Wolf Richter wolfstreet.com, http://www.amazon.com/author/wolfrichter

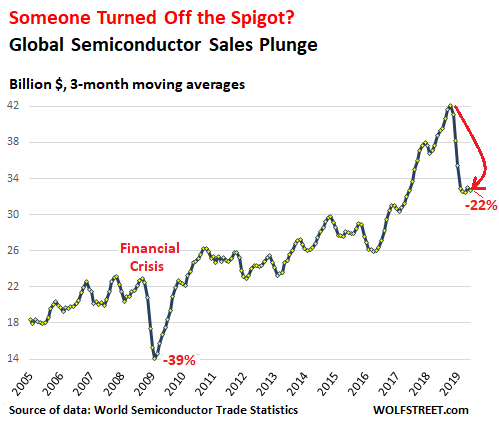

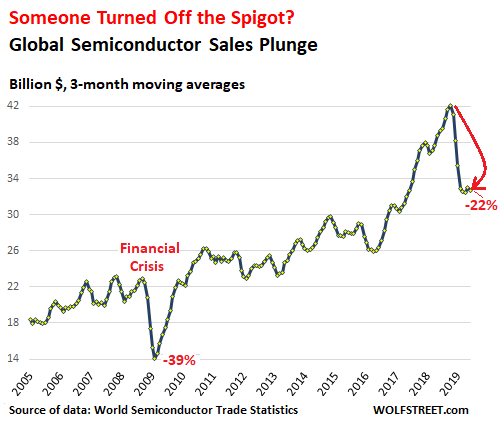

The deepest plunge since the Financial Crisis, but more persistent.

Global chip sales plunged 16.8% in June from June last year, to $32.7 billion, on a three-month moving average basis, and are down 22% from the peak in October 2018, according to the World Semiconductor Trade Statistics today. As deepest and most relentless plunge in semiconductor sales since the Financial Crisis continues, any hopes for a V-shaped recovery, such as during the Financial Crisis, have been shelved:

This was the fifth month in a row that the three-month moving average has been in the range of $32 billion to $33 billion, down about $10 billion from the peak in October last year, the steepest dollar-drop ever. During the Financial Crisis, sales plunged and then bounced back instantly, for a perfect V-shaped recovery. But this time around, sales have been stuck at low levels for five months already.

In percentage terms, the 22% drop from the peak pales compared to the 39% plunge during the Financial Crisis and the 45% plunge during the long dotcom bust. The dotcom-bust plunge was the worst, not only the deepest in percentage terms, but also by far the longest in duration.

For the first six months of 2019, semiconductor sales dropped 14.5% compared to the same period last year. And sales were down “across all major regional markets and semiconductor product categories,” the report by the Semiconductor Industry Association said.

Sales fell in all major geographic regions in June (three-month moving averages compared to the same period last year):

- Americas: -29.5%

- Europe: -10.9%

- Japan: -12.8%

- China: -13.9%

- Asia Pacific/All Other: -13.7

The culprits span the spectrum, from the decline in smartphone sales to the crypto-mining collapse. But now add a new one that is spreading across the globe:

Auto sales drop around the globe.

What was at first thought to be a localized drop in China and a little bitty dip in the US and some squiggles in Europe has now turned into a serious global downturn, and there are a lot of semiconductors in each new vehicle rolling off the assembly line. While chips for EV-related components such as battery management systems are still experiencing growth, chips for ICE-vehicle components are getting hit. This include the multitude of chips in emission systems, engine management systems, transmissions, fuel systems, lighting systems, infotainment systems, driver assist systems, etc.

In the second quarter, global sales of new vehicles fell 7% compared to the same period last year, after having already fallen 6.5% in the first quarter, according to Bloomberg Intelligence. I have covered the sales debacle in select hot spots:

- In China, the world’s largest market, new vehicle deliveries are down 12% so far this year;

- In the US, the world’s second largest market, deliveries are down for the third year in a row and are back to 1999 levels;

- In India, deliveries have plunged about 25% in May and June year-over-year, for a host of reasons, including a shadow-banking financial crisis;

- In the UK, auto sales dropped to a five-year low;

- In Canada, auto sales fell 5.5% in the first half this year, after having already fallen for the year 2018, on track for the second year in a row of declining sales.

Smartphone sales drop around the globe.

In terms of the number of devices shipped, global smartphone sales have declined in the first half, from mere stagnation in 2018, according to Gartner Inc., which expects unit sales for the whole year to continue on the same path and end the year down 2.5%, with the steepest declines in Japan (-6.5%), the EU (-5.3%), and North America (-4.4%).

“In mature markets, the high-end smartphone market is particularly oversupplied and commoditized, with higher average selling prices (ASPs) and no compelling new utility or experiences for users to upgrade to,” the report said.

PC/laptop shipments fell then ticked up.

In the second quarter, global PC and laptop shipments ticked up 1.5% compared to Q2 2018, after having fallen 4.6% in Q1, according to Gartner.

The Big Three vendors booked increases in shipments in Q2 – with Lenovo up 15.9%, HP up 2.6%, and Dell up 2.1% – and were able to increase their market share to a combined 64.1%, up from 60.7% a year earlier. The also-rans all booked declining shipments: Apple -0.2%, Acer -14.4%, ASUS -9.9%, and Others -6.7%.

Global IT spending on hardware falls.

Total IT spending, hardware and software, is expected to remain about “flat” at $3.7 trillion globally in 2019, “despite uncertainty fueled by recession rumors, Brexit, trade wars and tariffs,” according to Gartner. Software sales are expected show growth (Enterprise Software +9.0%, IT services + 3.8%, and Communications Services -1.0%).

But hardware sales – that’s where semiconductors end up – are expected to fall in dollar terms in 2019: Data Center Systems (“the cloud”), which used to be the hottest of the hot segments, -3.5% and Devices -4.3%.

“Although an economic downturn is not the likely scenario for either 2019 or 2020, the risk is currently high enough to warrant preparation and planning. Technology general managers and product managers should plan out product mix and operational models that will optimally position product portfolios in a downturn should one occur,” the report said.

The US-China trade-war debacle.

The rhetoric last year about potential tariffs and export controls triggered a stampede in 2018 on all sides to buy semiconductors to front-run actual tariffs and export controls. That is one of the reasons why semiconductor sales surged to that extent last year.

These export controls have now hit Chinese tech and telecom giant Huawei Technologies, whose telecom infrastructure equipment and smartphones contain US semiconductors. Huawei has seen this coming and has prepared for it by stockpiling semiconductors and other potentially affected components to keep its business supplied for up to six months or a year, allowing it time to realign its supply chain. Other Chinese companies have made similar preparations – all of which boosted chip sales and inventories last year, and created a hangover this year.

The Crypto-mining collapse.

The boom in the special rigs used to mine cryptocurrencies was huge and contributed to the surge in chip sales in 2017 but it collapsed in 2018, which hit certain chip makers in a concentrated manner, such as Nvidia.

Chips go into an endless variety of goods. Even a new toaster has a chip or two. The goods-based sectors globally have been ailing, and chip sales are a sign of that. But they’re also a sign of how the economy reacts to uncertainties, such as the threat of tariffs and export controls in 2018, and then the actual imposition of them.

US makers of heavy trucks – such as Peterbilt, Kenworth, and Mack – are still floating on top of what was a historic order backlog created in 2018. But orders have collapsed, and that backlog is dissipating fast. Read… Heavy-Truck Orders Collapse Stunning 81%. Lowest Since 2010