Every price rally of 2019 has ended in tears. The latest will probably end similarly.

It is based on hope that ending the U.S. – China trade war might improve the economy and oil demand. It is also based on belief that yet another OPEC+ production cut will make a difference. In other words, it is based on sentiment.

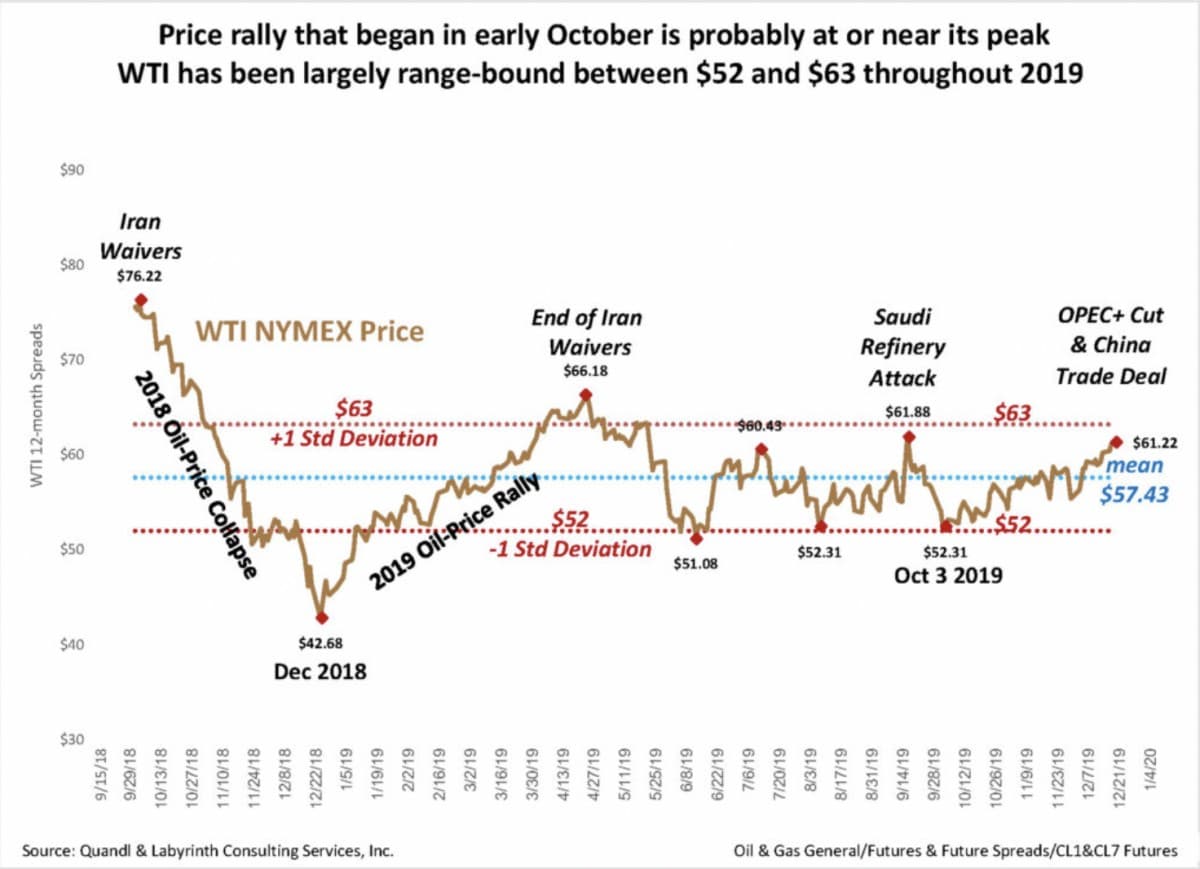

WTI prices began increasing in early October from a low of $52.31 and reached $61.22 on December 19 (Figure 1). $52 was one standard deviation less than the WTI mean for the last 15 months. Each price rally of 2019 began within a dollar of this low and ended in the low-to-mid $60 range, about one standard deviation more than the mean.

Figure 1. The oil price-rally that began in early October is probably at or near its peak. Source: Quandl and Labyrinth Consulting Services, Inc.

The current price rally gathered momentum after November 29. Since then, the oil-price volatility index OVX has fallen 32% (Figure 2). This change cannot be related to any specific cause other than optimism. Falling OVX generally correlates with higher oil prices in the short term.

Figure 2. The WTI oil-price volatility index OVX has fallen sharply (-32%) since November 29. Source: EIA, CBOE, Quandl and Labyrinth Consulting Services, Inc.

