Wolf Richter wolfstreet.com, http://www.amazon.com/author/wolfrichter

Ironically, after having lamented the flattening yield curve for a year, soothsayers are now lamenting the steepening of the yield curve.

On Friday, capping a rough week in the US Treasury market, the 10-year yield closed at 3.23%, the highest since May 10, 2011, and stocks fell for the second day in a row. This is an unnerving experience for pampered equity investors who’ve come to take endless stock-price inflation for granted, who’d figured for years that interest rates would never rise, and as short-term interest rates began rising, figured that long-term interest rates would never rise – and now they’re rising too.

To rub it in that this is a new world, similar to the old world before QE and before zero-interest-rate policy, another Fed heavy-weight discussed what’s coming: Quite a few more rate hikes.

New York Fed president John Williams told Bloomberg TV on Friday that we’re witnessing a “Goldilocks economy” with strong labor market, earnings growth, “low and stable inflation,” etc. “We want to sustain this economy, we want to keep it in good balance, so we don’t want to see inflationary pressures pick up,” he said.

And the topic came to “neutral” – the infamously theoretical short-term interest rate that is high enough to stop pushing the economy but is low enough to avoid slowing it.

“Of course, we don’t really know what the neutral interest rate is,” he said, pointing out that the FOMC members on average peg it at “about 3%. “We’re just a little bit above 2% for the federal funds target, so we have a ways to go to get to some idea of what people think of as neutral. We don’t really know where that is…. We continue to get closer to the range of neutral over the next year.”

This echoes Fed Chairman Jerome Powell’s pronouncements that “we’re a long way from neutral at this point” – and he’s thinking of taking rates beyond neutral [read… Powell Explains Just How Hawkish the Fed is Getting].

OK, so no slow-down in the rate hike tango next year. And the bond market is finally getting the drift of what this will do to long-term yields: They’ll rise too. And this caused some peculiar moves during the week:

- The 3-month yield rose just 4 basis points to close at 2.23% on Friday, October 5, the highest since February 2008.

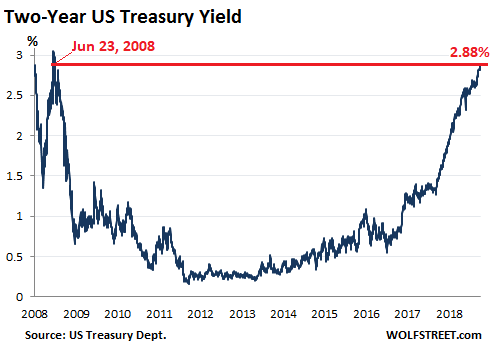

- The 2-year yield rose 7 basis points over the week, to 2.88%.

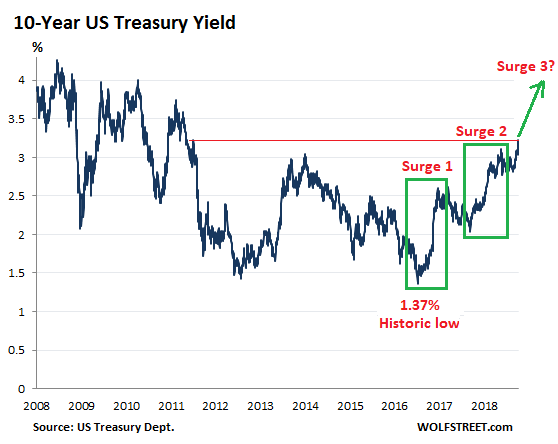

- The 10-year yield jumped 18 basis points, to 3.23%.

- The 30-year yield jumped 21 basis points, to 3.40%.

The 2-year yield that has now reached the highest level since June 23, 2018:

The real action was reserved for long maturities – surprising the folks that had been clamoring for a “yield-curve inversion,” where the 10-year yield would stay low, and the 2-year yield would rise above it. This yield-curve inversion phenomenon in the past occurred before recessions or worse. The last one occurred before the Financial Crisis.

So surely, if the yield curve inverts, the Fed would quit raising rates and Wall Street could go on undisturbed, the thinking went.

But over the week, the 10-year yield jumped to 3.23%. In this rate-hike cycle, the 10-year yield has moved in two surges of over 100 basis points each with some backtracking in between. Are we now looking at the beginning of the third such surge that would take the 10-year yield across the 4% line by mid-2019? Seems likely to me:

Surging long-term interest rates will raise borrowing costs for:

- Consumers, whose debts, including mortgages, have ballooned by $442 billion over the past year.

- Corporations, whose debts have ballooned by $574 billion over the past year;

- The federal government, whose debt has ballooned by $1.27 trillion in fiscal 2018.

- But state and local government debts have edge down a smidgen over the year (-$4 billion).

In total, indebtedness of consumers, corporations, and all governments has grown by $2.04 trillion over the past four quarters. And they’re going to be paying higher interest rates on this ballooning debt. In other words, debt service costs are going to rise substantially.

And a 10-year yield of 3.23% is still low, though it is incomprehensibly high to those who in mid-2016, had expected it to be zero by now. And it’s going higher.

The spread between the 2-year yield (2.88%) and the 10-year yield (3.23%) has widened to 35 basis points. This is still nothing to write home about, but it’s almost twice the 18-basis point spread on August 27.

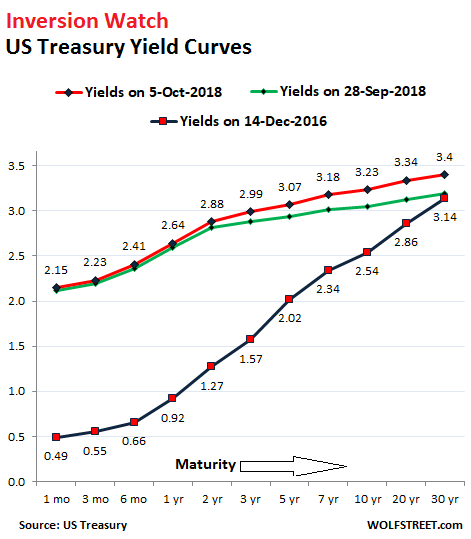

The chart below shows the yield curves on Friday, October 5 (red line); a week earlier, on September 28 (green line); and on December 14, 2016, when the Fed got serious about raising rates (blue line). Note how the red line has steepened compared to the green line, but remains relatively flat compared to the black line, especially from the 2-year yield on out. Friday’s 35-basis-point spread between the 2-year and the 10-year markers is still small compared to the 127-basis-point spread on December 14, 2016:

If the yield curve were to invert, the red line in the chart above would have a downward slope. But this yield curve isn’t ready to invert just yet.

Wall Street soothsayers had been postulating over the summer that the yield curve would invert by September’s rate hike, and that the Fed, scarred by the Financial-Crisis turmoil that happened after the yield curve had inverted last time, would then quit raising rates and give Wall Street a break. Instead, the yield curve has done the opposite – it steepened.

Ironically, after having lamented the flattening yield curve for a year in order to get the Fed to back off, these soothsayers are now lamenting the steepening of the yield curve. They now fear, as long-term debt gets more expensive for borrowers and more attractive for investors, that investors might abandon stocks, and that the ludicrously inflated stock market might start hissing a lot of hot air.