By David Stockman

Yesterday afternoon brought three salient statements from Washington financial authorities that boil down to a simple admonition. To wit, if you are still in the Wall Street casino, run don’t walk toward the nearest emergency exit.

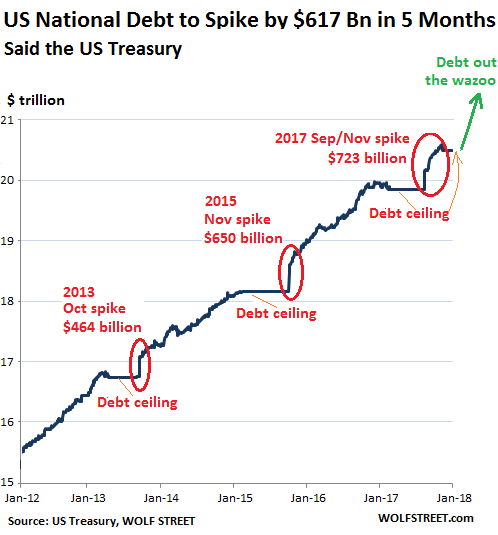

We are referring first to the CBO’s warning that Uncle Sam will run out of cash by early March if the debt ceiling is not raised sharply.

That warning was coupled, in turn, with the Treasury Department’s estimate that it will need to sell the staggering sum of $617 billion in new debt during the next five months. And, by the way, that short interval happens to include Q2 when the great annual fleecing of taxpayers causes a bulge in collections.

Finally, the Fed’s post-meeting statement assured that all is awesome with respect to the main street economy:

Information received since the Federal Open Market Committee met in December indicates that the labor market has continued to strengthen and that economic activity has been rising at a solid rate. Gains in employment, household spending, and business fixed investment have been solid, and the unemployment rate has stayed low.

Whew!

After all, the following chart might have been unnerving in the absence of the FOMC’s glowing confidence that the US economy is stronger than an ox and therefore, presumably, capable of shouldering the current eruption of Federal red ink.

Still, a crucial question recurs: Just because the US Treasury is happy to march the public debt across the $21 trillion mark, it doesn’t mean there are 60 votes in the Senate or 218 in the House for the same.

So in light of the above discordance, we now commence some ruminations on how both ends of the Acela Corridor have ended up in an economic fantasyland like no other. Fittingly, the origins of the latter are squarely rooted in the Eccles Building, and the imminent departure of Janet Yellen, mercifully, provides the perfect jumping off point.

The above quoted meeting statement is pure Yellen. That is, the ritual gumming of a Keynesian school marm which is utterly irrelevant to what the Fed is actually doing, and dead wrong besides.

The entirety of the four paragraphs statement consists of rubbery expressions of the Fed’s satisfaction that its goals for the labor market, inflation and economic activity are unfolding nicely. The only fly in the ointment, of course, is that the Fed’s interest rate manipulations and balance sheet inflation have had almost no impact on the said objectives.

In view of realized and expected labor market conditions and inflation, the Committee decided to maintain the target range for the federal funds rate ar 1-1/4 to 1?1/2 percent. The stance of monetary policy remains accommodative, thereby supporting strong labor market conditions and a sustained return to 2 percent inflation.

We will address tomorrow why the Fed has been tilting at macro-economic windmills for years.

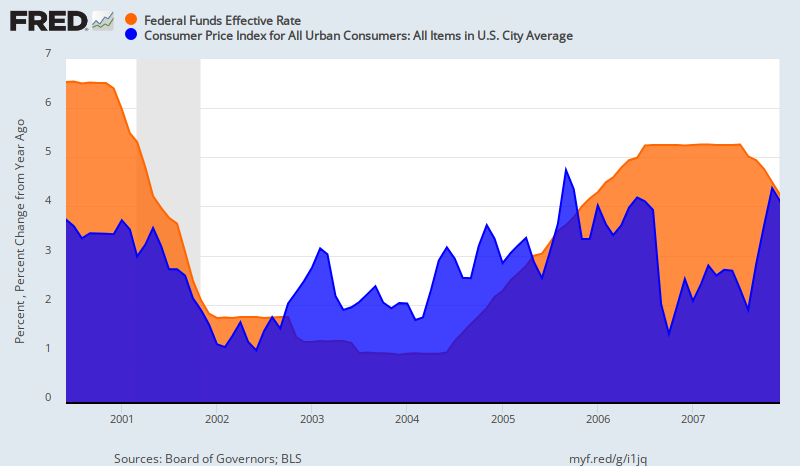

But first it needs be noted that we are already at 2.00% inflation even by the BLS’ sawed-off measuring stick. During the last 12 readings, the year-over-year CPI has been at or above the Fed’s target 75% of the time, and has posted an average gain of 2.14%.

