by DaGhostOfMarx

This should be obvious to anyone who hasn’t been living under a rock, but given the mass influx of Robinhood and other retail into $USO in recent days, it apparently isn’t.

What $USO Is and Isn’t

United States Oil is not a bet on the price of oil, just like VIX ETFs (UVXY, TVIX) are not bets on the spot price of VIX. It’s a bet on the yield of rolling 1-month oil futures into the next month. Up until today, the fund held the vast majority of its assets in front month futures – it held around 25% of all oil futures contracts for May prior to the spectacular blow-up in that market. It now holds over 25% of June’s contracts.

Along with other speculators, $USO cannot actually take physical delivery of this oil. It is thus forced to sell and roll those contracts every month to get them off its books. This makes it a shitty buy-and-hold vehicle at any time, but these are special times.

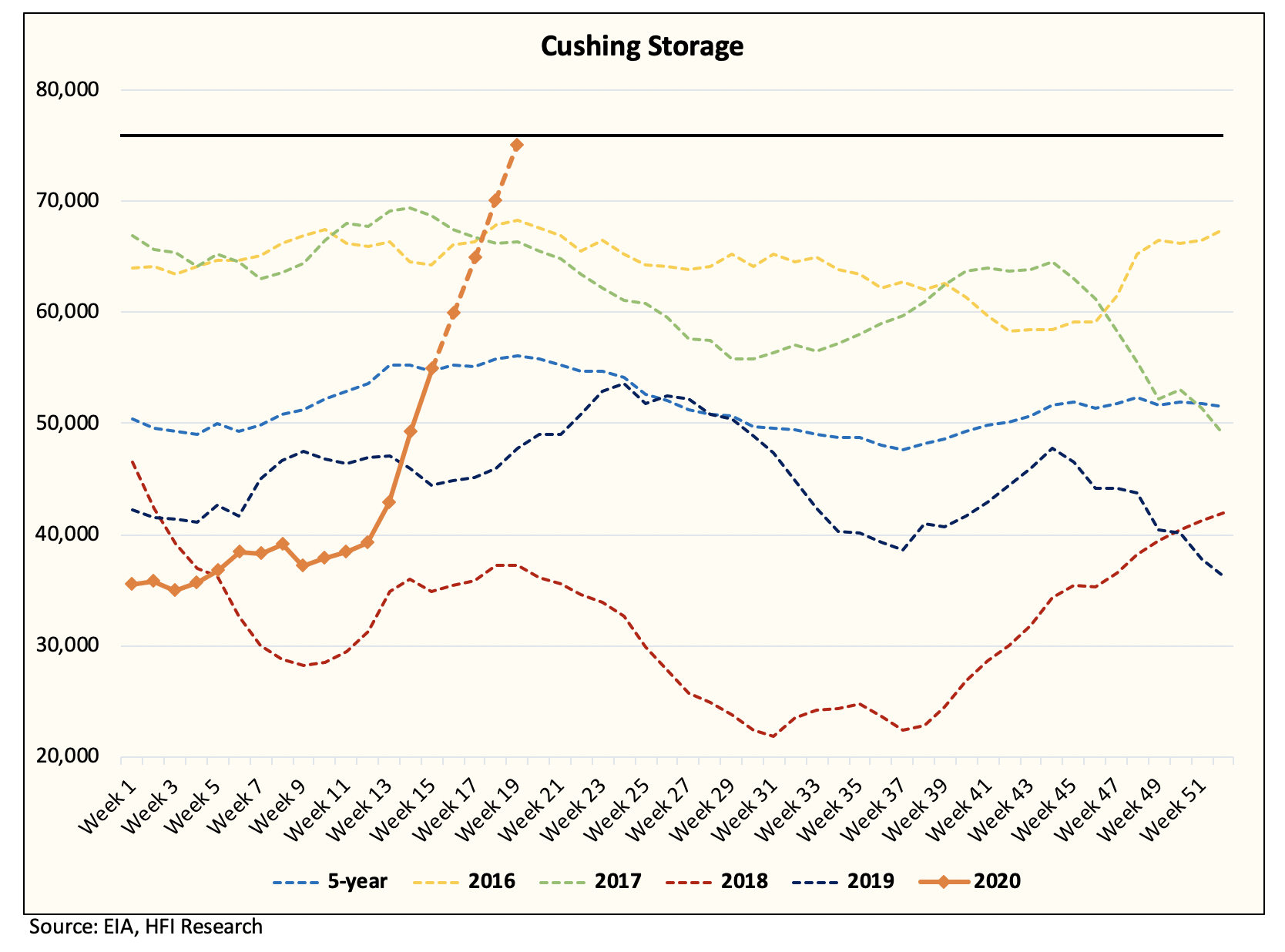

The Fundamentals

Everyone knows that the oil market is fucked. No travel and (next to) no economy means (next to) no oil consumption. Along with the Saudi-Russian price war, this has caused a massive glut of production that needs to be stored somewhere. These oil futures are based on delivery to a specific place with limited storage capacity: Cushing, Oklahoma. The oil storage problem is not getting better and certainly isn’t going to evaporate in a few weeks when $USO next needs to roll contracts.

{kind=link}

When speculators and ETFs like $USO sell contracts, they need someone who can actually receive and store the crude oil to buy them. May was a spectacular blow-up for a variety of reasons, including non-fundamentals-related front-running of contract rebalancing (this is a problem with many products). But one crucial reason was the need to dump a full quarter of all futures contracts in a few days onto limited storage/reception capacity and the fact that no one is fucking buying oil. Hence the insane selling even in negative territory – if you can’t store, you can’t buy contracts at/near settlement.

$USO “Restructuring” and the Contango Shitshow

$USO’s value has declined precipitously along with the collapse of oil/futures markets. Its underlying assets (futures contracts and some Treasury hedges) have dropped in value from $13 a share in January to $2 a share now. $USO has decided to “fix” its exposure and contract rolling problem by spreading itself out into July and August contracts. It now “only” holds 55% of its assets in June contracts. It can also no longer create new shares to draw in capital from dumb retail bagholders (you) and is thus trading as a closed-end fund.

Oil futures are still in deep fucking contango – which means later month futures are trading way higher than closer months. Makes sense, right? What doesn’t make sense is investing in a product that has to sell those dirt cheap front month contracts to buy more expensive contracts every fucking month. June contracts will need to be rolled in early May. Who is going to buy and store all that oil? No one! $USO still needs to dump $1.6 billion in June futures (read: your money) to get out of this mess, and that’s at a price of $11.57 per contract. If those contracts go to zero again, that’s the majority of the fund’s remaining assets gone. Zilch. And if they go negative? The ETF will be on the hook for those losses.

$USO is currently trading at ~$2.74 after hours while the value of underlying assets per share (NAV) is $2.06. That’s a 33% premium based on retail idiocy! The fund is going to liquidate just like $OIL, soon, and its value could be completely obliterated in the process. No one holds the bag like retail and pensions. Get the fuck out while you still can.

Disclaimer: This information is only for educational purposes. Do not make any investment decisions based on the information in this article. Do you own due diligence.