by howmuch

It’s no secret that millions of Americans are struggling with debt, but the numbers might still surprise you. While the economy doesn’t seem to be slowing down quite yet, U.S. debt is reaching worrying heights.

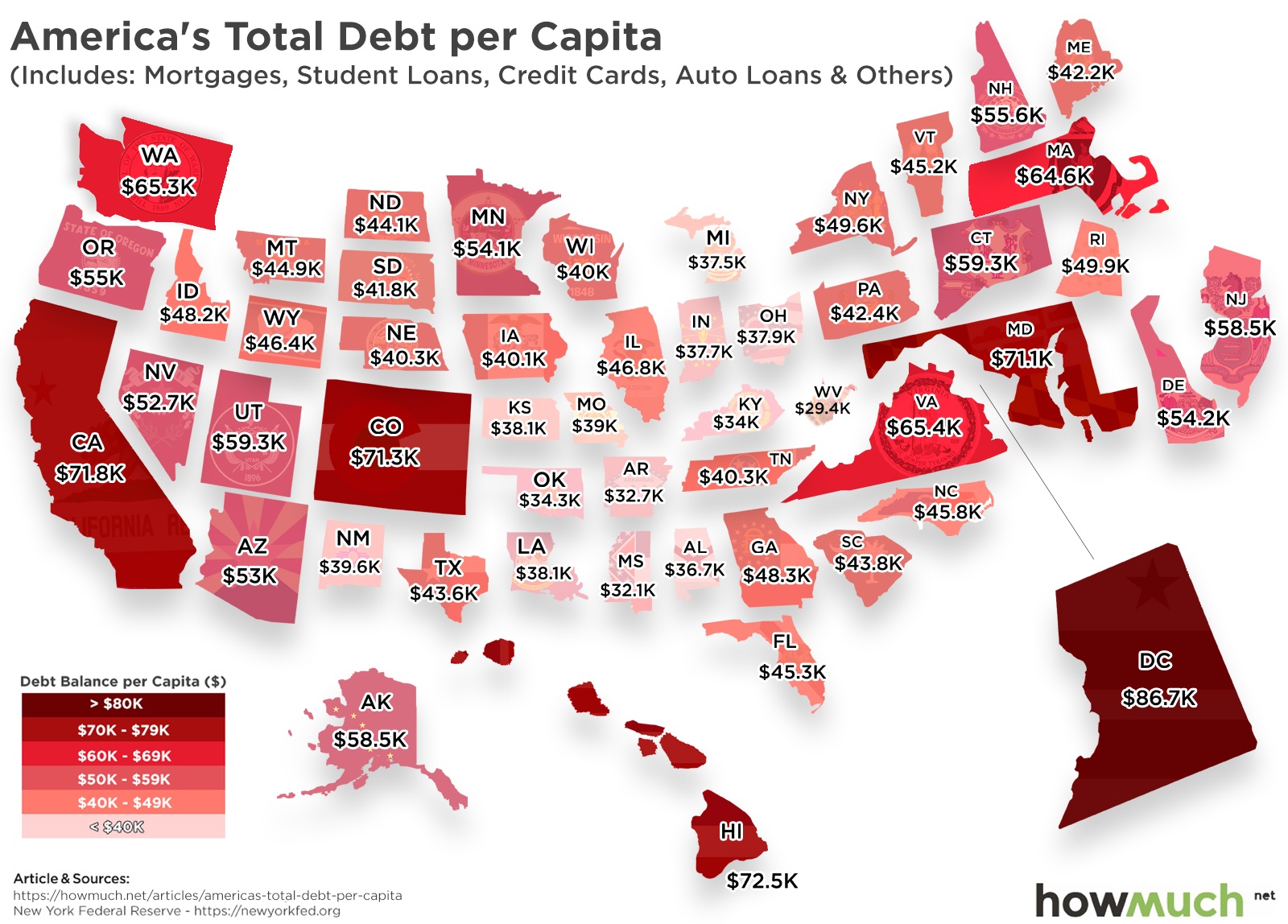

To see how extreme this debt crisis is, let’s take a look at each U.S. state’s debt per capita.

- The District of Columbia has the highest total debt per capita at $86,730

- Mortgages are the primary source of each state’s total debt per capita

- The total debt per capita across the United States is $50,090

- West Virginia has the lowest total debt per capita at $29,430

- Federal debt is rising at alarming rates and is expected to reach 92% of the GDP by 2029

U.S. consumer debt is continuing to increase with the main causes being auto loans, credit card debt, student loans, and mortgages. Using data from Credit Karma and the New York Federal Reserve, we can see how consumer debt is affecting consumers across the nation. But consumer debt isn’t the only concern. Federal debt is increasing at unprecedented rates. To make matters worse, the federal government faces debt default by early September due to lower than expected tax revenues. Though the U.S. economy doesn’t seem to be in immediate danger of slowing down, the current debt crisis presents some cause for concern.

States With the Highest Total Debt per Capita

1. District of Columbia: $86,730

2. Hawaii: $72,590

3. California: $71,860

4. Colorado: $71,340

5. Maryland: $71,120

States With the Lowest Total Debt per Capita

1. West Virginia: $29,430

2. Mississippi: $32,100

3. Arkansas: $32,790

4. Kentucky: $34,010

5. Oklahoma: $34,370

The visualization used above shows us each state’s debt per capita, but that doesn’t necessarily paint the entire picture. It’s also important to look at where this debt is coming from. In all states, mortgage loans make up the largest percentage of total debt per capita, but mortgages are often considered good debt as they are used to purchase assets which can appreciate over time.

Revolving debt, on the other hand, is more troubling. While credit card debt and auto loans make up a lower percentage of total debt, are typically considered bad debt. Meaning, states with lower total debt per capita but higher credit card, auto loan, and student loan debt balances aren’t necessarily in better shape. By examining each state’s total debt per capita as well as the sources of this debt, we can get a better idea of the current state of consumer debt in the United States.

Total debt per capita, as well as federal debt, are continuing to increase at rapid rates. However, that isn’t necessarily a bad thing. Debt is relative. If you owe $20 and earn $100,000, that’s nothing. However, if you owe $20 and only make $100, that’s a big deal.

Small amounts of debt can often stimulate economic growth. Additionally, debt you take out for an investment yields positive results. Student loan debt becomes an investment when it increases your earnings potential over the cost of the debt. Debt for business equipment that increases production works the same way. Debt turns bad when you use it to purchase things that quickly lose their value. Taking out debt for things like clothes shopping beyond basic needs is bad debt. Putting a gaming system on your credit card is bad debt.

While the U.S. economy is still going strong, it’s important to be aware of the severity of the current debt crisis so that we can work to improve the situation.

Are you one of the millions of Americans struggling with consumer debt? Are you worried about the rising federal debt? Let us know in the comments below. We love to hear feedback from our readers.

Data: Table 1.1