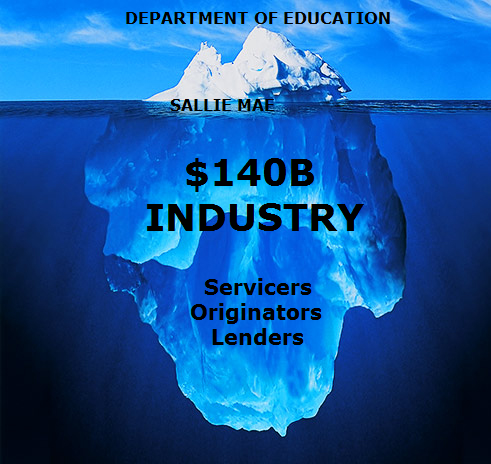

That said, the harshness of the term pretty well summarizes the $140B/ Year Student Loan, Finance & Servicing industry in America, which like an Iceberg is mostly hidden, below the surface. With student loans now totaling $1.4T this means that an additional 10% of that sum is being grafted annually from unsuspecting students and parents.

There has been an endless amount written in the last decade about the exploding size of the $1.4 Trillion of student loans outstanding . College tuition and expenses has risen at a financially devastating rate for students and their financially trapped families. What few however can answer satisfactorily is: Why has this occurred?

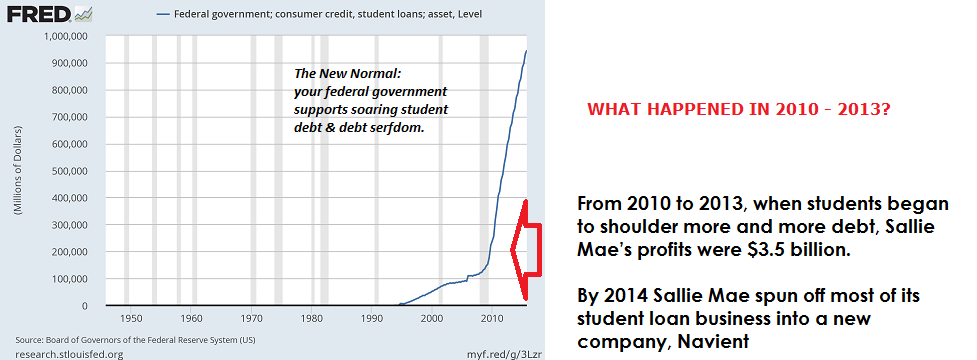

We can see from the chart below that this debt inducing juggernaut began gaining momentum in the mid 1990’s but then mysteriously exploded in 2010-2011. What happened in the early part of this post financial crisis decade?

Certainly students didn’t suddenly start wanting to go to college? College operating costs on the other hand didn’t abruptly get more expensive?