If the Fed were a decent economic parent, therefore, it would have told the boys and girls on Wall Street that we are already “there” long ago. As it happens, in fact, the chart below means that in its wisdom the FOMC yesterday choose to stand pat in month #104 of the current expansion with a real funds rate at negative 0.8%.

Yet where was it ever written by even the good and great Keynesians of modern times—from Paul Samuelson to James Tobin to Milton Friedman (“monetarism” is just closet Keynesianism)—-that negative interest rates are in order during the ninth inning of what will soon be the longest business expansion in history (the record is 119 months during the 1990s)?

To the contrary, every bit of the economic learning prior to 2007 (including the Keynesian mis-learning) would have been appalled by the very idea of negative real rates for eight straight years—let alone at the tail-end of an expansion that has reached notional full-employment at 4.1% on the U-3 rate.

That’s because even the ancients (i.e. Wall Street and Fed economists who functioned prior to 2007) had at least an inkling that to impact the main street bathtub of GDP and its purported Phillips Curve trade off between employment and inflation, the Fed’s policies had to be transmitted through the canyons of Wall Street. So doing, they had the potential to distort the price of debt and other financial assets and to encourage undue financial market leverage and speculation.

Accordingly, even Greenspan determined in June 2003 that after marching the fund rate downward for 30 straight months (from 6.50% to 1.00%) that normalization of rates was in order.

By May 2005, therefore, the real funds rate was back in positive territory—with the target rate at 3.0% compared to a 2.8% Y/Y rise in the CPI.

In all, the Greenspan spell of negative real interest rates lasted about 30 months. Yet even then it elicited an orgy of Wall Street speculation in securitized mortgages and derivatives that fueled the September 2008 meltdown.

By contrast, since the end of the Great Recession in June 2009, the funds rate has been continuously underwater relative to the Y/Y trend of the CPI (save for the tiny orange specs in the chart) for more than 100 months, and sometimes to the tune of negative 2.0%. The picture below, in fact, amounts to the same thing as having issued an 8.5 year bond in Q2 2009 with a negative 1.2% coupon.

In retrospect, no one in their right mind would have bought such a bond at par. Nor would any sane central banker have failed to recognize that actually paying investors a 1.2% stipend to borrow at zero real cost for 104 months running was a recipe for rampant speculation and risk-talking.

As it happened, however, the Yellen Fed has been so obsessed by its magical 2.000% inflation target (as measured by the PCE deflator) that it has kept its foot firmly on the neck of the money market rate—-notwithstanding the retrospective madness of it and the overwhelming catalyst for carry-trade speculation that it provided.

That is to say, any security with a positive yield or prospect for even modest appreciation became a target for repo-style leveraged speculation. Traders bought the “asset” on 70-95% leverage, and did so with brimming confidence that they could roll the funding over and over again at virtually zero nominal cost.

Why such exuberant confidence?

In a word, because the Fed destroyed the free market in money. Short-term debt became a completely pegged, administered market—-locked into place by the $2.5 trillion of excess reserves the Fed’s wild balance sheet expansion had cycled into the banking system; and on top of that, further reinforced by the Fed’s foolish pledge of “transparency”, which meant that even a 25 bps change in the money market rate would be telegraphed well in advance through the hideous device of the Fed’s Dot Plot.

Yet the resulting falsification of asset prices, the yield curve, risk spreads and every other price signal within the canyons of Wall Street was obvious to any sentient observer. So why did Yellen & Co. keep their head down in splendid obliviousness year after year?

