by Brian Maher from The Daily Reckoning

How far might markets plunge next time around?

And will you be able to recover your losses rapidly?

Answers — possibilities, rather — shortly.

And is one of Wall Street’s oldest chestnuts of investment wisdom tragically wrong?

This question too we will tackle.

But first to that vicious den of sin and iniquity — the stock market.

The Dow Jones roared 353 points today. The S&P rallied 28 points and the Nasdaq… 109.

For reasons we turn to the president’s comments this morning:

Had a very good telephone conversation with President Xi of China. We will be having an extended meeting next week at the G-20 in Japan. Our respective teams will begin talks prior to our meeting.

That G-20 meeting transpires June 28-29.

We shall see.

But how much value can you expect the stock market to shed in the next bear market?

The United States economy has endured recession every five years since World War II — on average.

Yet the present economic expansion runs to 10 years. It will be crowned history’s longest next month.

How much longer will the gods of chance be put off, cried down, ridiculed and shooed away?

10-year Treasury yields have slipped beneath 3-month Treasury yields.

This yield curve inversion has preceded each and every recession 50 years running.

And last week the yield curve inverted to its steepest degree since April 2007.

Meantime, Morgan Stanley’s Business Conditions Index just endured its largest-ever monthly plummet.

It presently languishes at its lowest level since December 2008 — the teeth of the financial crisis.

In Morgan Stanley’s telling, the American economy may already be sunk in recession.

But today or 18 months from today… a bear market will likely come dragging in on recession’s coattails.

Thus we arrive at the inevitable question:

How much value might the stock market lose in the next bear market?

Financial journalist Mark Hulbert interrogated the history since 1900 (based on data from research firm Ned Davis).

Investors have withstood 36 bear markets in these 119 years.

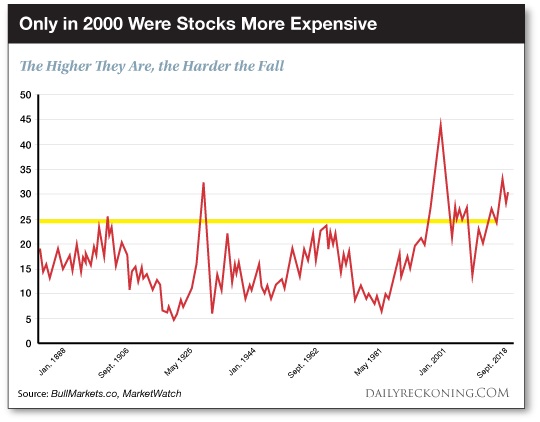

Hulbert then zeroed in on stock market valuations.

In particular, to the cyclically adjusted P/E ratio (CAPE) hatched by Yale man (and Nobel winner) Robert Shiller.

At 30.2, CAPE is mountain-high — that is, stocks are vastly expensive by history’s standards.

Today’s valuations rise even above 1929’s — and put 2008’s in the shade.

Only during the dot-com delirium were stocks dearer than today.

Hulbert’s research reveals bear markets tend to greater severity when stock valuations are elevated.

And so given today’s wild valuations, how far might the Dow Jones drop next time?

The answer, says Hulbert… is 35.3%:

A simple econometric model whose inputs are past bear markets and CAPE values predicts that, if a bear market were to begin from current levels, the Dow would tumble 35.3%. Though that’s less severe than the 2007–09 bear market, it still would sink the Dow below 17,000.

In fairness…

Hulbert concedes his findings do not rise to the 95% confidence level he seeks. But can you safely throw them aside?

Assume the Dow Jones does go tumbling 35.3% — beneath 17,000.

Worry not, says Wall Street.

Hold on for the long pull. Buy and hold is the way.

The stock market always comes back, the learned gentlemen assure us.

The magic of annually compounding returns will ultimately leave you in easy waters.

But have another guess, says analyst Lance Roberts of Real Investment Advice…

Perhaps you seek 10% compounding annual returns for five years.

Ten percent is handsome — but not extravagant.

Assume 10% is precisely what you receive the first three years. But you lose 10% the fourth.

What then happens to your gorgeous five-year 10% compounding?

You would need to haul in a ludicrous 30% return the fifth year… to catch up.

Roberts:

The “power of compounding” ONLY WORKS when you do not lose money. As shown, after three straight years of 10% returns, a drawdown of just 10% cuts the average annual compound growth rate by 50%. Furthermore, it then requires a 30% return to regain the average rate of return required.

If you are approaching retirement — or already in retirement — can you afford to stagger 10%?

Or 20%?

You must further consider today’s extreme valuations.

The higher the valuation… the lower returns you can expect over the next several years.

At today’s valuation extremes…

Would you be better off placing $3,000 into the stock market each year — or wedging it under your mattress?

Roberts has given the numbers a good, hard soaking. At 20x valuations, he finds…

Your stock market money would finally exceed your snoozing cash… in twenty-two years.

22 years!

“Historically, it has taken roughly 22 years to resolve a period of overvaluation,” affirms Roberts, adding:

Given the last major overvaluation period started in 1999, history suggests another major market downturn will mean revert valuations by 2021.

And recall — today’s CAPE is 30.2%. Perhaps stocks must wait even longer to break ahead.

But can you afford to wait?