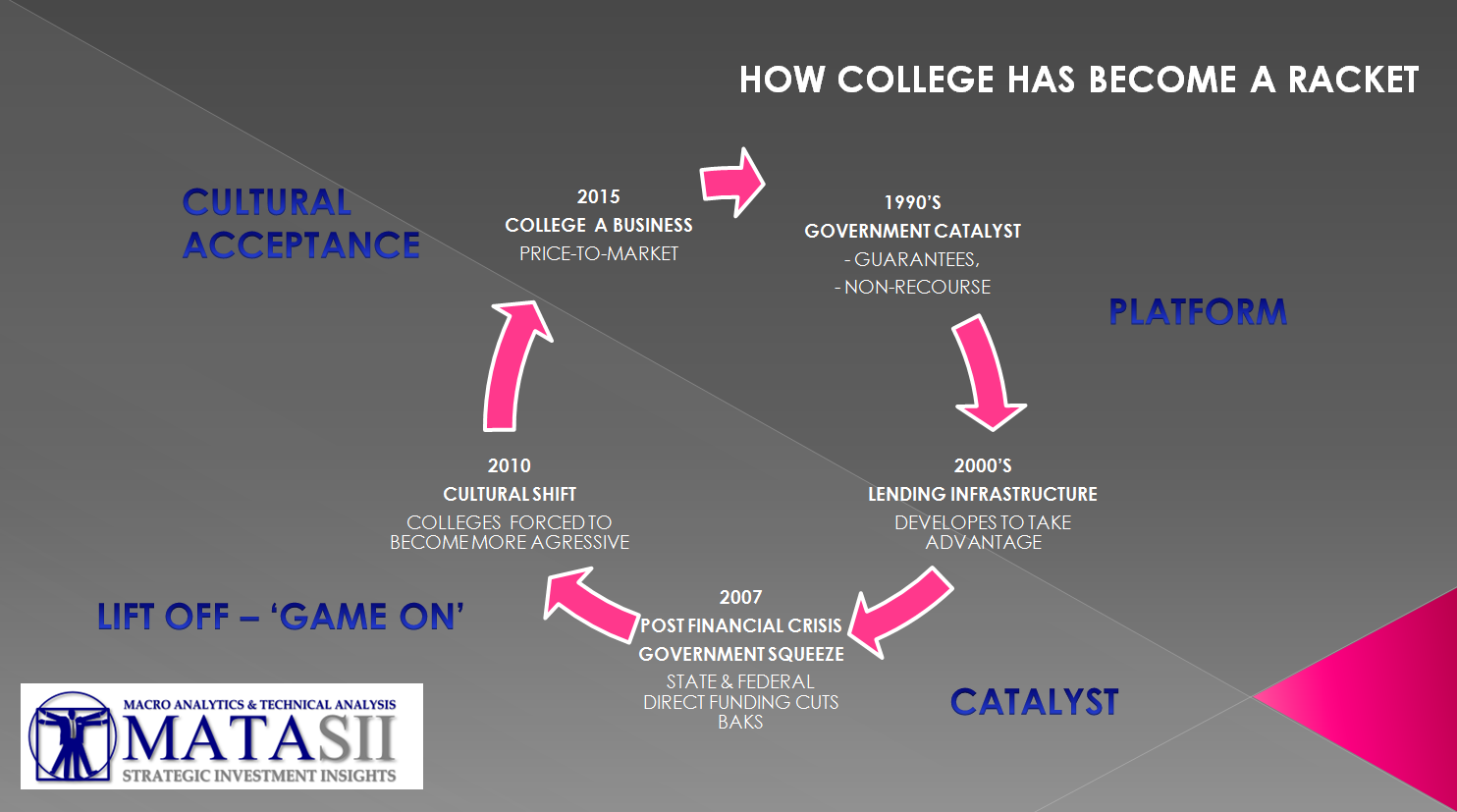

To understand the Student Debt Super Nova — Post-2010, we need to understand it in the context of a series of ongoing lift-off stages similar to a rocket launch, each stage accelerating the rocket upward towards a well planned trajectory.

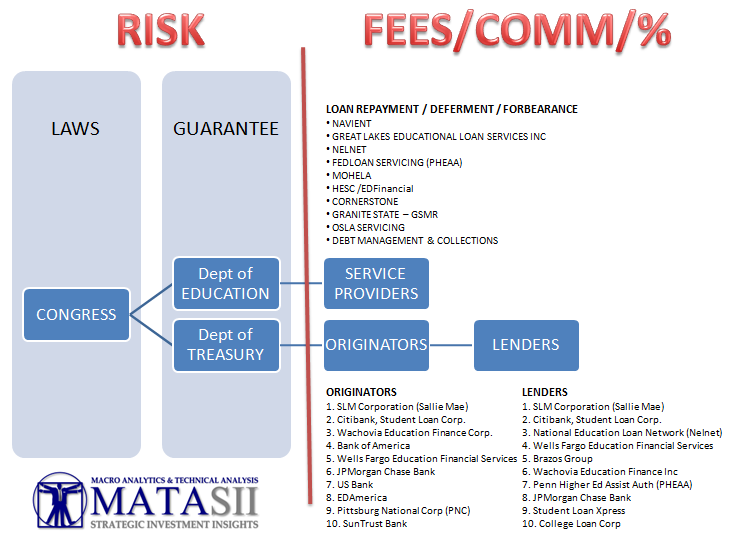

A BANKERS DREAM: A RISK-LESS INVESTMENT

The graphic above illustrates that the rocket was successfully placed in the launch gantry after three pivotal events had been successfully staged:

- The US Government accepted the full risk of student loans and financially Guaranteed Student Loans to the bankers,

- The banking lobbyist pulled off the biggest heist in history by having student loans made fully Non-Recourse loans, not dis-chargeable in bankruptcy court and open to debt garnishment procedures.

- Sallie Mae was privatized and was then allowed to operate without government oversight and constraints to become much more aggressive and highly creative and innovative in its approaches to making student loans available.

To the ‘money lenders’ this was a dream opportunity! An opportunity for “risk free” lending that needed to be fully capitalized on before the magnitude of the mistake was fully appreciated and consumer protection laws changed.