The answer is this: There was no reason other than the pall of groupthink, whereby the monetary central planners at the Fed became fixated on the PCE deflator as a measure of inflation, when it is no such thing; and became enslaved to the risible assumption that the second decimal place on the annualized inflation rate makes a difference, when that cannot possibly be true.

While the Fed swears by it, the personal consumption expenditure (PCE) deflator absolutely does not measure apples-to-apples price change. Instead, it reflects the changing weight of various goods and services in the 70% of GDP accounted for by personal consumption expenditures.

That means, of course, that if the price of steak and movie tickets go up but the relative volume of consumption for these items goes down and is replaced by chicken and Netflix, no inflation is recorded. By contrast, in a fixed weight index like the CPI these short-term consumption fluctuations don’t impact the measuring stick, and appropriately so.

Our point is that when the average price level rises by 2.0% during a year, the principal value of a government bond goes down by a like amount, whether the owner is eating steak or chicken.

Accordingly, from the point of view of the financial markets—thru which all of the Fed’s manipulations and interventions traverse—-the PCE deflator is the last inflation gauge you would use. Despite all of its imperfections, the CPI is a far truer measure of “inflation” in the general price level, and most especially in the financial markets.

The reason why the Fed prefers the PCE deflator, of course, is evident in the chart blow. Since the turn of the century when all out money printing became a way of life at the Fed and other central banks, the CPI has risen by 46% compared to only 37% by the CPI.

On an annualized basis, therefore, the Fed’s target has been met and then some—with the CPI clocking in at a 2.14% annual rate for the entirety of this century. By contrast, the PCE deflator computes to a 1.82% rate during the same period.

Still, here’s the thing. Do these fools really think that a microscopic 18 bps shortfall from their notional inflation target over 18 years makes any difference? There is simply not a shred of economic evidence anywhere that an economy performs better at 2.00% inflation over extended time periods than it does at 1.82%.

Indeed, the Fed’s entire inflation targeting regime amounts to statistical fetishism with a vengeance.

The problem, of course, is that this asinine obsession has not been pursued in a vacuum. By keeping the money market rate staked to the floorboards on the front-end, and via massive QE purchases across the entire length of the yield curve, the Fed triggered a giant financial fraud and deformation.

The $4.0 trillion of b0nds it purchased via credits conjured from thin air since the turn of the century—–and the $20 trillion by all central banks on a worldwide basis—-caused the bond market to clear at the wrong prices. That is, at yields which were far too low relative to the supply of real money savings.

But in the process of getting there, a second distortion was generated. Namely, bond traders and arbitragers added to the mispricing by front-running the central banks—buying today what the latter promised to buy tomorrow.

So doing, the central banks have generated the mother of all bond bubbles and something more. Namely, they have completely euthanized the politicians fiscally—-inherent spenders who didn’t need much encouragement in the first place.

So now the Washington end of the Acela Corridor has no clue that all fiscal hell is about to break loose as it stampedes toward a $1.2 trillion deficit during the tenth year (FY 2019) of a business cycle that is fast reaching its sell by date.

At the same time, the casino gamblers have built an edifice of grotesquely inflated financial asset prices that depend entirely on the ultra-low yields and cap rates that have been confected by the central banks and their front runners.

The pity is that a bond market shock of biblical proportions is now just around the corner—yet neither end of the Acela Corridor sees it coming.

So now is the time to head for the emergency exits. They will soon become impassable—-especially after the awesome economy celebrated by yesterday’s meeting statements is shown to be a snare and delusion.

That part of the fantasy we will address in more detail tomorrow.

Stockman is all over it and Trump would have been smart to bring him into his administration. Trump is making the mistake of spending like a drunken sailor and not raising taxes to close the gap where he can. The middle class and corporate tax cuts were probably necessary, but the tax cuts on income of the top 5% were unnecessary. The Fed has become a political animal afraid of its own shadow. It was necessary to keep rates low at the end of Obama’s term to keep the QE charade they had built going and similarly so at the beginning of the Trump administration the ponzi scheme had to be continued. Stockman knows the day of reckoning is coming. He will be proven right eventually and it will not be pretty.

The problem is where to run to. With interest rates rising and inflation coming the bond market does not look too attractive.