By Alex Kimani

- Don’t expect the oil price rout to trigger a wave of M&A activity any time soon.

- The last Big Oil M&A wave turned into a disaster for the acquiring companies.

- There’s a very real possibility that 2020 could be the slowest in the history of mergers in the sector

Under normal circumstances, energy downturns create a perfect opportunity for deep-pocketed oil and gas heavyweights to land prime assets on the cheap. A good case in point: the last oil bust of 2016 was followed by a sizable number of huge M&A deals in the sector including the $60B tie-up between Royal Dutch Shell (NYSE:RDS.A) and BG Group, Canadian Oil Sands and Suncor EnergyEnergy, as well as a handful that fell through including the proposed merger between Halliburton (NYSE:HAL) and Baker Hughes (NYSE:BKR). But these are hardly normal circumstances and don’t expect the oil price rout to trigger a wave of M&A activity any time soon.

That’s according to Cowen analysts via Barron’s who have said that the majority of Big Oil executives will likely be too gun-shy to pull the trigger on the numerous distressed assets that are becoming available as the downturn drags on.

M&A disaster

The Cowen team, led by Jason Gabelman, has pointed out how the last M&A wave turned into a disaster for the acquiring companies.

In April, Royal Dutch Shell cut its dividend to US$0.16 per ordinary share from US$0.47, for a 66% cut. That marked the first time the company cut the dividend since WWII, a testament of just how severe the oil massacre has been, which is what Shell blamed in its press release. However, another culprit could be to blame for the dramatic cut: the company’s 2016 acquisition of BG Group, which set it back $60B.

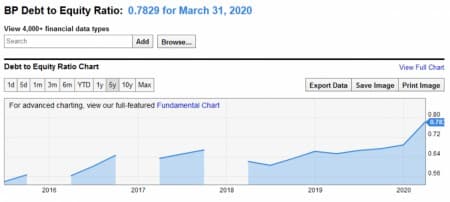

Occidental Petroleum’s (NYSE:OXY) $55B leveraged purchase of Anadarko has become the poster-child of oil and gas mergers gone bad. The deal has turned into a complete disaster, leaving the company in deep distress over its mountain of debt and water cooler wisecracks of how it could itself get acquired at a fraction of what it paid for Anadarko. Cowen also pointed to BP Plc.’s (NYSE:BP) extremely high debt, though it might have less to do with its 2018 merger with BHP Billiton for $10.5B and more to do with its Deepwater Horizon oil spill which has cost it a staggering $65B in clean-up costs and legal fees over the years.

BP’s debt-to-equity ratio of 0.78 is way higher than the oil and gas sector’s average of 0.47, and the highest among the oil supermajors. So far, BP has maintained its juicy dividend (fwd yield of 10.64%) but keeps piling on debt after recently taking on $12B in hybrid bonds, thus raising genuine questions about its sustainability.

Source: Y-Charts

Cowen though says that oil majors like Chevron (NYSE:CVX) and Total (NYSE:TOT) with relatively strong balance sheets could go for cheap assets such as GALP Energia (GALP.Portugal) or BP’s stake in a gas project in Oman.

Evidence coming from the oil and gas M&A space so far appears to support Cowen’s sentiments.

In April, a report by Enverus (formerly DrillingInfo) revealed that U.S. upstream M&A deals for the first quarter only amounted to $770 million, less than 1/10th the average deal amount recorded quarterly over the previous decade.

The largest dollar transaction was a deal by Alpine Energy Capital, which purchased Approach Resources’ Midland Basin assets for $193 million. That compares very poorly with the $55 billion Occidental-Anadarko merger or the $9 billion tie-up between Marathon Oil and Andeavor Logistics, both consummated last year.

Further, Enverus said that only ~$4.7B in upstream deals were available in the market by the end of the quarter, the majority of which were located in the Eagle Shale. There’s a very real possibility that 2020 could be the slowest in the history of mergers in the sector if the other three quarters track Q1 numbers closely.

Shale opportunities

Instead of mergers, oil and gas companies prefer to maintain the all-important dividend or cut capex in a bid to preserve liquidity. This is a trend we clearly witnessed during the last earnings season.

Not everybody shares Cowen’s bearish M&A outlook though. Goldman Sachs analyst Michele DellaVigna has told Barron’s that the highly fragmented U.S. shale industry could be a candidate for a spate of consolidations.

DellaVigna, though, has conceded that we are unlikely to see a repeat of the megamergers of the 1990s; however, he says there’s a financial case to be made for mergers especially in a sector like U.S. shale that has previously lacked cost discipline:

“The oil industry has delivered its best corporate returns in periods of consolidation, financial tightening and rising barriers to entry. We believe this environment (and shareholder pressure for de-carbonisation) could engender a similar phase of consolidation and capital discipline, as in the late ’90s.”

By Alex Kimani for Oilprice.com