AN INDUSTRY IMMEDIATELY WANTED TO FEED OFF THE GOVERNMENT’S LARGESSE

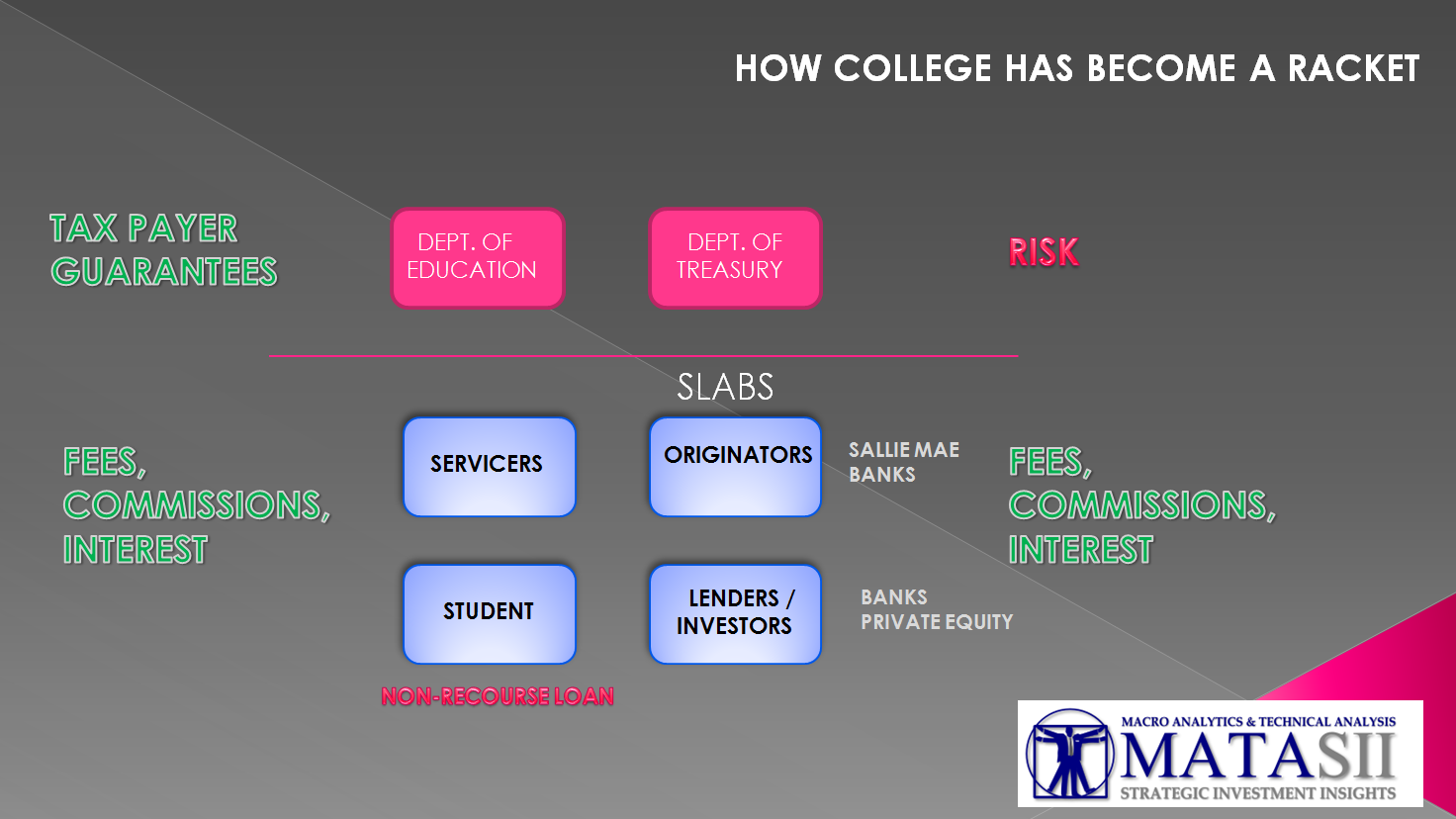

Like the housing bubble prior to 2007, financial players quickly emerged to grease the skids of easy money and student credit. The $140B industry spun off fees, commissions, interest payments for all manner of services and financing. The explosion in SLABS made CMBS, Auto ABS’, and MBS’ seem like the slow-lane of finance, after all these older vehicles actually carried risk. Major players grew rapidly keeping low profiles and attracting little public awareness.

We explore all this and more in a 44 minute video presentation which can be found here.

For the sake of brevity here is what we found most disturbing:

- TAX PAYER CARRYING ALL THE RISK

- Through Government Guarantees and Non-Recourse Loans, the government and students carry all the loan risk. Lending by definition comes with some risk but through effective lobbying this has been removed within the student lending industry.

