacturing output declined for the third month in a row, and at the steepest rate since March 2016, according to the official Purchasing Managers Index (PMI), released by China’s National Bureau of Statistics. For these PMI measures, a value below 50 means “contraction,” and a value above 50 means “expansion”:

Small-sized manufacturers in China got hit the worst, with their PMI falling to 45.3, while the index for mid-sized manufacturers dropped to 46.9. Large manufacturers showed growth, at 51.5. And all combined, with the sub-index for employment, at 47.5, manufacturers were shedding jobs.

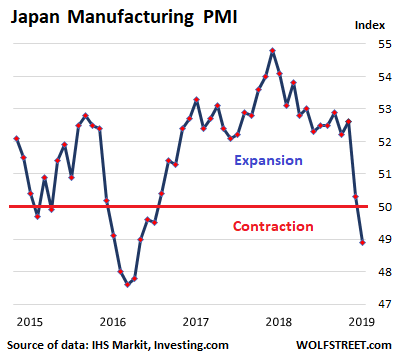

Japan dragged down by domestic demand & exports.

The Nikkei Japan Manufacturing PMI fell to a 32-month low of 48.9 in February. New orders declined at a quickened pace as new export orders continued to fall “amid lower sales to China.”

“Deteriorating demand conditions were signaled in the February PMI survey,” according to IHS Markit, which compiles the survey. New orders for Japanese manufacturers “dropped at the fastest rate in over two-and-a-half years.” And the decline in orders was “broad-based across both domestic and foreign markets, with falling new export sales also recorded.”

Businesses cut their output expectations for a ninth month in a row. The manufacturing executives on the panel cited “global trade frictions, downbeat demand forecasts, and the impending consumption tax hike” in Japan.

PMI measures are based on surveys of industry executives whose names and companies are not disclosed. These “panelists” are asked to rate various aspects of their companies – new orders, new export orders, employment, backlog, inventories, supply chain delays, input costs, etc. — by whether each of these aspects is increasing or decreasing. Their responses form the sub-indices, which are then combined into the overall headline index (the basis for these charts).

These PMIs are a quantified boots-on-the-ground view by panelists who see how their company are being impacted by economic developments. They can get outright gloomy in the run-up to a crisis, such as the European Debt crisis from 2010-2012, and have proven to be fairly accurate predictors of manufacturing data coming down the pike.

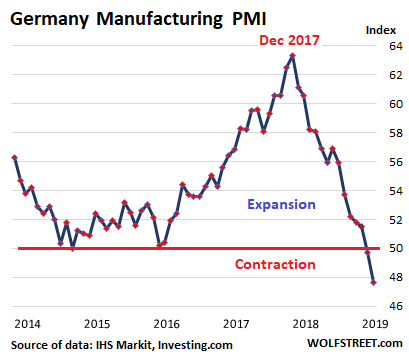

Germany dragged down by exports and cars:

The IHS Markit/BME Germany Manufacturing PMI in February dropped below 50 for the second month in a row, and at 47.6 to the lowest level – the fastest contraction – since December 2012, “showing a deepening downturn in new orders and the first drop in output in almost six years”:

All sub-indices except employment were in contraction mode. Hardest hit were the intermediate and capital goods sectors. Only manufacturers of consumer goods recorded an increase in output. IHS Market added that the downturn in new orders is “gathering pace, led by a sharp and accelerated decline in export sales. The level of new business from abroad fell the most since October 2012.”

The panelists blamed dropping car sales – a huge industry in Germany – weaker demand from Asia, and particularly from China, “Brexit anxiety among clients,” and increasing competition.

Due to the cut in output, manufacturers reduced their purchases for the fifth month in a row, “with the rate of decline accelerating to the quickest in over six years.”

But it’s not just in Germany…

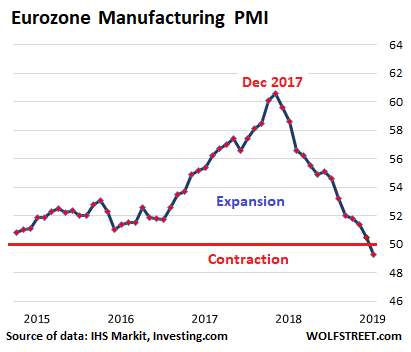

Eurozone dragged down by Germany, Italy & Spain:

The IHS Markit Eurozone Manufacturing PMI fell to 49.3. Germany led the decline. The index for Spain (49.9) entered contraction mode for the first time since November 2013. The index for Italy (47.7) was in contraction mode for the fifth month in a row, and at the lowest level since May 2013.

The chart below is on the same scale as the chart for Germany above; so you can see that the peak, and the decline from the peak, have been less pronounced than in Germany alone, with the manufacturing sectors in several Eurozone countries still in expansion mode – including in France, the Netherlands, Austria, Ireland, and Greece:

IHS Markit observed that new orders fell the most since April 2013; inventories of finished goods were rising for the fifth month in a row; manufacturers were reducing their backlogs for the sixth month in a row, “and to the greatest degree since April 2013.”

And there is a bifurcation, with a downturn in the in the intermediate and capital goods sectors, while the consumer goods sectors continued to expand, though at the weakest pace since July 2016. The report added:

Euro area manufacturing is in its deepest downturn for almost six years, with forward-looking indicators suggesting risks are tilted further to the downside as we move into spring.

Most worrying is the downward trend in new orders. Orders are falling at a faster rate than output to a degree not seen for seven years, meaning production is likely to be pared back further in coming months unless demand revives. The new orders to inventory ratio has also fallen to its lowest since 2012, with many companies reporting excess warehouse stocks.

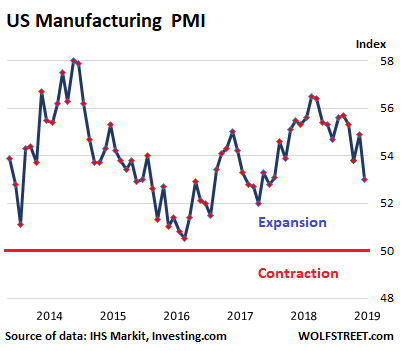

The US, the cleanest dirty shirt, so to speak:

Operating conditions in the US manufacturing sector in February showed “softer, but still solid improvement … amid slower expansions in output and new orders,” according to the IHS Markit US Manufacturing PMI. Backlogs were still increasing, as was employment. The index, at 53.0, shows the slowest expansion in 18 months, “with firms reporting a marked easing in production growth in February, linked to a similar slowdown in order book growth:

The survey “suggests that factory production and orders growth rates are close to stalling mid-way through the first quarter,” the report said. “Export markets remained the principal drag on order books.”

The manufacturing PMI from the Institute for Supply Management comes to similar conclusions – decent but slowing growth in the US, and was a notch or so more upbeat: “Comments from the panel reflect continued expanding business strength, supported by notable demand and output, although both were softer than the prior month.”

These PMIs are a scale for global demand and regional within the goods-based economy, giving an advance glimpse of official manufacturing data one or two months later. And for now, the US manufacturing sector is hanging on, even as manufacturers in China, Japan, and Germany are losing grip.