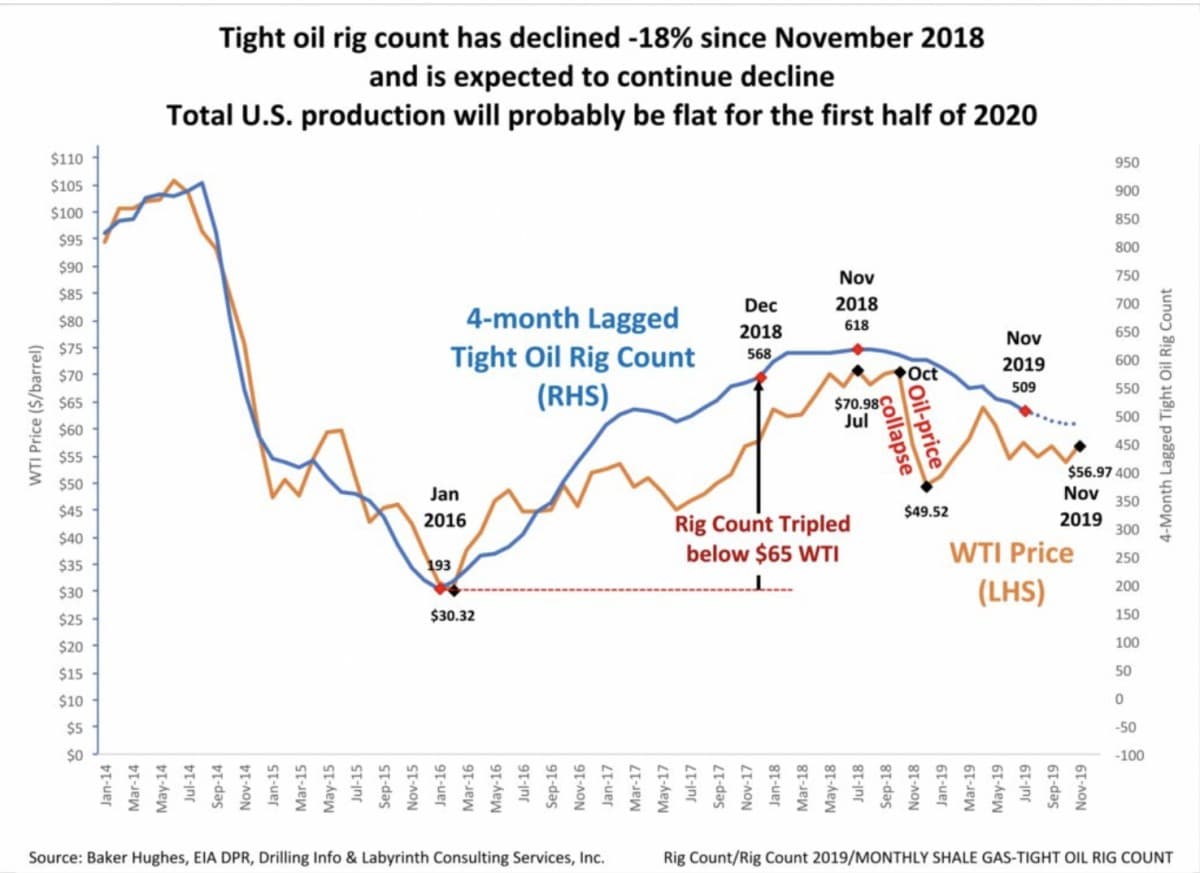

Some believe that potential peaking of U.S. shale production is a factor in the current price rally. The tight oil rig count has declined 18% since November 2018 and is expected to continue to decline (Figure 3). Accordingly, tight oil and total U.S. production will probably be flat for the first half of 2020. While this is certainly an important development, it is not new.

Figure 3. Tight oil rig count has decilned since November 2018 and is expected to continue to decline. Total U.S. production will probably be flat for the first half of 2020. Source: Baker Hughes, EIA DPR, Drilling Info and Labyrinth Consulting Services, Inc.

Comparative inventory (C.I.) provides a reliable correlation between secular trends in oil-price, and stocks of crude oil and refined products. Rising stock levels correspond to falling prices and vice versa.

C.I. and prices have increased together during this price rally (Figure 4). That is anomalous and suggests that higher price is because of sentiment and not supply-demand fundamentals.

Figure 4. Increasing WTI price with increasing comparative inventory (C.I.) is anomalous. C.I. and price are normally inversely correlated. Source: EIA and Labyrinth Consulting Services, Inc.

Some analysts think that the price increase signals a fundamental shift in market pricing. I expect higher prices some time in 2020 when optimistic forecasts for U.S. production are found to be flawed. That said, I find no reason for higher WTI prices now.