- This ‘risk-less lending’ phenomenon is likely a historic first for lenders which will inevitably come home to roost for US tax payers.

- CORRUPTIBLE LENDING PRACTICES

- We learned during the Housing Bubble and Financial Crisis that when loans are packaged, sold and then are no longer held by the originators, then the opportunities for abuse increases significantly. It is seldom identified until the bubble bursts and an investigative light is shown upon it.

- The bigger the profits; the more unregulated the opportunity; the less educated the lenders and the more the perceived the demand for the product; — the more the opportunities for corruption.

- DISCONNECT BETWEEN VALUE & COST

- When money is lent and the terms are irrelevant of whether it can be economically justified, then a loan is unsound.

- There must exist a direct relationship between “value” and “cost” which today is completely missing within the existing Student Lending practice,

- Though for example degrees in Engineering, Medicine, Computer Science have a much higher probability of being repaid compared to a degrees in liberal arts, this is not a consideration in whether a loan is granted and guaranteed by the tax payers elected government.

- The student loan guarantee structure by design and via successful lobbying doesn’t differentiate “value” versus “cost”.

- NON-RECOURSE LOANS TO THE NAIVE ARE IMMORAL

- It is immoral to have our youth assume a “non-recourse”, non-bankruptcy discharge-able loan without having the experience and maturity to understand the risk and obligations that come with it.

- Desperate for a possible “future” our youth are unwittingly being forced to assume a loan type that no company, organization or investor would ever assume. No lawyer would advise it.

- STUDENTS & PARENTS NEED TO BE EDUCATED IN “RISK ACCEPTANCE”

- The education that students are receiving is nothing more than a ‘sales pitch’ on why an education is important to their future. This is not the critical requirement of sound lending practices,

- Little effective education is being given to student and parents on how risks are to be properly undertaken and receive professional counseled on whether the risks involved should in fact be assumed. Consumer protection enforcement guidelines have been blatantly omitted.

- There is no honest, unbiased counselor in the lending process. There are only short term profit motivations.

We need to stress that we are not suggesting anything illegal or nefarious is occurring in the Student Loan Industry. We would suggest that lending and servicing practices must be more tightly regulated and much stronger Consumer Protection laws quickly put in place to protect our youth from the destructive ravages of the soon to emerge – ‘unscrupulous’ debt collectors.

![]()

Like everything else, banks determine the cost. The kids and parents who must bear this are left with a handful of nothing. The banker’s mantra. They laugh all the way to the bank. Times change. Bankers don’t.

“What would Jesus do?”…oh wait, we already know the answer to that one!

Recently I keep getting robot calls about do you have unpaid student loans? If you do you could be eligible for a reduction OR a total forgiveness of your loan!!! Press one now. WTF? Now the govt is just giving this shit away again!!!! I don’t owe any student loan I just have a listed home phone number. Apparently they are calling everyone under the sun. Haven’t gotten these calls on my cell phones yet.

I find the whole higher education thing a big racket, seems before everyone jumped on the bandwagon, the nation was a much better place to live in, we had pretty much all the things man has today except the major problems, and there was no division of those with a piece of paper hanging from the wall and those who had not. I look around and ask myself daily what is it that has gotten better with this higher education thing and find nothing, crime is worse, the leaders are terrible, the nation is turning into a turd world country, the list is endless. So lets abolish college and return to the days when people had fewer problems and a better life.

Colleges and Universities should have to guarantee job placement with an adequate salary to pay back those loans and still be able to live a dignified life or have to pay back those student loans themselves!

No college means you can’t find work in big cities – period.

Big cities are ghetto sh:t holes full of welfare cretins…only jobs in big cities are government jobs catering to filthy humans…

That require a college degree from brain washing institutions of Marxism.

The elites hated the idea of college education for the serfs, which is what thousands of returning veterans got with the GI Bill after WWII. They have been doing everything they can to undermine and water down college education for “the rest of us”, and make a filthy buck on the side. Their scheme worked better than their wildest dreams of avarice.

I noticed the trend almost 30 years ago when it became obvious that night school classes were being skewed toward MBA’s and away from EE and ME’s. You could no longer go to night school to get your BSEE. You HAD to quit your job and go to day school to get that degree. The only night courses offered were for made-up degrees that were essentially worthless, except for the MBA courses. It was setup so that only those with sufficient financial backing could get real degrees, the rest of us were left with useless dregs.

College used to be a ticket to a career or a higher paying job. Now it’s a ticket to debt slavery.