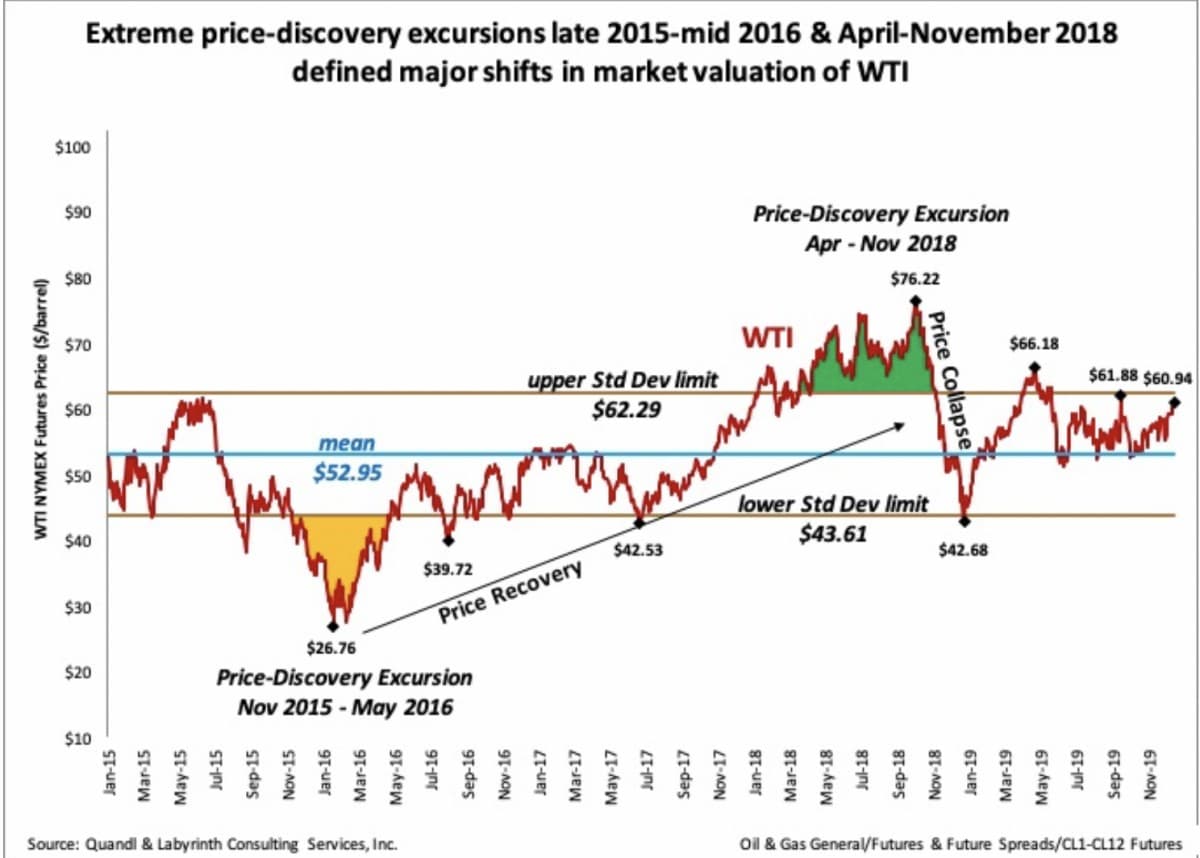

For the past 5 years, WTI has been well-constrained around a mean of about $53 except for two significant excursions (Figure 4).

The first began in late 2015. The implications of the 2014 oil-price collapse and slowing world economic growth produced widespread pessimism in oil markets. WTI fell to less than $30 per barrel in early 2016. That price-discovery excursion persisted 7 months and defined a price recovery that lasted until October 2018.

Figure 4. Extreme price-discover excursions in late 2015 and April through November 2018 defined major shifts in market valuation of WTI. Source: Quandl and Labyrinth Consulting Services, Inc.

The second excursion was in 2018. Prices exceeded one standard deviation from April through November. It was largely driven by anticipation of U.S. sanctions on Iranian oil exports. The price collapse that followed defined another major shift in oil-price valuation that has kept prices relatively subdued through 2019.Related: Iran: We Won’t Agree To Any Production Cuts In The Future

I see nothing about that this price rally that suggests a shift similar to these signature events. Markets famously shrugged off an almost 6 million barrel per day outage when Saudi refineries were attacked in September.

Why should a trade agreement have more effect than the largest supply outage in history? Why should another OPEC+ production cut achieve what previous cuts have not?

I expect that this rally will continue into the new year. WTI prices of $63 or somewhat higher would not surprise me.

It will last as long as someone can be found on the other side of the trade. When those counter-parties realize that nothing in the world has fundamentally changed, prices will fall to $51 or $52 as they have with the last three failed rallies of 2019.

By Art Berman